The mechanism lesson answers "what anchors a peg." Lesson 3 discusses: when the peg comes under pressure, how prices in the market reflect values like $0.98, $0.95, or even lower, and whether this process presents a brief arbitrage opportunity or signals rising systemic risk. "Depeg" and "run" are often used interchangeably: depeg refers to the price outcome, while run describes behavior and liquidity processes; they often occur together, but not necessarily at the same time.

1. Where Depegging Occurs: Primary Redemption Price vs. Secondary Trading Price

There are at least two "price" concepts for stablecoins:

-

Theoretical Peg Price ($1 USD): The face value promised by the issuer or protocol, as well as the reference price for primary market minting/redemption.

-

Secondary Market Price: The actual trading price on spot exchanges, on-chain DEXs, or OTC. Most holders interact with this layer.

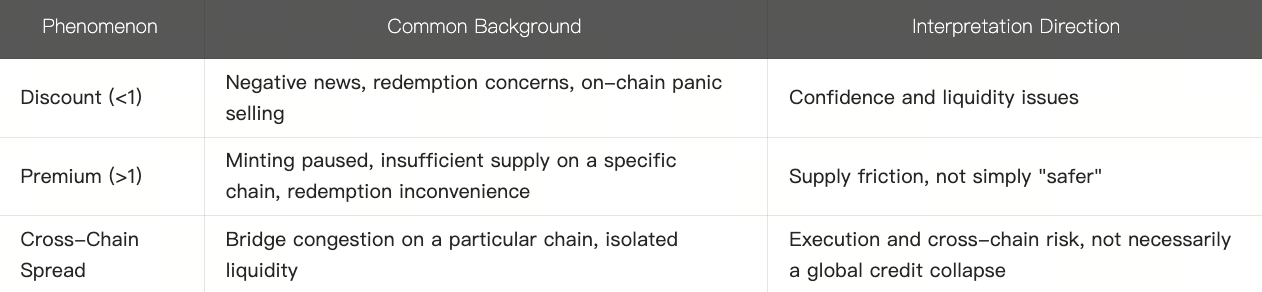

When secondary market prices remain below $1 for an extended period, it is referred to as discounted depeg; prices above $1 are called premiums (commonly seen when redemption is restricted, minting paused, or certain chains have liquidity shortages).

Depegging does not necessarily mean "reserves instantly go to zero," but is often the result of redemption friction + loss of confidence + liquidity withdrawal.

2. Typical Depegging Transmission Chain

Most events can be understood through a simplified chain:

-

Trigger Factors: reserve doubts, regulatory actions, banking risks, collateral crashes, protocol vulnerabilities, major negative news, etc.

-

Confidence Declines: holders tend to swap stablecoins for BTC, ETH, or other stablecoins; market makers narrow quotes.

-

Secondary Market Liquidity Thins: on-chain pool depth drops, spreads widen; large trades push prices quickly away from $1.

-

Arbitrage Blocked: if primary redemption slows, is capped, paused, or KYC/channels are restricted, arbitrageurs cannot quickly "buy low redeem" to correct deviations—depeg persists.

-

Run and Deep Depeg: Large-scale redemption requests pile up; issuers sell reserve assets or limit redemptions; price falls further, affecting DeFi collateral and leveraged positions.

The educational takeaway from this model is: the earlier the intervention, the smoother the redemption, the deeper the liquidity—the shorter and shallower the depeg; otherwise, it can intensify.

3. Runs: Not Just for Banks

A run in the stablecoin context means a large number of holders simultaneously seek to exit (swap back to fiat, convert to other assets, withdraw cross-chain), causing:

-

Extended redemption queues or caps;

-

Reserve assets must be sold at a discount to meet payouts;

-

On-chain transfers congested, gas fees surge;

-

DeFi protocols relying on the stablecoin see collateral quality deterioration and liquidation waves.

Fiat-collateralized run

Focus is on whether the issuer can process redemptions timely, fully, and at face value, and whether reserves are highly liquid. If reserves are heavily allocated to long-duration assets, they may face mark-to-market losses under interest rate or liquidity shocks, further undermining confidence.

Overcollateralized run

Manifests as stablecoin sell-off → collateral ratio drops → increased liquidations → collateral selling pressure → both stablecoin and collateral decline in feedback loop. The March 2020 scenario is a classic teaching case (parameters vary by protocol).

Algorithmic run

Often happens faster: absorption tokens and stablecoins spiral down within days or even hours, with arbitrage and market making nearly failing.

4. Discount and Premium: Different Deviations, Different Meanings

Therefore, monitoring depegging requires looking beyond just one exchange price—observe whether mainstream venues resonate and which chain or pool deviates first.

5. Early Warning Signals: Observable and Recordable

The following signals are for raising vigilance and tightening risk budgets—not to assert "inevitable collapse."

1. Secondary Market Price and Depth

-

Main trading pairs continuously deviate from $1 (e.g., below $0.995 for several days with deepening);

-

On-chain major pool TVL drops, spreads widen;

-

Significant increase in large order slippage.

2. Primary Market and Issuer Dynamics

-

Announcements of minting/redemption pauses or adjusted redemption limits;

-

Sudden reserve composition changes, audit delays, custodian news;

-

Regulatory investigations, asset freezes, legal proceedings.

-

Sharp short-term drops in supply (redemption) or abnormal minting;

-

Surges in net stablecoin inflows to exchanges (potential sell pressure);

-

Concentrated DeFi-related liquidations or bad debt events.

4. Cross-stablecoin Flows

-

Absorption tokens crash (algorithmic structure);

-

Upstream stablecoins used as collateral depeg first (chain risk);

-

Sudden rate changes cause reserve asset value swings (fiat-collateralized reserves mainly in Treasuries).

It's recommended to organize these signals into a weekly or event-period checklist (to be incorporated into portfolio discipline in Lesson 6).

6. Educational Takeaways from Historical Scenarios

Fiat-collateralized volatility

Repeated brief discounts or premiums mostly relate to reserve transparency, regulation, and banking channels. Key teaching points: recovery is often linked to reopening redemptions + clear disclosures + return of market makers; duration ranges from hours to weeks.

Collateral-backed stress tests in extreme markets

When collateral plummets, whether liquidations absorb supply and whether governance can urgently raise stability fees or adjust parameters determines depeg depth.

Algorithmic collapse

As discussed in the mechanism lesson: after confidence breaks down, prices may never return to $1 for an extended period—eventually leading to restructuring or discontinuation. The lesson for holders: do not use algorithmic stablecoins as "cash" equivalents.

7. Behavioral Discipline During Depegging

For holders

-

Distinguish "short-term deviation arbitrage" from "credit events": for the latter, prioritize reducing reliance/concentration on that coin;

-

Avoid large market sells during extremely poor liquidity to minimize slippage;

-

Monitor whether redemption channels are open for your account type.

For DeFi users

-

Check whether loan collateral includes depegged assets;

-

Monitor liquidation thresholds and pool utilization rates;

-

Stablecoin LPs may face one-sided markets + IL + compounded bad debt during depegging.

For traders

Summary

Lesson 3 explains: depegging mainly manifests in secondary market prices—driven by confidence, liquidity, and redemption/arbitrage smoothness. The typical transmission chain is trigger → confidence drop → thin liquidity → blocked arbitrage → deepening run. Discount and premium have different implications; judge based on chain, venue, and primary market status. Early warning signals include price depth, issuer announcements, on-chain supply and cross-stablecoin flows, related collateral and sentiment—use these as monitoring checklists when risk heats up rather than single buy/sell signals. Lesson 4 will discuss friction in holding and circulation costs, explaining why net returns may still be impaired even after "peg restoration."