This is not a routine rebound in the memory-chip cycle. The market is fundamentally revaluing SK Hynix—upgrading it from a cyclical memory-chip manufacturer to a core asset of AI infrastructure. High-bandwidth memory (HBM) is becoming another key component—after GPUs—for determining AI compute supply.

Triple tailwinds in sync: Why did SK Hynix suddenly surge 27%?

The July 15 surge was driven by the convergence of three tailwinds: fundamentals, institutional sentiment, and market mechanics.

First tailwind: Leading research institutions support it, reversing bearish expectations

The immediate catalyst was top-tier semiconductor research firm SemiAnalysis. On July 14, SemiAnalysis released a report titled “Greed When Others Are Afraid,” explicitly bullish on SK Hynix. The report forecasts SK Hynix’s 2026 Q2 DRAM blended average selling price (ASP) to jump about 45% quarter-over-quarter, with DRAM operating profit projected at around 55 trillion won. This figure exceeds many market consensus estimates and starkly contrasts with the pessimistic sentiment from the earlier downgrade by Korean brokerage KIS.

Second tailwind: Barclays initiates coverage with a $330 target price

On the same day, Barclays initiated coverage of SK Hynix’s ADR and assigned a “Buy” rating, with a $330 price target. Based on Tuesday’s closing price, the implied upside is approximately 70% to 100%. Barclays analysts believe that supply-demand tightness in the memory-chip industry in 2027 will intensify further, while limited improvement is expected in the supply-demand balance in 2028. The report specifically notes that by the end of 2027, SK Hynix’s cash position could exceed 40% of its market cap at that time, enabling large-scale share buybacks.

Third tailwind: Options listing and macro positives, boosting trading momentum

On July 14, options on SK Hynix’s ADR began trading on the U.S. Options Exchange. Early trading saw over two-thirds of volume concentrated in short-dated options expiring that Friday, with call options at a strike of $185 and put options at $145 actively traded. In the short term, demand for call options surged, attracting significant capital inflows.

On the macro front, the U.S. June CPI rose 3.5% year-over-year, below market expectations, easing concerns about the Fed implementing aggressive rate hikes. The CME FedWatch Tool shows the market-implied probability of a rate hike at the July meeting fell from 42% to 17%. This macro tailwind provided a more accommodative monetary environment for a broad rebound in risk assets.

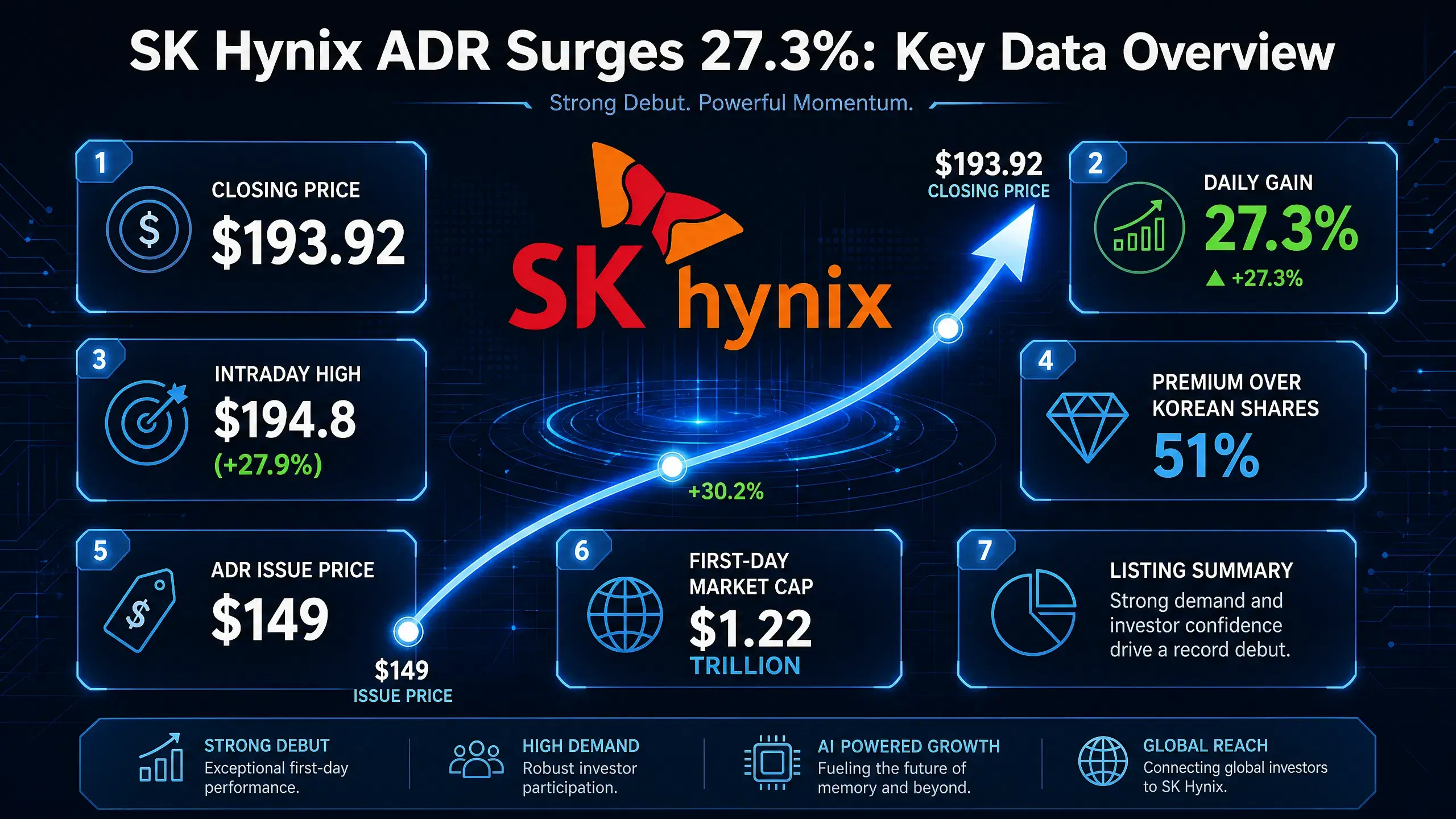

With these three tailwinds converging, SK Hynix’s ADR briefly topped $194.8 during the session, a gain of 27.9%. After the South Korean market opened on July 15, stocks surged in tandem—KOSPI’s rise widened to over 6%, SK Hynix’s shares in South Korea increased by more than 10%, and the Korea Exchange temporarily initiated the SIDECAR mechanism pause program for algorithmic buy orders.

SK Hynix ADR single-day surge — key data overview

HBM demand continues to explode: The core bottleneck in the AI compute supply chain

Behind SK Hynix’s surge is a structural explosion in HBM demand. HBM has become one of the most critical bottlenecks in the AI compute supply chain.

NVIDIA Blackwell architecture drives a surge in HBM demand

NVIDIA’s Blackwell architecture requires a substantial amount of HBM. In the Blackwell B200 configuration, there are 8 HBM3e chips, providing 192GB capacity and 8TB/s bandwidth. The Blackwell Ultra GPU includes 288GB of HBM3e memory, 1.5 times that of the previous generation. According to TrendForce, the 2026 Blackwell lineup will account for 71% of NVIDIA’s high-end GPU shipments. This means NVIDIA alone is driving HBM demand to grow exponentially.

HBM4 mass production begins a new cycle

More importantly, HBM4’s commercialization is underway. Korean media outlet The Bell reported that SK Hynix officially started shipping 12-layer HBM4 mass production for NVIDIA at the end of June 2026, moving into capacity ramp-up. This is the first time HBM4 has entered the market as a final specification with all quality certifications completed, targeting NVIDIA’s next-generation AI platform “Vera Rubin.” SK Hynix will officially expand HBM4 shipments starting September 2026.

NVIDIA’s Vera Rubin platform is expected to be delivered in Q3 2026, with terabit-level HBM4 memory in each server system. NVIDIA has confirmed that Samsung Electronics, SK Hynix, and Micron have all received HBM4 supplier certifications. Scaled mass production of HBM4 will elevate the HBM market from hundreds of billions of dollars into a higher tier.

Supply-demand imbalance continues to worsen

On the supply side, capacity growth is lagging behind demand expansion. According to SEMI China data, the HBM market size in 2026 is expected to grow 58% to $5.46 billion, representing nearly 40% of the DRAM market. Although Samsung, SK Hynix, and Micron—together the top three DRAM manufacturers—have allocated 70% of new capacity to HBM, the overall capacity shortfall remains at 50% to 60%. Goldman Sachs forecasts the global HBM market will reach $5.46 billion in 2026. TrendForce, as of May 2026, significantly raised its forecast for the global memory industry value; its 2026 estimate increased from $55.16 billion to $88.93 billion.

This supply-demand imbalance is not short-term. SK Hynix CEO Kwak Ryul-jung previously stated that 2027 will be the most supply-constrained year in the history of the storage industry, as customers increasingly seek long-term supply agreements to secure capacity.

Markets re-evaluate memory-chip profitability: from cyclical products to AI core assets

The valuation paradigm for the memory-chip industry is undergoing a fundamental shift.

Past logic: cyclical, low-margin industry

Traditionally, memory chips have been viewed as a cyclical industry—when supply increases, prices fall, and profits erode due to inventory pressures. Long-term concerns include DRAM price cycles, NAND pricing competition, and storage inventory buildup. These cyclical traits have kept memory-chip company valuations suppressed at relatively low levels.

Current logic: core AI infrastructure asset

AI is transforming this perspective. HBM is not ordinary DRAM—it is a core component in AI servers working alongside GPUs. The AI training compute chain can be simplified to: GPU (NVIDIA) + HBM (SK Hynix, Micron, Samsung) + advanced packaging (TSMC)—all three jointly determine AI compute capacity.

HBM’s supply-demand relationship differs markedly from traditional DRAM. HBM is typically secured via long-term supply agreements, so it does not fluctuate sharply with short-term market conditions. A South Korean securities firm noted that while long-term supply agreements limit price upside, they also enhance earnings stability and reduce the volatility historically seen in the memory industry. Going forward, market valuation will focus more on earnings sustainability than on short-term profit margins.

A structural uplift in profitability

Market expectations for SK Hynix’s profitability are being systematically revised upward. Although KIS forecasts second-quarter operating profit at 60.4 trillion won—below the market consensus of 65 trillion won—this remains very strong, up 61% quarter-over-quarter and 556% year-over-year. SemiAnalysis projects 55 trillion won in DRAM operating profit, confirming a structural improvement in profitability.

UBS recently raised its target price for SK Hynix to 320 trillion won and expects the share of HBM in DRAM revenue to increase from 15% in 2026 to 58% in 2030. If HBM’s average selling price rises further, it will support earnings in 2027. According to Koyfin, of 37 analysts tracking SK Hynix, 36 have issued “Buy” or “Strong Buy” ratings.

The market is recognizing that HBM’s dominance shifts valuation from cyclical profit volatility to a structural upward movement in the “center of gravity” of earnings.

SK Hynix leads the HBM market: competitive landscape and moat

Market share: clear leader

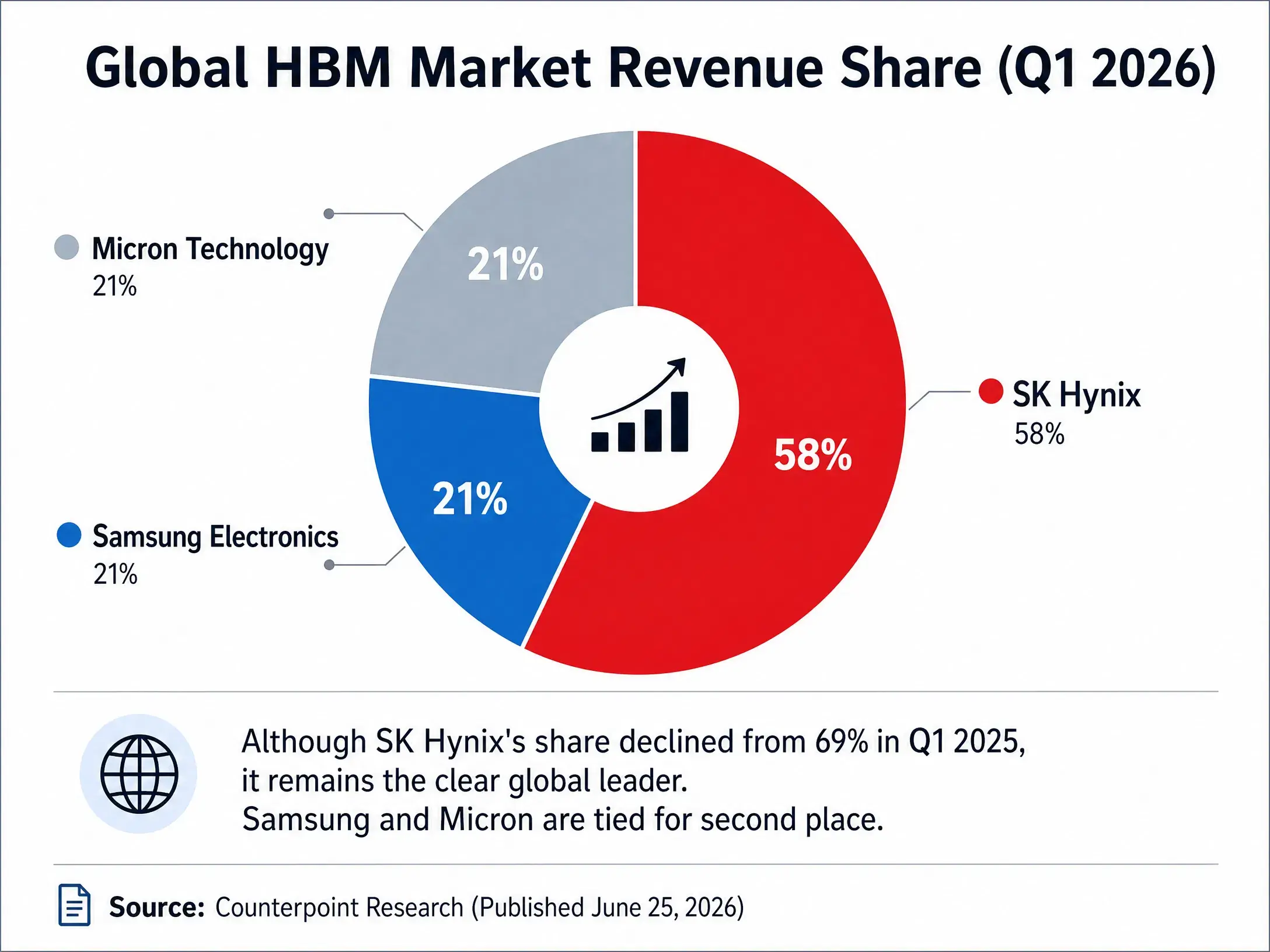

In HBM, the key segment, SK Hynix maintains a significant lead. According to Counterpoint Research, in Q1 2026, by revenue share in the global HBM market, SK Hynix held 58%, while Samsung Electronics and Micron each held 21%. Although SK Hynix’s share declined from 69% in the same period of 2025, it remains above 50%.

Looking ahead to full-year 2026, analysts forecast SK Hynix’s HBM revenue could reach $595 million. Counterpoint expects SK Hynix’s HBM4 share in 2026 to be about 54%, with Samsung at 28% and Micron around 18%. TrendForce projects SK Hynix’s full-year HBM market share in 2026 to stay near 50%.

HBM market “three giants” competitive landscape (Q1 2026)

Core moat: deep integration with NVIDIA

SK Hynix’s most critical competitive advantage is its close partnership with NVIDIA. As NVIDIA’s primary HBM supplier, SK Hynix’s HBM chips are directly embedded into NVIDIA’s AI accelerators. This supply chain position reflects technical capability and creates a strong customer lock-in. AI chip validation cycles are very long; once a supplier is integrated, it’s difficult to replace in the short term.

The mass production of HBM4 further consolidates this advantage. SK Hynix was the first to achieve 12-layer HBM4 mass production and became the first supplier to ship final-spec HBM4 products to NVIDIA. While Samsung’s HBM4 certification is progressing rapidly—with expected mass production after Q2 completion—SK Hynix has already secured the lead.

Competitive dynamics: a race for capacity among the three giants

Competitors are accelerating their efforts. Samsung plans to increase HBM capacity by 50% in 2026, targeting 250,000 wafers per month. Micron has already sold out its full-year HBM supply under fixed-price contracts. In early July, Micron announced a $9.3 billion investment to expand HBM capacity in Hiroshima, Japan, with shipments expected in two years. Samsung and SK Hynix together control over 80% of the global HBM market share.

While competition intensifies, SK Hynix’s first-mover advantage, scale, and customer relationships form a moat that is difficult for rivals to surpass in the near term.

Conclusion

SK Hynix’s 27% single-day jump reflects, on the surface, the convergence of three tailwinds—SemiAnalysis’s bullish report, Barclays’s buy rating, and macroeconomic data—but deeper down, it signifies a systematic revaluation of the memory-chip industry’s valuation model.

HBM is transforming everything. It is not merely an upgraded version of traditional DRAM but a core component of the AI compute supply chain, on par with GPUs. When the AI training compute chain simplifies to “GPU + HBM + advanced packaging,” HBM’s strategic importance becomes clear. The $5.46 billion HBM market in 2026, the 50–60% capacity shortfall, and the commencement of HBM4 mass production all point to one conclusion: the HBM super-cycle has begun.

For SK Hynix, its 58% HBM market share, close partnership with NVIDIA, and first-mover advantage in HBM4 mass production create a moat unlikely to be breached soon. The market currently prices this structural shift at a $1.36 trillion market cap.

Memory chips are no longer just a “cyclical, low-margin” industry—they are infrastructure for the AI era, and SK Hynix is becoming one of its most vital builders.

FAQ

Q1: What are the key figures behind SK Hynix’s surge on July 15?

SK Hynix ADR rose 27.29% to $193.92, with an intraday high of $194.8. Its South Korean shares increased over 10%, and the KOSPI index gained more than 6%.

Q2: What are the main drivers of SK Hynix’s surge?

The triple tailwinds: SemiAnalysis’s bullish report forecasting strong DRAM earnings; Barclays’s initiation with a “Buy” rating and $330 target; and options trading on SK Hynix ADR alongside U.S. June CPI data below expectations.

Q3: How large is the HBM market opportunity?

Goldman Sachs projects the 2026 global HBM market at $5.46 billion, up 58% year-over-year. SEMI China estimates a 50–60% capacity shortfall. TrendForce raised its 2026 global memory industry forecast to $88.93 billion.

Q4: What is SK Hynix’s position in the HBM market?

In Q1 2026, SK Hynix led with 58% revenue share; Samsung and Micron each held 21%. SK Hynix has begun shipping 12-layer HBM4 for NVIDIA.

Q5: How does HBM influence the valuation of the memory-chip industry?

HBM shifts valuation from a cyclical, low-margin industry to a core AI infrastructure asset. Long-term supply agreements stabilize earnings, and market focus moves from short-term profit cycles to sustainable earnings growth.