Lesson 1 defined stablecoins as "infrastructure for pricing and circulation," emphasizing that the same name does not imply the same risk. Lesson 2 dives into the mechanism layer: When the market says a token is "pegged to 1 USD," what exactly supports this price—is it reserves in a bank account, on-chain collateral and liquidation processes, or supply-demand rules and market confidence? Understanding the differences among these three mechanisms is the key to interpreting news about depegging, freezes, yield packaging, and regulation.

1. Fiat-Backed: Trust Rests on Issuer and Reserves

Basic Structure

Users deposit fiat currency or equivalent assets with the issuer (or an authorized institution), and the issuer mints an equal amount of stablecoins (or minus fees). Upon redemption, stablecoins are burned and fiat is returned. The on-chain token represents a claim or custodial share; its core value depends on whether the reserves are real, sufficient, liquid, and independently verifiable.

Common Features

-

Reserve assets are mostly cash, short-term government bonds, bank deposits, etc. (composition varies by issuer disclosure)

-

There is a centralized operating entity and compliance interface

-

Usually includes compliance features such as address freezing and blacklisting (necessary for combating crime but also means on-chain assets are not fully censorship-resistant)

-

Transparency relies on regular disclosures, audit reports, or proof of reserves (frequency and scope vary by issuer)

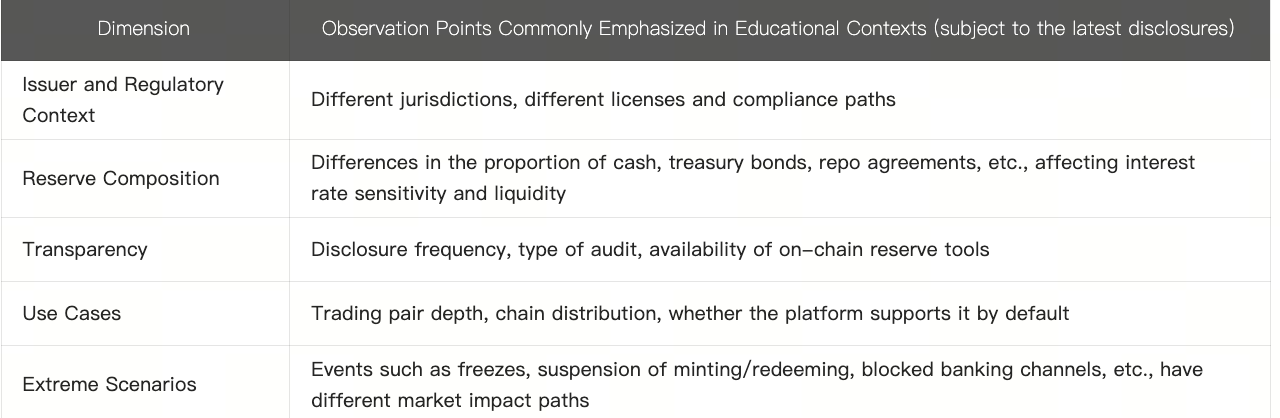

USDT and USDC: Both Are Fiat-Backed but Structurally Different (Teaching Comparison)

Key Mechanism Points

Depegging in fiat-backed stablecoins is usually not due to "mechanism design flaws," but rather issues of confidence and liquidity: market doubts about reserves, redemption congestion, regulatory shocks, or a lack of short-term arbitrage capital can cause secondary market prices to deviate from $1. Restoring the peg often relies on disclosures, opening redemptions, market making, and arbitrage—sometimes quickly, sometimes over time.

Advantages and Costs (General Knowledge)

-

Advantages: Intuitive structure, mature fiat onramps, typically good liquidity

-

Costs: Centralized credit risk, censorship risk, exposure to reserve rates and issuer operational risk

2. Crypto Overcollateralized: Trust Rests on Contracts and Collateral

Basic Structure

Users lock volatile assets like ETH on-chain to borrow stablecoins (e.g., DAI). The system requires a collateralization ratio above 100% (e.g., 150%). When collateral value drops and approaches the liquidation threshold, liquidators can repay debt and auction collateral to prevent the stablecoin from being undercollateralized.

Core Mechanism Components

-

Collateral ratio & liquidation threshold: determines system's tolerance for price volatility

-

Liquidation mechanism & penalties: incentivizes liquidators to participate and avoids bad debt

-

Stability fee/interest rate: adjusts supply and demand, influencing minting and repayment incentives

-

Governance & parameter adjustment: types of collateral, caps, liquidation discounts can be changed by governance (introducing governance risk)

DAI and Similar Models: Why They're Not "Purely Algorithmic"

Early narratives often called DAI the "decentralized stablecoin" representative. In practice, its collateral basket can include centralized stablecoins and RWAs (real-world assets), so its credit chain combines on-chain liquidation logic with off-chain asset credit. As DAI's scale grew, USDC's share in its collateral reserves once exceeded 50%, but later diversification into RWAs significantly reduced this proportion for a more balanced reserve. Thus, in this lesson's classification it remains "overcollateralized," but learners should check current collateral composition instead of relying on outdated impressions.

Sources of Depegging and Risk

-

Collateral crashes: extreme market conditions can lead to liquidation congestion and bad debt accumulation

-

Collateral and stablecoin drop together: increased correlation during systemic crises

-

Governance attacks or parameter errors: improper collateral onboarding or overly loose liquidation parameters

-

Upstream stablecoin depegging: if collateral includes USDC etc., there can be a chain reaction of stablecoins backing stablecoins

Advantages and Costs

-

Advantages: On-chain verifiable, strong composability with DeFi, not directly reliant on a single bank account

-

Costs: Complex mechanisms, collateral volatility, governance and smart contract risk, gas fees and operational barriers

3. Algorithmic Stablecoins (Algorithmic / Hybrid): Trust Rests on Rules and Market Dynamics

Basic Structure (Conceptual Level)

Attempts to maintain the peg using algorithms to adjust supply (mint/burn) or dual-token models (stablecoin + equity/absorbing token), without requiring full fiat reserves. Historically, many projects have shown that pure algorithms quickly lose confidence under stress.

Common Failure Modes (Mainly for Teaching Review)

-

Death spiral: slight depeg → market sells absorbing token → absorbing token crashes → further depeg of stablecoin

-

Liquidity exhaustion: DEX pools and market makers withdraw, arbitrage fails to correct price

-

Yield dependency: high APR attracts deposits; when yield becomes unsustainable, capital exits trigger a run

-

Under-collateralization or fake reserves: nominally algorithmic but essentially unbacked

Educational Value of Typical Cases (e.g., UST/LUNA Structures)

Don't memorize project names—extract lessons from mechanisms: when "pegging" mainly relies on market belief and arbitrage cycles rather than independently redeemable reserves, the system lacks a hard anchor during headwinds. Regulatory and market caution toward these structures will have lasting impact on new product design.

Current Market Status

Pure algorithmic stablecoins now account for a much smaller share in mainstream trading and DeFi core collateral. However, yield-wrapped products, synthetic dollars, and some hybrid models still appear under new names. The way to identify them is to return to Lesson 1's questions: What is redeemed? Who bears final losses? Where does liquidity come from?

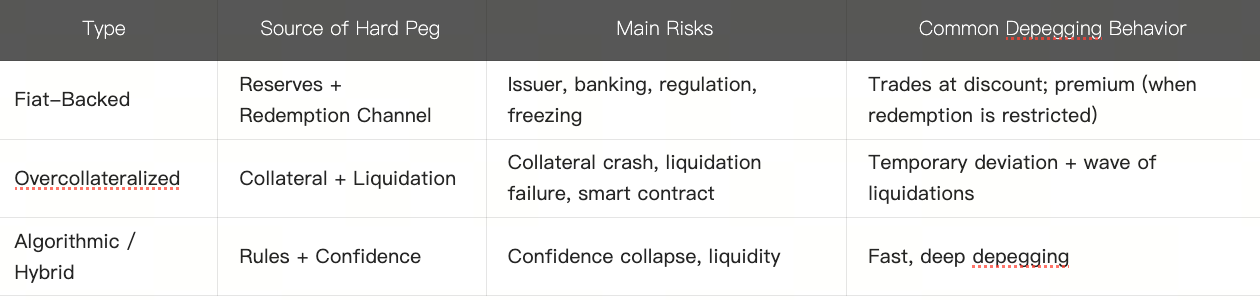

4. Three Mechanisms Side by Side: One Table to Remember "Trust Anchor"

5. Minting, Redemption & Arbitrage: How Price Is "Pulled Back" to $1

Primary Market (Minting/Redemption)

If the issuer offers reliable 1:1 minting/redemption with low friction, arbitrageurs will buy below $1 on the secondary market and redeem, or mint above $1 and sell—thus correcting deviations.

Friction includes KYC, minimum amounts, processing times, fees, banking hour limits—the higher the friction, the more likely secondary market prices will deviate from $1 for extended periods.

Secondary Market (Trading & DeFi)

Most holders don't redeem directly but trade on exchanges or on-chain pools. Here the peg is maintained by market depth + arbitrage capital + news flow. On chains or pools with poor liquidity, even slight sell pressure can cause notable depegging.

"Implicit Redemption" in Overcollateralized Models

By repaying debt to reclaim collateral, stablecoin supply is effectively destroyed; liquidation is the forced path. If liquidation markets fail, the peg also suffers.

6. Regulation, Freezes & What "Compliant Stablecoins" Mean

Fiat-backed models commonly face:

-

Address freezing: related to law enforcement requests; on-chain balances may become non-transferable

-

Issuer changing terms: suspending minting on certain chains or adjusting reserve assets

-

Regional restrictions: users in specific jurisdictions may be unable to use them

This does not mean "the project is a scam," but reflects product attributes. If traders use stablecoins for long-term storage or cross-border transfers, they must weigh auditability against "decentralization."

Overcollateralized models face more regulatory discussion around smart contracts and governance (such as whether collateral includes sanctioned assets), with different pathways from fiat-backed models.

Summary

The core of Lesson 2 is breaking down stablecoins from "all called $1" into three trust structures. Fiat-backed models rely on reserves and redemption channels—risks focus on issuers, banks, and compliance; overcollateralized models depend on collateral, liquidation, and governance—risks center around volatility, contracts, and upstream assets; algorithmic models rely on rules and confidence—which historically fail easily under stress. Price pegs are maintained by both primary market arbitrage and secondary market liquidity; friction and poor liquidity make deviations persist. With this framework in hand, Lesson 3 will go straight into contagion paths for depegging and runs—and which signals deserve special attention as risk rises.