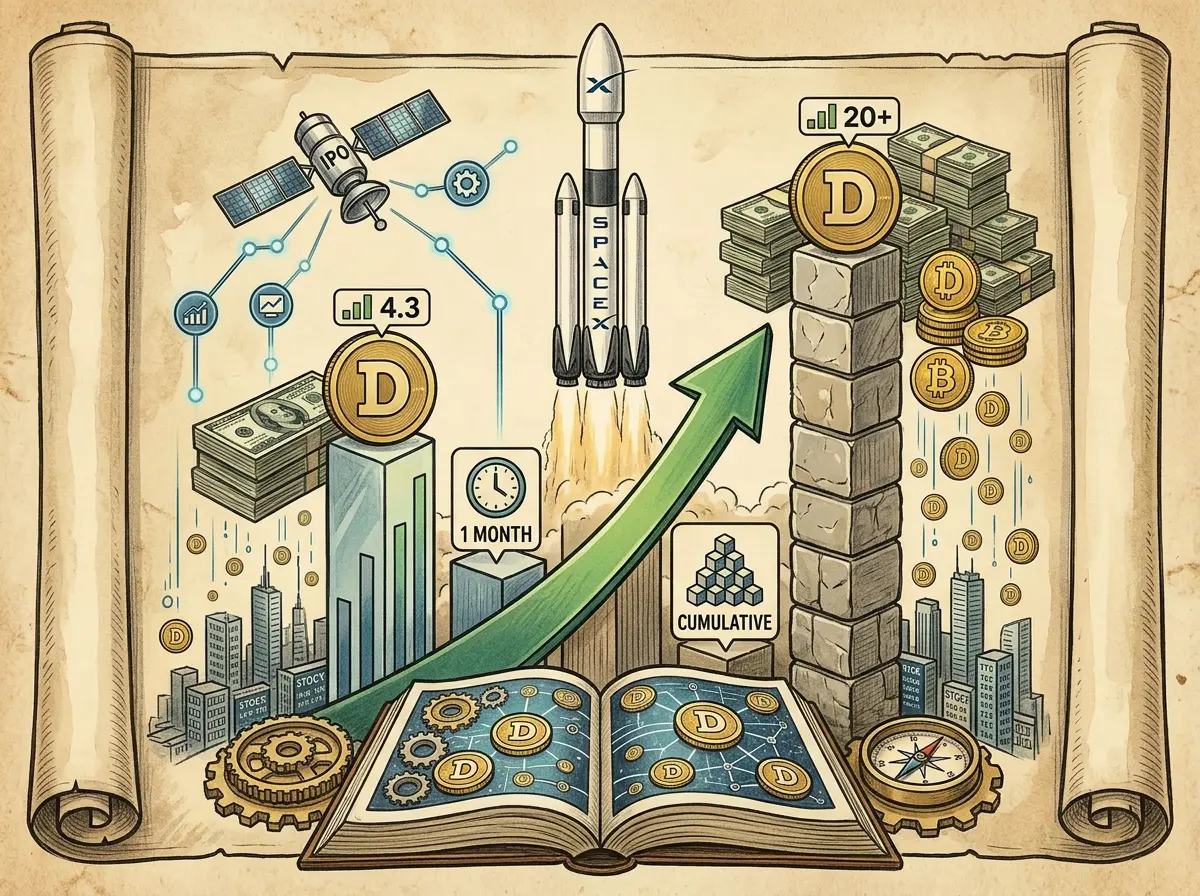

Capital Markets Commentator Journal Kobeissi Letter posted on X on June 17. Over the past 30 days, on-chain tokenized stock trading volume reached $4.3 billion, and the cumulative transferred volume of tokenized stocks first exceeded $20 billion. The main catalyst driving this round of growth was the SpaceX IPO: on June 15, tokenized stocks on Solana saw their first 24-hour spot trading volume exceed $100 million.

Three numerical milestones of Kobeissi Letter

Based on Kobeissi Letter’s confirmed figures from its X platform post: over the past 30 days, on-chain tokenized stock trading volume was $4.3 billion (a monthly historical high), with year-over-year growth of over 140%; on June 15, Solana’s single-day spot trading volume first surpassed $100 million; and cumulative transferred volume first exceeded $20 billion.

Solana accounted for 99% of all on-chain tokenized SpaceX trading volume at its peak, with Jupiter leading in trading volume as a venue. The complete statement from Kobeissi Letter reads: “Tokenization is accelerating.”

Participation models across platforms for the SpaceX IPO and refund events

According to the整理 from the original text, the participation models confirmed by each platform fall into two categories: pre-IPO/subscription (Kraken, Bybit, Binance Wallet, Bitget Wallet, and MEXC mainly use the xStocks SPCXx to open subscription or an expression-of-interest channel; users must additionally pay about a 5% price spread or underwriting fees); and pre-market trading, perpetual contracts, or synthetic trading (no actual stock settlement is provided, mainly used for price discovery and derivatives trading).

Because the underlying stock allocation was insufficient, platforms including Bybit, Binance Wallet, and Bitget Wallet ultimately canceled the related subscriptions or issued full refunds. Gate participated through direct IPO subscription and linked the IPO allocation to the subsequent U.S. stock trading account.

Confirmed structure differences between tokenized stocks and real stocks

The author of the original text confirmed that pre-IPO tokenized products can be simplified by users to “buy SpaceX stock on-chain,” but the actual structure is not the same as directly holding Nasdaq-listed stocks. The specific differences include: what users submit may be a subscription intent (not a guaranteed allocation); what they receive may be tokenized certificates or price exposure, not full shareholder rights; and before listing and for perpetual products, the focus is trading and price discovery, with no actual stock settlement.

For this round’s SpaceX case, it also confirms that tokenized stocks can lower users’ participation thresholds, but they cannot bypass the core limitations of traditional IPOs: the initial allocation of high-quality assets still depends on the underwriting system, custody arrangements, and upstream supply.

Common questions

What is the source for the figure that on-chain tokenized stock cumulative transfers exceeded $20 billion?

According to the confirmation that Kobeissi Letter posted on X on June 17, 2026, the cumulative transfer volume of on-chain tokenized stocks first exceeded $20 billion. Kobeissi Letter is a capital markets commentary journal, and its X platform post is the first-hand source for this report.

Why did platforms such as Bybit and Binance Wallet ultimately refund?

According to the original text, after each platform simultaneously opened subscription channels for this round of IPO, front-end subscription volumes accumulated quickly, but some platforms ultimately could not obtain enough underlying SpaceX share allocation, leading to cancellation of the related subscriptions or full refunds. This reflects the structural limitation that the front-end subscription demand for tokenized stocks can be amplified quickly, but the supply of underlying real assets cannot expand in sync.

What does the 99% peak share for Solana mean?

According to the confirmed data from Kobeissi Letter, after the SpaceX IPO on June 15, Solana accounted for 99% of all on-chain trading volume in tokenized SpaceX at its peak, while Jupiter was the leading venue by trading volume. This reflects that SpaceX tokenized trading is highly concentrated within the Solana ecosystem. Hyperliquid’s HIP-3 perpetual contract (previously confirmed in earlier reporting) is another major channel, but it is for derivatives rather than spot.