The core takeaway from this set of data is: How far can AI chip demand carry the semiconductor industry? This article will analyze it across five dimensions: demand logic, supply chain transmission, industry chain signals, cycle judgment, and risk warnings.

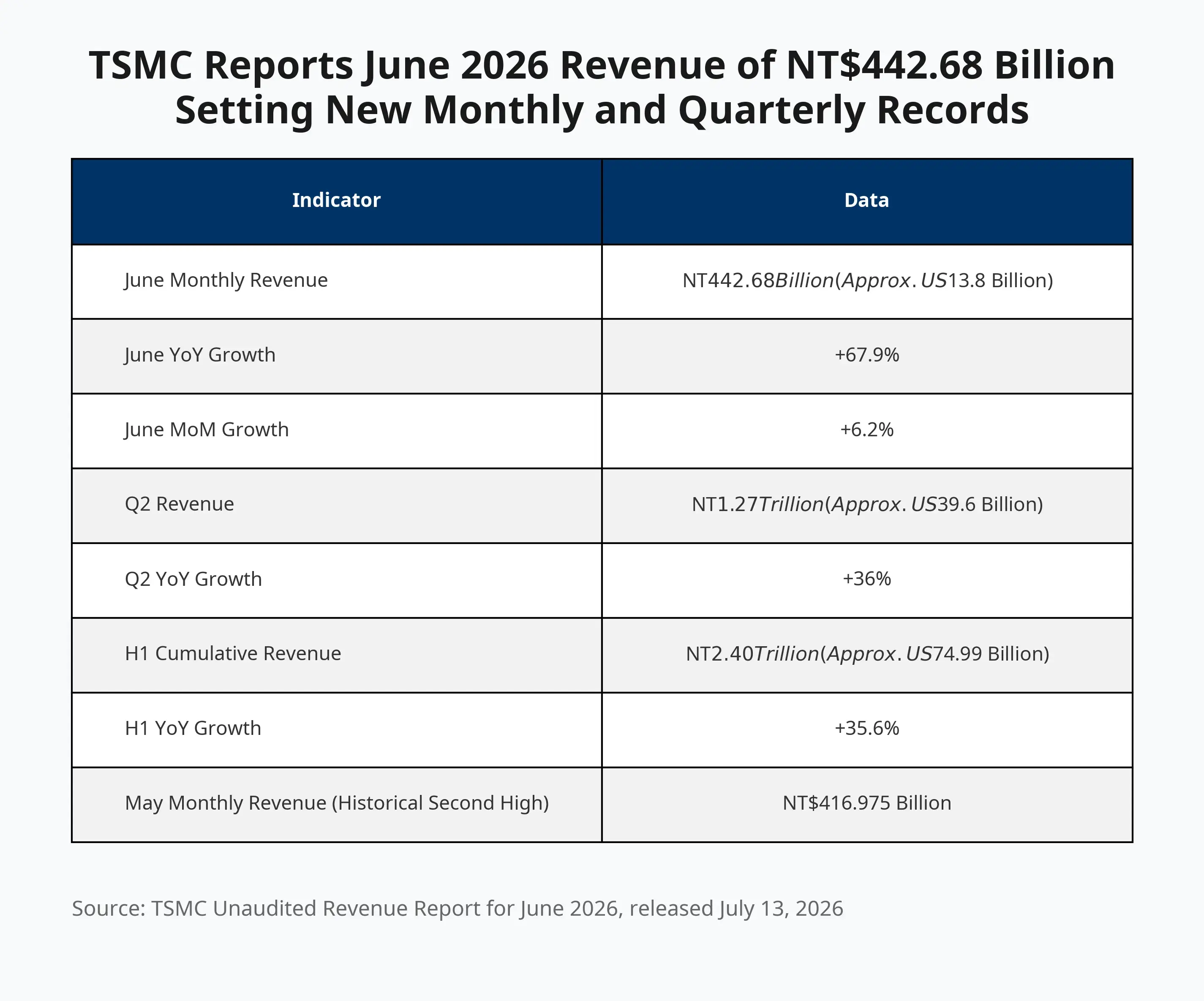

TSMC’s June 2026 revenue exceeds NT$442.68 billion—record year-over-year and quarter-over-quarter highs for the month and quarter

Why did TSMC revenue accelerate suddenly in June?

The 67.9% year-over-year growth in June revenue marked the fastest monthly increase this year, surpassing May’s previous record of NT$416.975 billion. Second-quarter revenue reached NT$1.27 trillion (about $3.96 billion), up 36% year over year—aligned with analysts’ average expectations.

The main driver of this growth is demand for AI chips. TSMC manufactures AI GPUs, AI accelerators, and high-performance computing (HPC) chips for customers including Nvidia (NVDA.US), AMD (AMD.US), and Apple. Tech companies such as OpenAI, Meta, Google, and Amazon continue to expand spending on AI infrastructure; cloud providers are increasing GPU purchases, which in turn drives rising chip manufacturing demand.

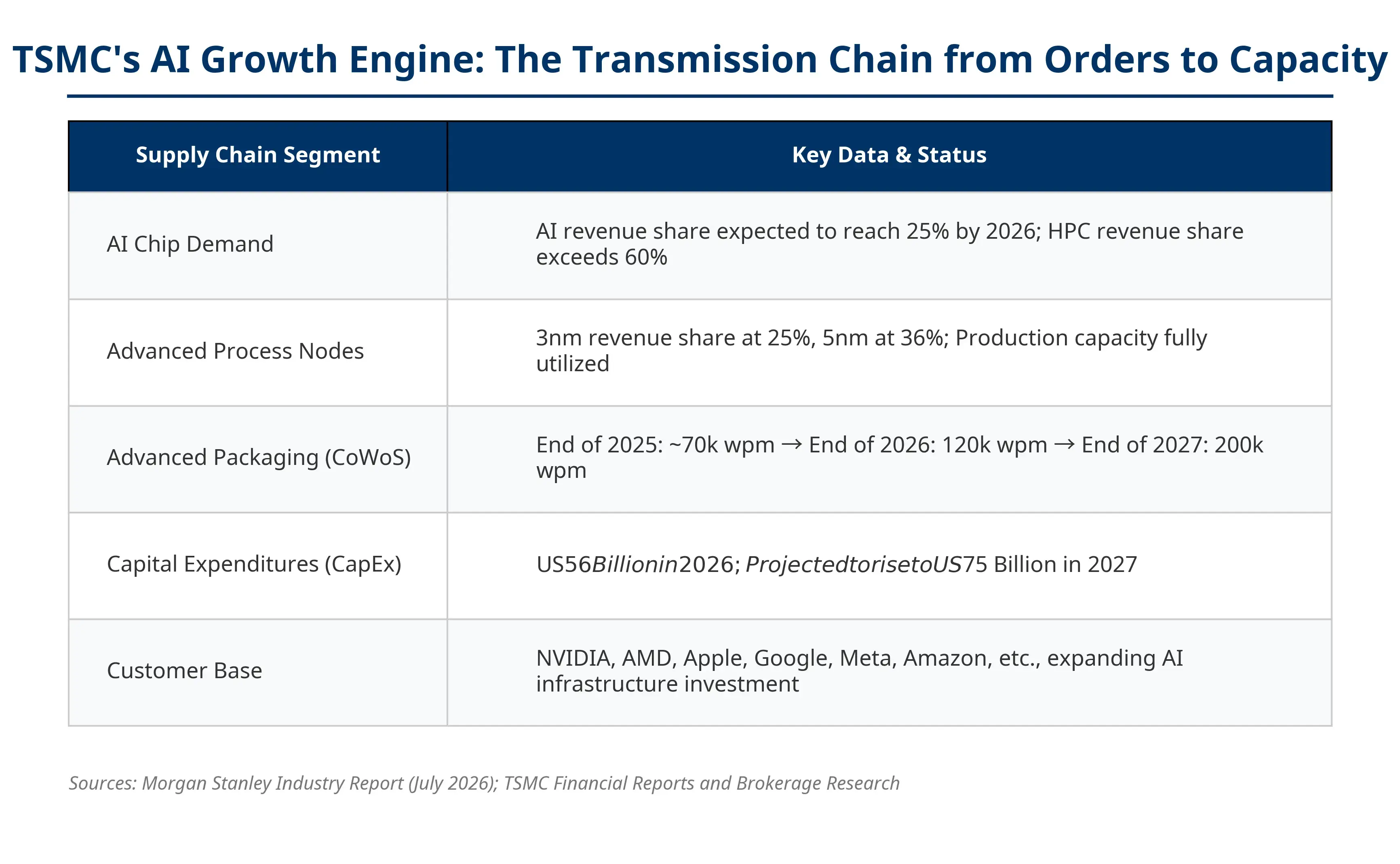

TSMC holds a 73% share in the global pure-play foundry market (data for Q1 2026). Its performance is widely viewed as a barometer for the global AI industry chain. When advanced-node capacity (3-nanometer and 5-nanometer) at TSMC remains fully utilized, it indicates strong demand for downstream AI chips. From AI GPUs to advanced-node wafers, and then to CoWoS advanced packaging and AI servers, TSMC is positioned at a core node in this chain.

It’s also worth noting that TSMC’s explosive growth in June is not an isolated event. The company plans to add two advanced packaging plants in the Chiayi Science Park in southern Taiwan— the first has already entered mass production, and the second is about to start operations. The ongoing expansion of advanced packaging capacity indirectly confirms the visibility and durability of AI chip orders.

TSMC’s AI growth engine in full—an order-to-capacity transmission chain

What does TSMC’s growth mean for Nvidia and AI stocks?

For equity investors, TSMC’s revenue data is an important leading indicator for assessing the health of the AI industry chain.

For Nvidia, continued growth in TSMC orders indicates that demand for AI GPUs remains strong. If wafer capacity remains tight, it will support Nvidia’s revenue growth expectations. On July 13 (Beijing time), Nvidia’s after-hours trading declined 1.74% to $207.29. Semiconductor stocks overall were under pressure, as market concerns about slower growth in AI compute demand continued to build. TSMC’s June data, to some extent, provides evidence that near-term demand remains solid.

For AMD, its MI-series AI chips also rely on TSMC’s advanced processes. Improvements in TSMC’s capacity help AMD expand its supply of AI chips. Top investment banks have recently raised their price targets for AMD in quick succession: Goldman Sachs raised its target from $450 to $640, and Wells Fargo raised it to $615; UBS increased its target to $670.

Broader beneficiaries also include semiconductor equipment makers (such as Applied Materials and Lam Research), memory chip companies (such as SK Hynix and Micron), and data-center-related firms (such as Broadcom). TSMC’s planned 2026 capital expenditures are close to a record $56 billion, which will directly boost demand for upstream equipment.

However, semiconductor stocks faced broad pre-market pressure on July 13 (Beijing time)—Marvell fell 1.9% to $3.10, Intel dropped nearly 5%, and Lam Research slid 3.6%—reflecting that the market is already digesting other macro factors beyond TSMC’s positive news, including the suppressive impact of tensions between the US and Iran on risk assets.

Is a semiconductor supercycle forming?

This is the most central debate in the market right now. To answer this question, we need to compare structural differences between historical cycles and the current cycle.

In the past, semiconductor supercycles were driven by PC demand, smartphone adoption, and the growth of mobile internet. The key characteristic was a surge in terminal demand driven by the consumer upgrade cycle. The current cycle is driven by corporate capital expenditures—tech giants investing in data centers for AI infrastructure, GPU clusters, and model training costs.

Arguments supporting the continuation of a supercycle include: First, AI capital expenditures remain elevated. Tech giants invest hundreds of billions of dollars annually in AI equipment purchases, with a substantial portion supported by borrowing. Second, supply and demand for high-end chips remains tight. 3-nanometer and 5-nanometer advanced processes and CoWoS advanced packaging are still capacity bottlenecks. Last month, TSMC CEO Wei Zhe-jia warned that even if new US capacity comes online in the coming years, the company may still not be able to fully satisfy US customer demand. SK Hynix executives also believe the current memory-chip shortage could last beyond 2030.

However, simply analogizing the current cycle to previous supercycles may lead to misjudgment. The sustainability of corporate capital expenditures depends on whether AI commercialization can generate returns that match the investment—this is fundamentally different from natural demand growth driven by consumer upgrade cycles. Bloomberg Intelligence analysts pointed out that demand for AI accelerators and server CPUs keeps 3-nanometer and 5-nanometer capacity tight, but whether gross margins can be sustained near the upper end of guidance depends on whether high full utilization of advanced-node capacity can continue to offset the dilution effect from overseas plants.

What should investors be wary of?

No industry analysis can avoid risks. Behind the market’s high expectations for semiconductors and AI stocks are at least three verifiable risk factors.

Will AI capital expenditures peak? This is the biggest question in the market. Companies invest huge sums to build AI infrastructure, but will the returns from AI commercialization match the spending? If AI revenue growth falls short of expectations, chip stock valuations could face systemic pressure. The market’s focus has shifted from “whether AI will grow” to “whether AI investment can generate returns.”

Semiconductor inventory cycle risk. The chip industry historically exhibits clear cyclicality: demand overheats → capacity expansion → inventory accumulation → demand cools → inventory correction. With wafer-fab capacity at players such as TSMC operating at full utilization, once the growth rate of AI demand shows signs of slowdown, the risk of inventory correction could rise quickly.

Geopolitical risk. More than 70% of TSMC’s capacity is concentrated in Taiwan. Any escalation of regional tensions could disrupt global semiconductor supply chains. Additionally, changes to US policies on semiconductor export controls to China are an ongoing source of uncertainty.

Key items to watch in TSMC’s July 16 earnings report. Investors should focus on three metrics: whether the full-year revenue growth guidance exceeds 30% (TSMC previously expected its full-year US dollar revenue to grow by more than 30%); whether the capital expenditure plan continues to increase; and whether the share of AI-related revenue continues to rise—indicating whether AI is becoming a long-term growth engine rather than a short-term catalyst.

The global tech stock chain reaction

TSMC’s revenue growth validates the reality of AI demand, which boosts the market’s overall confidence in the AI industry chain. Across the chain—from AI chips to semiconductor equipment, from memory chips to cloud computing infrastructure—sentiment is reinforced by TSMC’s data.

But that doesn’t mean all related stocks will rise in sync. The market has entered a phase of differentiation: companies with clear paths to profitability and reasonable valuations are favored, while concept-driven names face greater valuation reset pressures.

With a 73% share in the global pure-play foundry market and record quarterly revenue, TSMC has sent a clear signal: demand for AI hardware is still expanding. But whether a supercycle truly exists ultimately depends on whether AI commercialization can continuously support corporate capital expenditures—this takes time and more data to confirm.

FAQ

Why did TSMC’s June revenue grow 68% year over year?

Mainly driven by demand for AI chips. TSMC produces AI GPUs, AI accelerators, and high-performance computing chips for customers including Nvidia, AMD, and Apple. Global tech giants are continuing to expand investment in AI infrastructure, leading to a significant increase in GPU purchases and foundry outsourcing demand.

What does TSMC’s revenue growth mean for Nvidia stock?

TSMC is a major foundry for Nvidia GPUs, and its order growth directly reflects that AI GPU demand remains strong. Ongoing tight wafer capacity will support Nvidia’s revenue growth expectations. However, on July 13, Nvidia’s after-hours trading fell 1.74% to $207.29, indicating the market is considering other macro factors.

Has a semiconductor supercycle really arrived?

The current cycle is driven by corporate AI capital expenditures, which is fundamentally different from past cycles driven by consumer upgrade demand. Supporting factors include high AI spending and capacity constraints in advanced processes; risks involve whether AI commercialization returns can match the investments. More data is needed to confirm if a supercycle is truly underway.

What should investors watch in TSMC’s July 16 earnings report?

Focus on three indicators: whether full-year revenue guidance exceeds 30%, whether capital expenditures continue to rise, and whether AI-related revenue share increases. These will indicate if AI chip demand can sustain long-term growth for TSMC.

What risks are associated with investing in semiconductor stocks?

Key risks include: potential peaking of AI capital expenditures, inventory cycle adjustments inherent to the industry, and geopolitical factors affecting supply chains. Investors should assess whether the returns from AI commercialization can justify the massive investments.