Summary

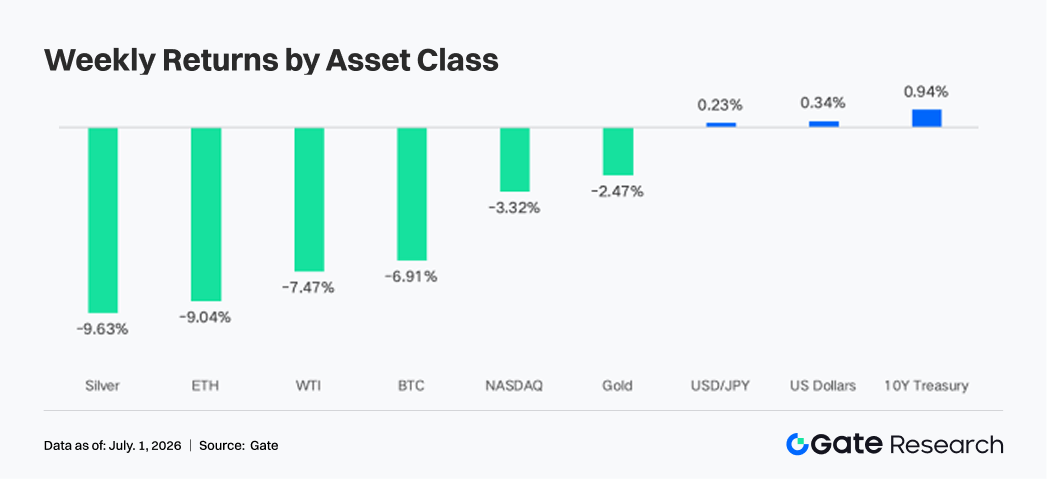

The easing of tensions in the Middle East pushed crude oil lower, and the market's trading logic shifted from the "war premium" to "higher-for-longer Fed rates." The Nasdaq fell about 3.3%, while BTC and ETH declined about 6.9% and 9.0%, respectively.

-

Spot BTC and ETH ETFs saw heavy net outflows, with BlackRock's IBIT and ETHA posting the largest outflows. As geopolitical risks cooled and volatility in AI tech stocks intensified, equities accounted for 55%-60% of TradFi Perp trading volume, with capital refocusing on risk trades tied to U.S. equities.

-

On-chain capital continued to concentrate in high-turnover trading venues, with PumpSwap becoming the largest incremental driver this week, reflecting a shift of capital in the Solana ecosystem from traditional DEXs toward issuance and high-frequency trading scenarios.

-

DeFi liquidity remained defensive. Stablecoins, LSTs, and lending markets all stayed broadly cautious. Aave lending balances contracted slightly, rates remained low, and capital continued to concentrate in Ethereum's core market, indicating that overall risk appetite has not yet clearly recovered.

-

BTC fell back to around $60,000, but this was not accompanied by a clear expansion in OI. Funding rates stayed positive, suggesting that this round of adjustment was driven more by spot selling and existing position reshuffling, while the overall BTC derivatives market remained in a low-leverage regime.

-

Monthly options volume expanded notably ahead of expiry. 25D Skew continued to weaken and DVOL rose to around 47-48, reflecting the market's repricing of downside risk.

1. Market Focus Analysis

Last week (June 22-28, 2026), the global macro narrative centered on three themes: easing geopolitical risks in the Middle East, still-sticky U.S. inflation, and continued hawkish expectations for Federal Reserve policy. First, after U.S.-Iran tensions eased temporarily, the market quickly marked down concerns over supply disruptions in the Strait of Hormuz, and the war premium in crude oil retraced significantly. Brent fell back to about $73.83 per barrel at one point, while WTI dropped below $70 per barrel. Lower oil prices reduced the risk of another upswing in energy inflation and also improved short-term consumer sentiment, with the University of Michigan consumer sentiment index for June rebounding by nearly 5 points from the prior reading. As a result, the market shifted away from the earlier trade of "geopolitical shock / rising oil / reaccelerating inflation" and toward reassessing whether inflation could continue cooling after energy prices eased.

However, U.S. inflation data did not support a rapid Fed pivot toward easing. May PCE inflation rose to 4.1% year-on-year, while core PCE came in at 3.4% year-on-year, still well above the Fed's 2% target. That said, month-on-month PCE was 0.4%, below the market expectation of 0.5%, which prevented a further sell-off in bonds. This combination means inflation pressure remains in place, especially in core services and wage-related prices, but there has not yet been a more serious near-term upside spiral. The market therefore maintained its higher-for-longer view while dialing back fears of a more aggressive hiking path. Treasury yields declined over the week, with the 10-year yield falling to about 4.37% and the 2-year yield to about 4.09%, reflecting lower inflation expectations due to falling oil prices, while the policy-rate path remained constrained by inflation.

From a macro transmission perspective, easing geopolitical tensions was supportive for risk appetite and bonds, but sticky inflation limited the room for asset valuations to recover. The U.S. dollar and real yields continued to weigh on gold, tech stocks, and crypto assets. The Nasdaq fell about 3.3%, while BTC and ETH declined about 6.9% and 9.0%, respectively. Meanwhile, lower oil prices helped ease corporate cost pressures and household inflation expectations. Overall, last week was not simply a safe-haven market. Rather, it was a repricing process in which the market shifted from the war premium to whether the Fed can maintain tight policy under persistently high inflation.

2. Liquidity Analysis

2.1 Institutional ETF Risk Appetite Cooled in Tandem, with IBIT Seeing Net Outflows of $1.304 Billion

BTC and ETH ETFs both saw clear outflows last week, indicating that institutional risk appetite cooled in tandem. Spot BTC ETFs recorded total net outflows of about $1.787 billion, worsening further from net outflows of about $228 million in the previous week. Spot ETH ETFs recorded net outflows of about $274 million over the same period, a significant deterioration from net outflows of about $10 million in the previous week. At the product level, the largest BTC ETF inflow went to Grayscale Bitcoin Mini Trust BTC, at about $71.7 million, while the largest outflow came from BlackRock's IBIT, at about $1.304 billion. For ETH ETFs, the largest inflow went to Bitwise ETHW, but it was only about $0.6 million, while the largest outflow came from BlackRock's ETHA, at about $236 million.

AUM likely moved lower week-on-week for both BTC and ETH. BTC fell about 6.91% last week, and together with heavy ETF redemptions, assets under management were dragged down by both price retracement and shrinking shares outstanding. ETH fell about 9.04% last week, while ETF-side inflows were even weaker, so AUM pressure was more evident. Overall, institutional sentiment shifted from prior allocation or wait-and-see behavior toward defense and position reduction. In particular, BlackRock products, which had previously been the strongest vehicles for attracting capital, became the main source of outflows, showing that core institutional money was also reducing crypto beta exposure. Compared with BTC, ETF demand for ETH was weaker, showing a more pronounced contraction in institutional risk appetite for higher-beta assets.

2.2 TradFi Liquidity

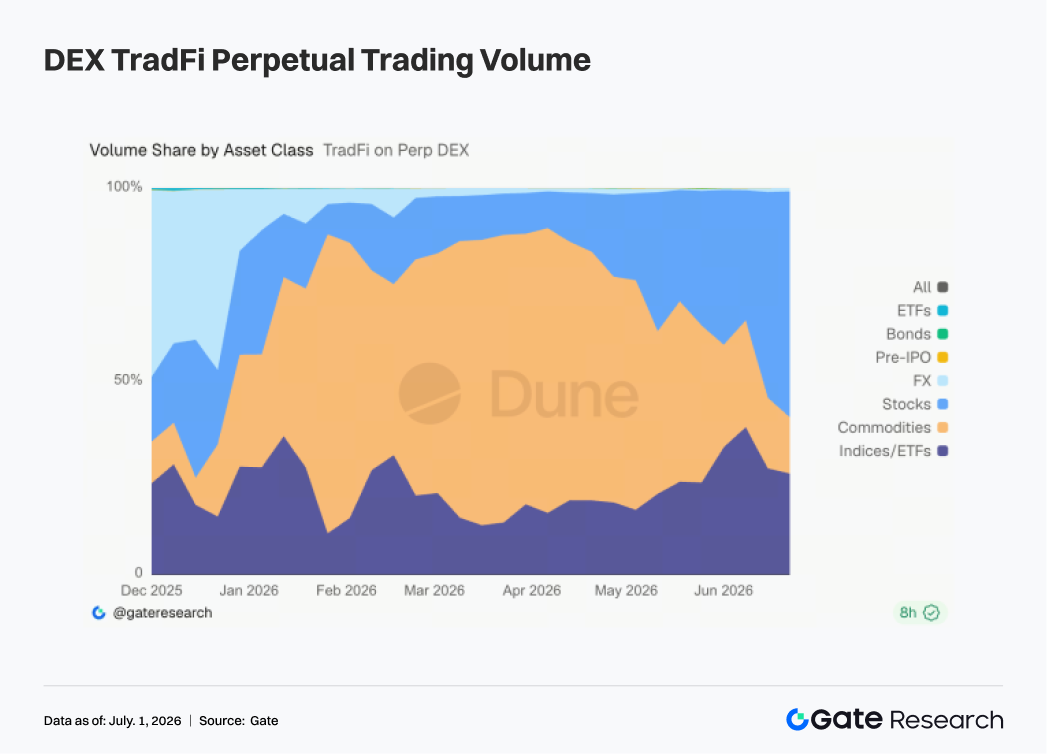

- TradFi Perp DEX: Over the past week, the trading structure on TradFi Perp DEXs shifted noticeably. Equity assets once again became the market leader, while trading heat in commodities continued to cool. Since late June, the equity share of trading volume has risen rapidly to about 55%-60%, making it the largest trading category. At the same time, the commodity share fell quickly from roughly 40%-50% to below 20%, showing that the previous heat led by safe-haven assets such as gold and crude oil weakened significantly. Meanwhile, the index/ETF share stayed relatively stable at around 25%-35% and remained an important allocation direction, reflecting that users are still participating in U.S. equity volatility through index products. This change is closely tied to the recent macro environment. Sharp swings in the U.S. AI sector, corrections in tech stocks, and the market's repricing of the rate-cut path all lifted trading activity in stock and index perpetuals. In addition, Pre-IPO-related assets such as SpaceX continued to attract attention, further drawing capital into the equity ecosystem. Overall, capital on TradFi Perp DEXs has been shifting away from commodity trading and back toward equities and index assets. The market's trading logic has gradually moved from geopolitically driven safe-haven trades toward risk trades built around U.S. equity volatility, the tech sector, and macro events. Equity assets are likely to remain the main growth driver for the TradFi Perp market.

-

Gate TradFi Perp Trading Volume: Despite a cautious macro backdrop, user demand for TradFi perpetual products remained strong. Over the past week, Gate TradFi Perp trading volume increased clearly week-on-week, with daily trading volume mainly concentrated in the $4 million-$6 million range. Overall volatility was more contained than in previous weeks, but trading activity did not show an obvious decline. By asset class, metals remained the absolute core source of volume, with precious-metal perpetuals such as gold contributing the vast majority of turnover. This reflects that under a hawkish Fed stance, recurring geopolitical risks, and gold prices fluctuating at high levels, safe-haven assets remain a key focus of market capital. At the same time, the share of index trading increased sharply from before, with a notable surge early in the week, showing that as the AI sector corrected, U.S. equity volatility rose, and stock-specific event drivers strengthened, user participation in U.S.-equity-related perpetuals continued to increase.

-

Number of Gate TradFi U.S. Equity Assets: Gate officially launched its U.S. equity trading service on June 2. Supported by real underlying assets, direct USDT trading, no overnight holding fees, and high liquidity, the business has continued to attract market attention since launch, with trading volume growing steadily. At present, Gate supports seven major asset categories, including ADRC, stocks, ETFs, ETNs, ETSs, ETVs, and PFDs, and it continues to expand product coverage. In terms of asset count, the total number of tradable instruments has doubled since launch. Among them, the stock category has grown the most significantly, with its share of all assets rising from about 70% in the early stage after launch to 85%, further enriching users' investment choices. Going forward, Gate will continue to expand market access, integrate global liquidity, and build cross-market trading capabilities, continuously broadening diversified asset coverage and further strengthening its strategic positioning as a global platform for asset trading and market access.

-

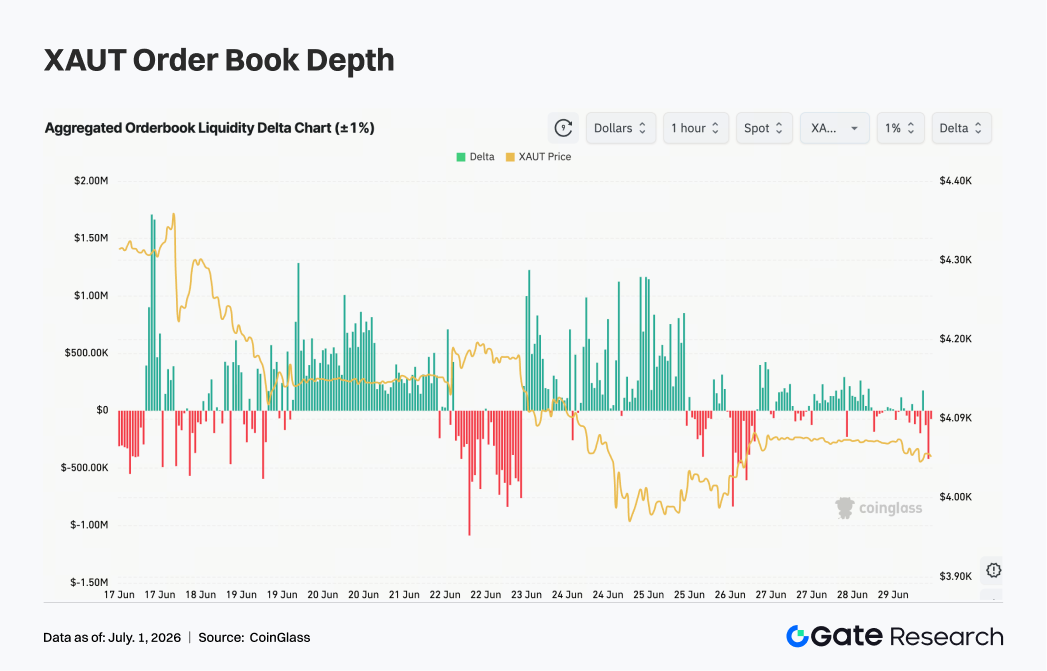

TradFi Order Book Depth: We selected XAUT, the highest-volume TradFi asset, to analyze order book depth (Delta). Over the past week, XAUT order book liquidity shifted from being previously dominated by bulls to being increasingly dominated by bears, while the price moved broadly in a choppy downtrend. Early in the week, Delta remained positive multiple times, with buy-side liquidity continuing to flow in and pushing XAUT to fluctuate in the $4,180-$4,330 range, showing relatively strong market absorption capacity. After June 22, however, as macro risk sentiment changed and gold prices fell back, order-book Delta turned sharply negative and repeatedly registered negative readings in the $0.5 million-$1.0 million range, indicating clearly stronger aggressive selling. XAUT simultaneously fell below $4,100 and at one point approached the $4,000 area, reflecting a concentrated release of short-term selling pressure. Although the order book still saw intermittent buy-side inflows over the weekend, the persistence of positive Delta weakened noticeably, and the market lacked sustained upside capital. If the U.S. dollar and Treasury yields stay elevated, gold tokens may remain under pressure in the short term. If rate-cut expectations improve later or geopolitical tensions heat up again, buy-side order-book strength may recover and drive a price rebound.

3. On-Chain Data Insights

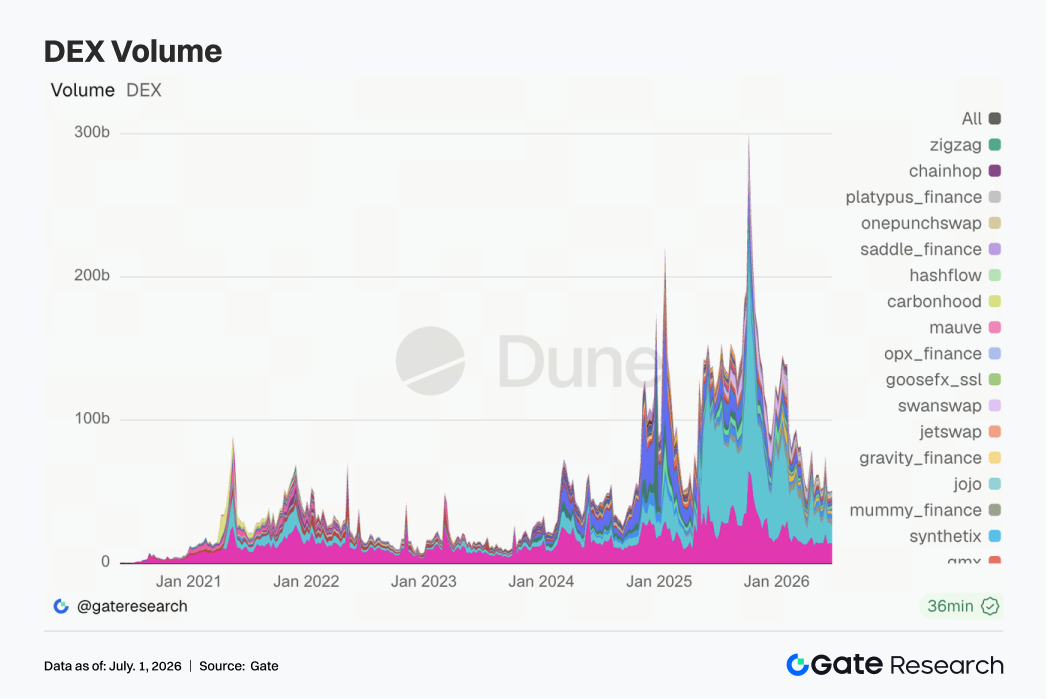

3.1 DEX Trading Volume Did Not Expand Broadly, and PumpSwap Was the Most Notable Structural Variable This Week

Overall DEX trading did not extend the strong expansion seen previously. Uniswap and PancakeSwap still ranked as the top two, but both saw slightly lower volume than in the previous week, and leading spot pools entered a period of consolidation at high levels. The key change came from PumpSwap, where both trading volume and trader count stepped up clearly, pushing it directly into the top three. Speculative traffic on Solana has not disappeared; instead, it has shifted from traditional entry points such as Raydium and Meteora toward issuance-oriented and high-frequency trading scenarios. Protocols such as Aerodrome, Bisonfi, and Tessera also saw some recovery, and Base plus emerging matching venues continued to absorb active capital.

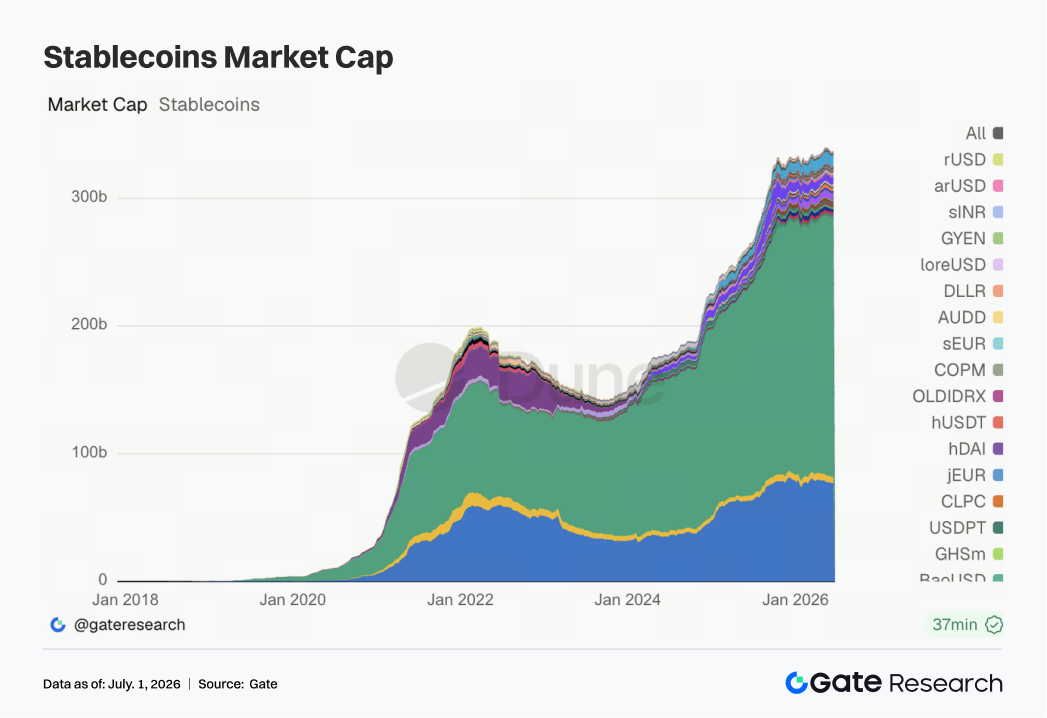

3.2 Stablecoin Supply Remained Defensive, and Regulatory Debate Had a Greater Impact on Pricing Than Short-Term Issuance

The stablecoin market as a whole remained in contraction this week. USDT and USDC both edged lower, while USDS, USDe, USD1, and PYUSD did not show clear expansion. Only DAI was relatively stronger. There was no large-scale new inflow of U.S. dollars on-chain; instead, existing capital mainly rotated among different stablecoins. On the news side, on June 28, U.S. community banking groups publicly opposed stablecoin-related legislation, with the core concern being that reward-bearing stablecoins could siphon deposits away from local banks. This elevated stablecoin regulation from a crypto-industry issue to a broader issue of redistributing interests within traditional finance. During the same week, the Bank of England also adjusted its stablecoin regulatory approach, shifting from holdings caps to issuance-size limits, indicating that major jurisdictions are all trying to balance innovation, payment efficiency, and the stability of the banking system.

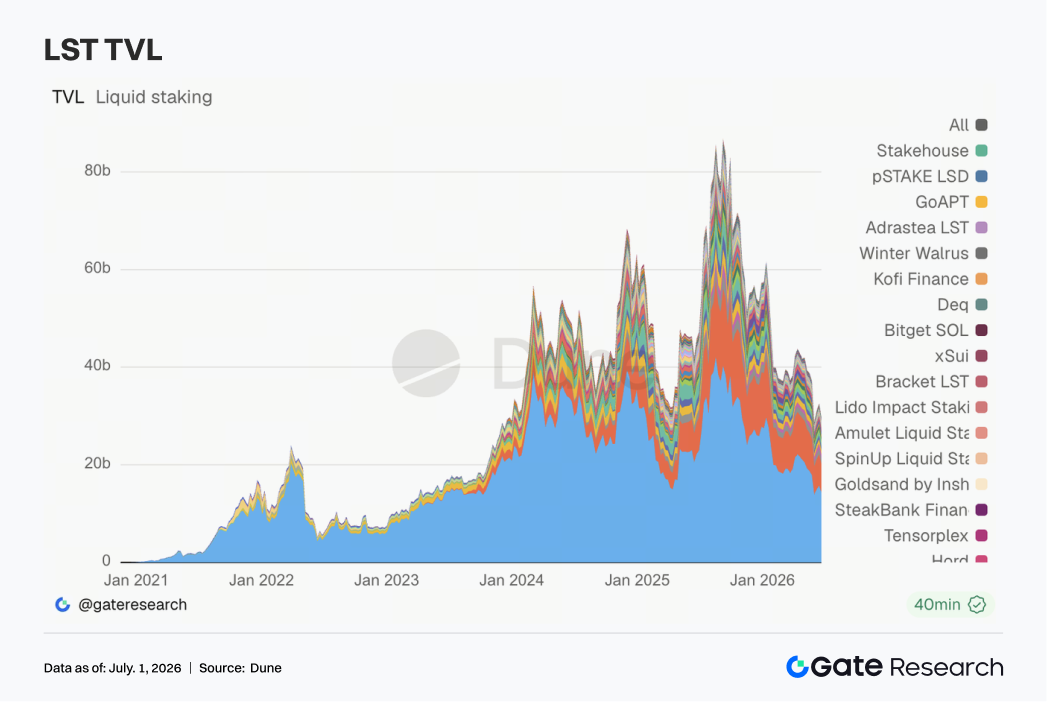

3.3 The LST Sector Pulled Back Again, and the Market's Risk Discount on Staking Assets Widened Again

The LST sector shifted from recovery in the previous week back to broad weakness. On the ETH side, Lido, Rocket Pool, and StakeWise all came under pressure, while on the SOL side, Jito and Sanctum also weakened in tandem. Because TVL is measured in U.S. dollar terms, a large part of the pullback was driven by price fluctuations in ETH and SOL, but capital preferences also did become more cautious. After the KelpDAO/rsETH incident, institutions have tiered their risk assessment of staking assets: standard LSTs, restaking assets, and cross-chain wrapped assets are no longer treated as belonging to the same risk basket. Lido's recent discussions around the cross-chain security of wstETH and Chainlink CCIP have reinforced the importance of bridge security and issuance control in LST pricing.

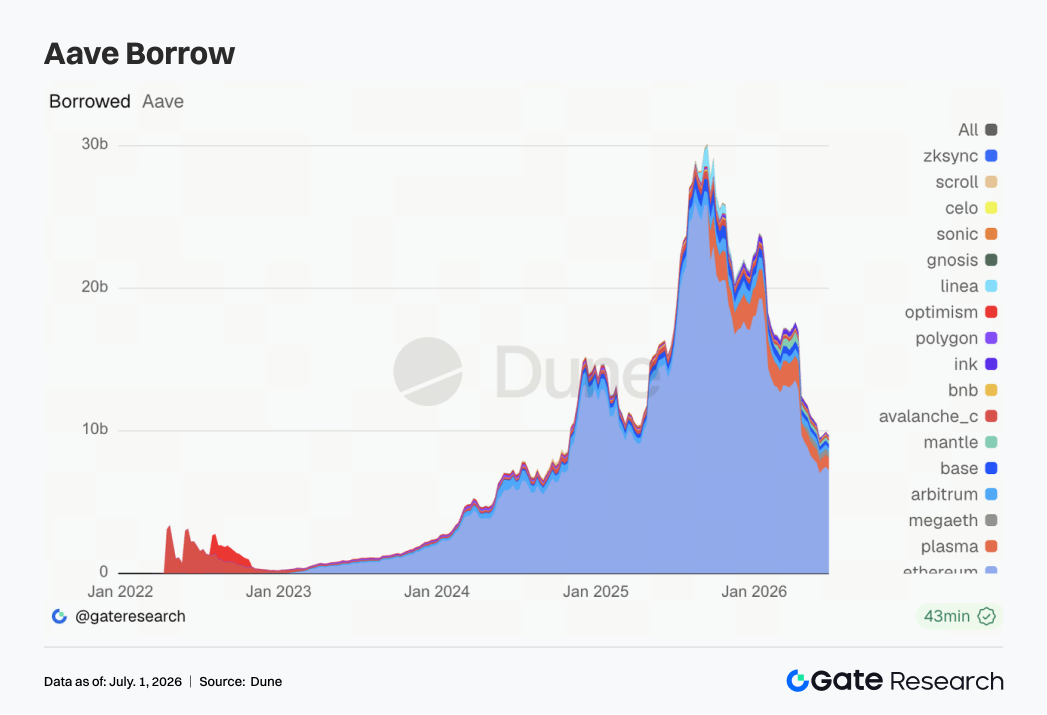

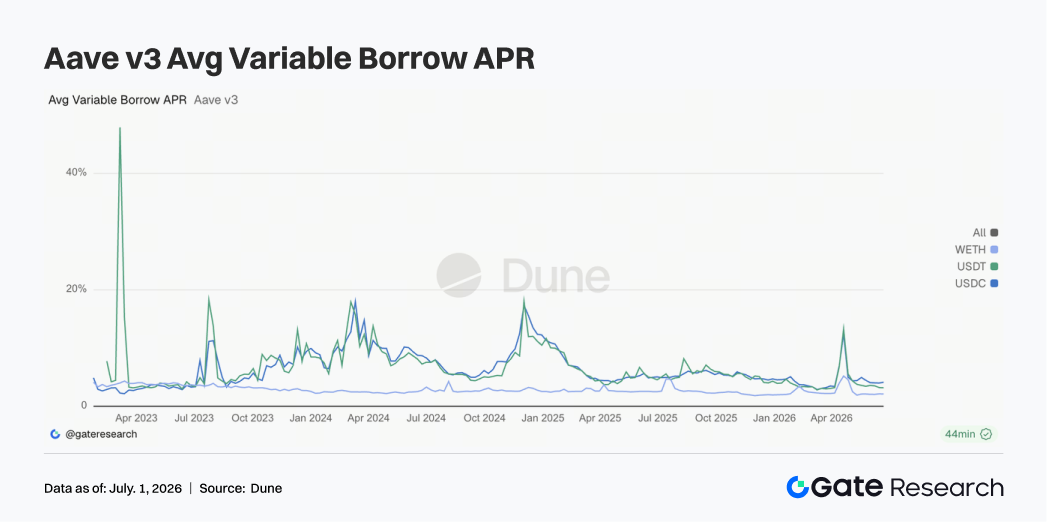

3.4 Aave Lending Balances Contracted Slightly, and Capital Still Favored Ethereum's Deepest Core Market

Aave's lending balances slipped slightly from the previous week. Ethereum's core market remained the absolute center, but it also bore most of the contraction pressure. Plasma was basically stable, Mantle improved somewhat, while MegaETH, Arbitrum, and Base were weaker. This shows that capital has not left Aave, but the pace of multi-chain expansion has clearly slowed. The aftereffects of the rsETH/KelpDAO incident are still present, making borrowers more sensitive to collateral safety, liquidation depth, and risk parameters. Aave's recent governance discussions around WETH unfreezing, USDC liquidity buffers, and the V4 Hub-and-Spoke architecture are turning this risk event into an institutional repair process. For institutions, Aave remains the core infrastructure of DeFi lending, but the short-term growth logic has shifted toward stable leverage in the main market and a repricing of the risk framework.

3.5 Core Aave Asset Rates Stayed Low but Divergent, and USDC Remained the Most Sensitive Pool

This week, borrowing rates for Aave's three core assets changed little overall. The average borrowing cost of USDC rose slightly, USDT declined, and WETH stayed at low levels. USDC's peak rate still showed brief spikes during the week, indicating that the core dollar pool remains sensitive to changes in utilization. USDT rates were more stable, and WETH did not show any obvious rush to borrow, meaning directional ETH leverage has not recovered on a large scale. This combination corresponds to a cautious funding environment. Stablecoin financing continues to be used for turnover, arbitrage, and liquidity management, but the market has not rebuilt one-sided risk exposure. Combined with Aave community discussions around USDC liquidity buffers, the protocol is actively reducing the risk of sharp rate jumps under extreme utilization. The signal from rates is milder than the signal from lending balances: panic has passed, but the memory of risk has not disappeared.

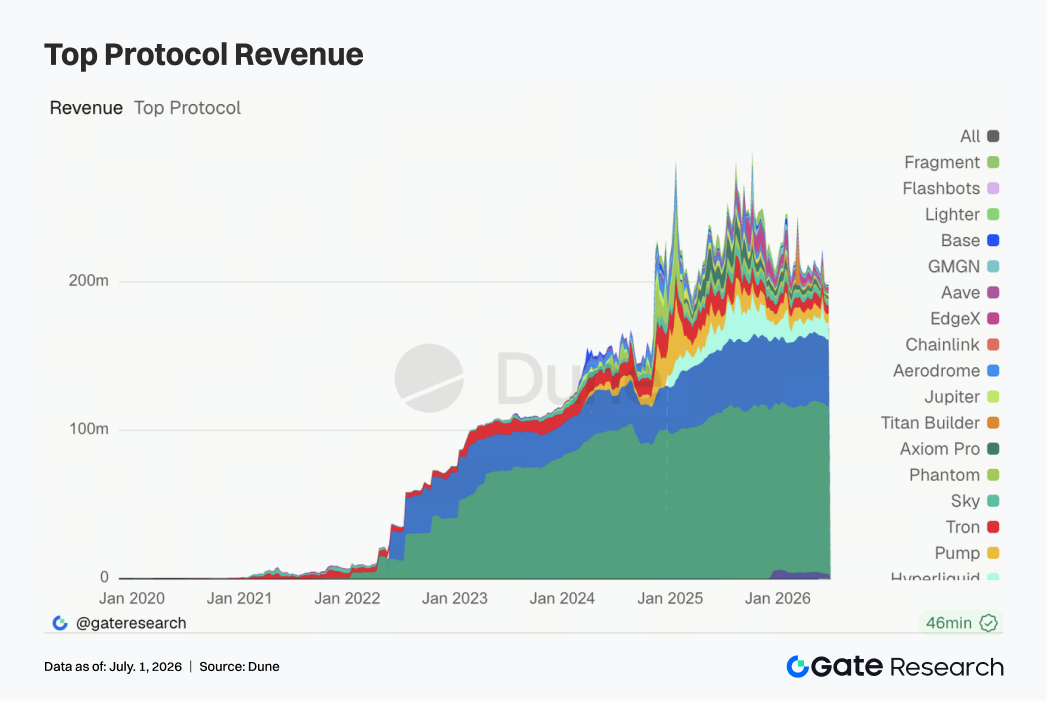

3.6 Protocol Revenue Structure Improved, with Stablecoins Providing the Base While Trading and Infrastructure Regained Elasticity

Protocol revenue had more layers this week than in the previous week. Tether and Circle remained the steadiest sources of cash flow, with little overall change. Hyperliquid Perps revenue resumed growth, showing that despite weakness in the spot market, on-chain perpetuals and high-frequency matching demand still have resilience. Solana traffic gateways such as Pump.fun, PumpSwap, Phantom, and Jupiter also recovered, echoing PumpSwap's volume expansion within the DEX space. Improvements in the revenues of Aerodrome, Base, Titan Builder, and Aave V3 suggest that revenue elasticity is spreading from pure meme-driven traffic toward matching engines, L2 trading, and lending infrastructure. On the macro side, weak Bitcoin performance, unstable ETF flows, and controversy over stablecoin regulation are suppressing broad risk appetite, but certain high-turnover segments can still generate revenue. The current main line of protocol revenue is that stablecoin issuers provide the base, while derivatives and trading infrastructure provide elasticity, and long-tail front ends still depend heavily on hot-topic traffic.

4. Derivatives Tracking

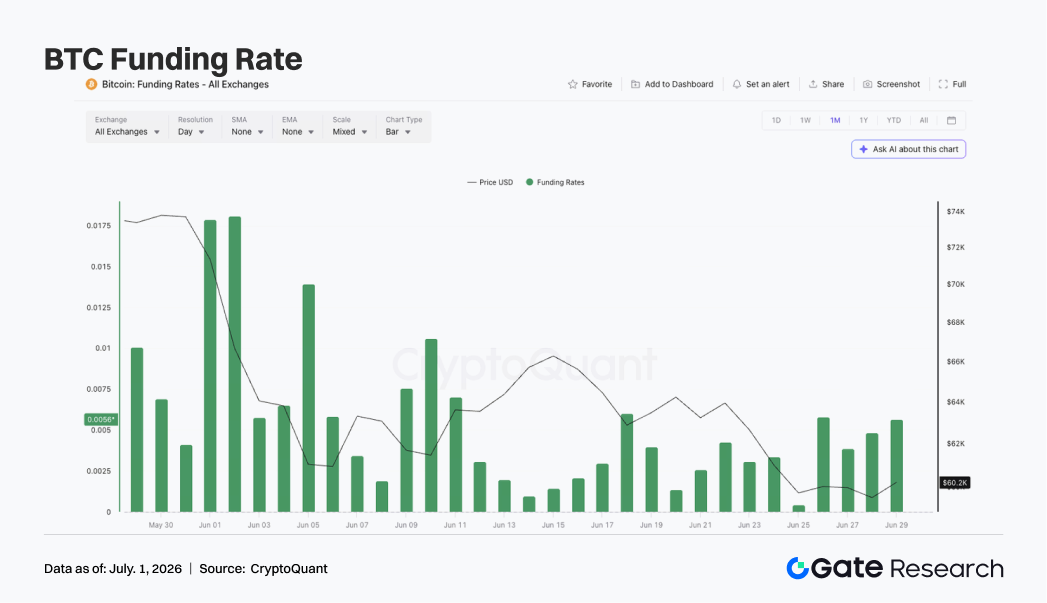

4.1 BTC Funding Rates Stayed Positive While Price Moved Lower, and Bulls Have Not Fully Exited in a Low-Leverage Environment

Last week, BTC prices generally remained in a weak and choppy pattern. Early in the week, BTC traded around $63,000-$64,000, then gradually moved lower and approached $60,000 around June 25. Although prices rebounded slightly over the weekend, BTC still remained in the $60,000-$61,000 range, and the overall rebound strength was limited.

Changes in OI were relatively restrained. Around June 22, OI was about $20.8 billion, then edged down to around $20.4-$20.5 billion and moved sideways at low levels during the week. Price fell, but OI did not expand materially, showing that this downward move was not driven by concentrated new short positioning, but was instead closer to spot-driven selling and the adjustment of existing positions in a low-leverage environment. Funding rates stayed positive throughout the week. On June 25, the funding rate briefly approached neutral, but then moved back higher from June 26 to June 28, showing that even as price fell toward $60,000, some demand for bottom-fishing longs or rebound positioning still existed in the market. The failure of funding rates to turn negative also means that the market has not yet formed an obviously crowded short structure.

Overall, the BTC derivatives market this week showed a combination of "falling prices + stable low OI + mildly positive funding rates." Lower leverage reduced the risk of extreme cascading liquidations, but bullish sentiment has not been fully flushed out. If BTC later falls below $60,000, the remaining long positions may still face further pressure. If price reclaims $62,000, however, it could support a short-term repair.

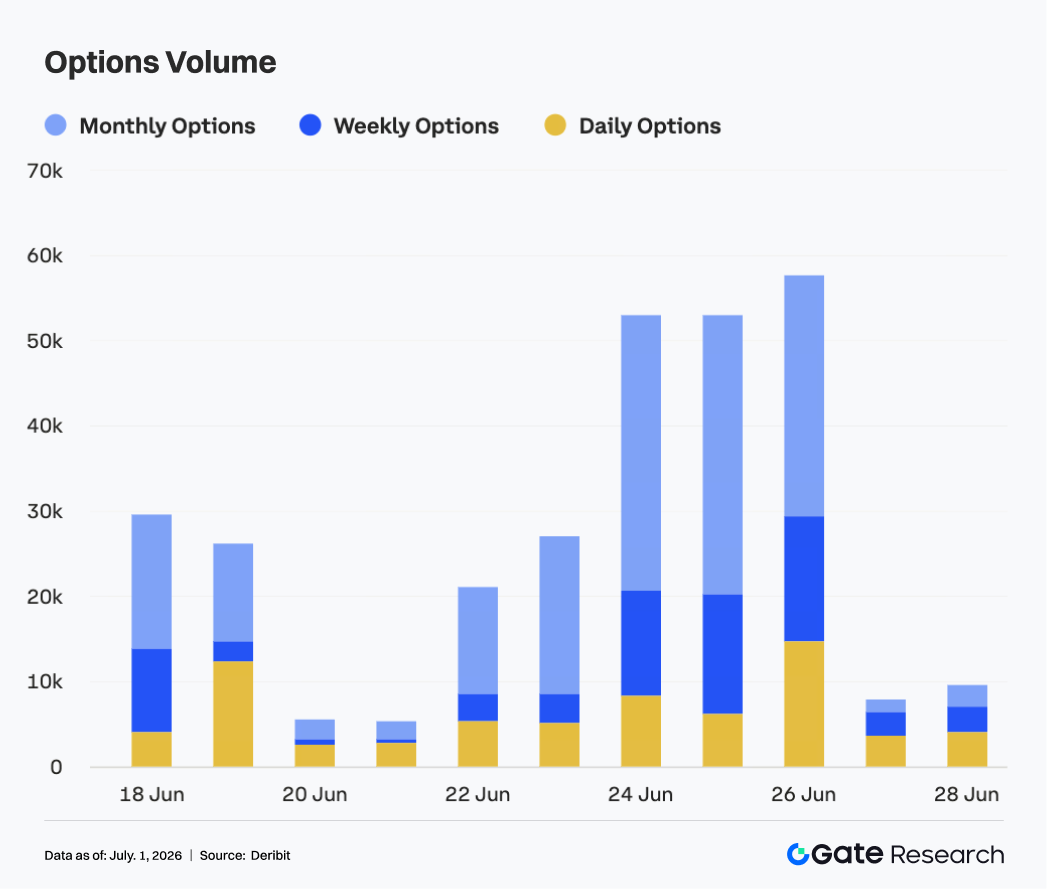

4.2 Options Volume Expanded Significantly Near Month-End, with Monthly Contracts Leading Roll Demand

The options market saw a clear increase in activity last week. From June 22 to June 23, BTC options volume remained around 20,000-30,000 contracts and was relatively stable overall. After June 24, volume rose quickly to above 50,000 contracts and reached a weekly peak near June 26, at close to 58,000 contracts.

Structurally, monthly options remained the main source of trading volume. In particular, during the expansion phase from June 24 to June 26, monthly contracts contributed most of the incremental activity. This shows that the market carried out concentrated rolling, risk management, and directional repricing around month-end expiry. Weekly options volume also rose in tandem, reflecting stronger short-term volatility trading demand. The share of daily options increased notably around June 26, indicating that as price approached a key support area, the market's demand for short-dated tools for hedging and event trading increased.

Volume fell quickly to below 10,000 contracts over the weekend, showing that after concentrated month-end rolling was completed, active trading heat cooled significantly. Overall, the expansion in options volume this week was driven more by month-end expiry and the price move lower than by sustained panic buying of protection.

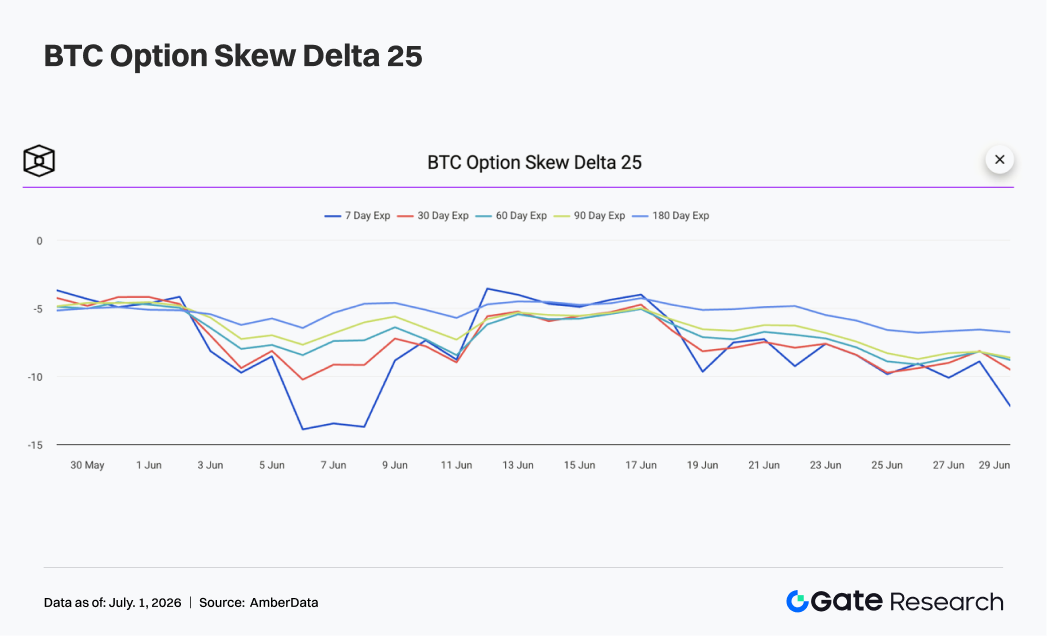

4.3 25D Skew Continued to Weaken, and Short-Dated Protection Demand Reheated

Looking at the 25D Skew curve, BTC skew across maturities remained negative overall last week and weakened further during the week. Early in the week, skew across maturities was mostly in the -6 to -8 range, showing that the market was still paying a relatively high premium for downside risk.

As BTC prices moved back toward $60,000, short-dated skew weakened clearly. Around June 25, both 7D and 30D skew approached -10, while 60D and 90D skew also moved down to around the -8 to -9 range, showing that demand for protection spread from short maturities into medium maturities. Compared with previous weeks, the feature of this week's skew was not a one-day extreme drop, but rather its persistent stay in a defensive zone. Volatility in 7D skew remained the strongest, reflecting that short-term traders remained highly sensitive to a break below $60,000. Medium- and long-dated skew was relatively more stable, but it also did not show a clear repair.

Overall, this week's skew structure shows that market defensiveness strengthened further. If BTC can hold $60,000 and move back above $62,000, short-dated skew may be the first to recover. If price breaks below $60,000, protective buying may continue to lift put-option premiums.

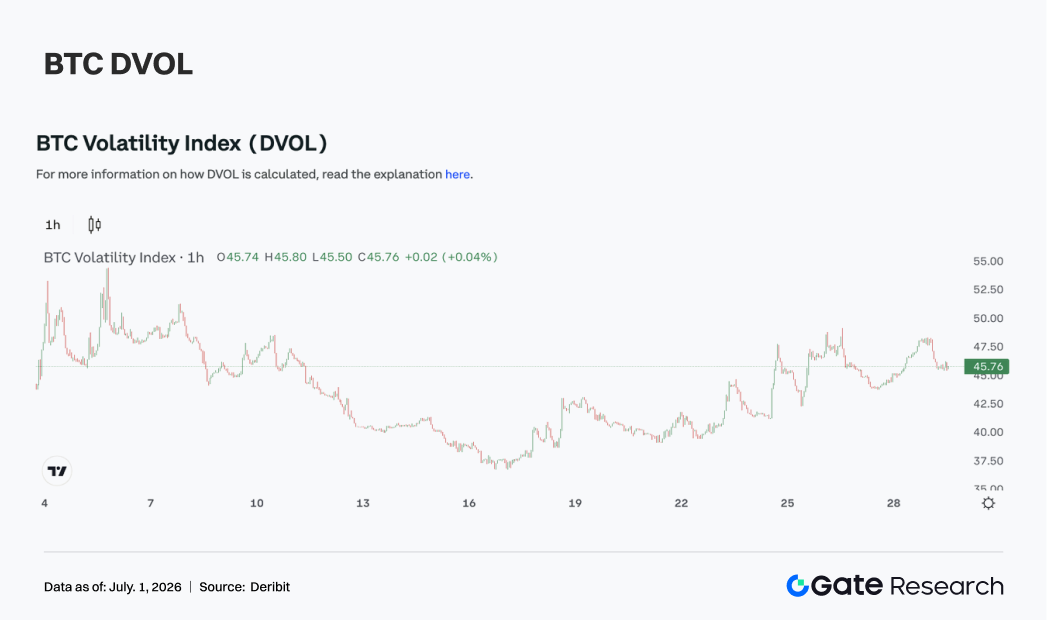

4.4 DVOL Rose Clearly, and the Market Repriced Downside Volatility Risk

In terms of volatility, BTC's volatility index DVOL rose clearly last week. Early in the week, DVOL still hovered around 40, then gradually moved higher along with the price decline and the expansion in options volume, reaching the 47-48 range around June 25 to June 26.

This rise in DVOL corroborated the move of price toward $60,000, weaker skew, and larger options volume, showing that the market has started to reprice downside volatility. Compared with the low-level consolidation of the previous week, volatility risk premium rose clearly this week, and the derivatives market became more sensitive to short-term directional breaks.

However, although DVOL rose, it did not break above previous extreme highs, showing that the market has still not entered a full panic state. OI remained low, which also means liquidation pressure from leverage is relatively controllable. The rise in volatility came more from protection demand and month-end rolling than from large-scale forced liquidations.

Overall, BTC is currently in a state of "price near key support + defensive skew + rising DVOL." If price continues to fluctuate around $60,000, DVOL may remain near 45. If a directional breakdown or a rapid rebound occurs, volatility could still expand further.

5. Outlook

Data Sources:

- Investing, https://investing.com/currencies/xau-usd-historical-data

- Gate, https://www.gate.com/trade/BTC_USDT

- CMC, https://coinmarketcap.com/real-world-assets/?type=all-tokens

- Coinglass, https://www.coinglass.com/pro/depth-delta

- Dune, https://dune.com/gateresearch/gate-tradfi#weekly-volume

- Dune, https://dune.com/gateresearch/gate-institutional-weekly-report

- Bybit, https://www.bybit.com/future-activity/en/tradfi

- Bitget, https://www.bitgettradfi.com/tradfi/XAUUSD

- CryptoQuant, https://cryptoquant.com/asset/btc/chart/derivatives

- Amberdata, https://pro.amberdata.io/options/deribit/btc/current/

Gate Research is a comprehensive blockchain and cryptocurrency research platform that provides deep content for readers, including technical analysis, market insights, industry research, trend forecasting, and macroeconomic policy analysis.

Disclaimer

Investing in cryptocurrency markets involves high risk. Users are advised to conduct their own research and fully understand the nature of the assets and products before making any investment decisions. Gate is not responsible for any losses or damages arising from such decisions.