On July 2, 2026, Metaplanet (stock code: 3350), a company listed on the Tokyo Stock Exchange in Japan, disclosed its Bitcoin holdings data for the second quarter of fiscal 2026. According to regulatory filings, the company purchased 2,823 Bitcoin at an average price of approximately $88,300 per coin in the second quarter. This acquisition, worth about $170.7 million, brought its total holdings to 43,000 BTC, with a market value of approximately $2.6 billion. As of July 3, 2026, according to Gate market data, Bitcoin was trading at around $61,779, with a total market cap of about $1.23 trillion, and Metaplanet's holdings accounted for approximately 0.205%.

This data means Metaplanet has surpassed US Bitcoin miner MARA Holdings, which holds 36,303 BTC, officially becoming the world's third-largest publicly traded company by Bitcoin holdings. Currently, it trails only Strategy (formerly MicroStrategy) and Twenty One Capital, and the gap to second place is just 514 Bitcoin.

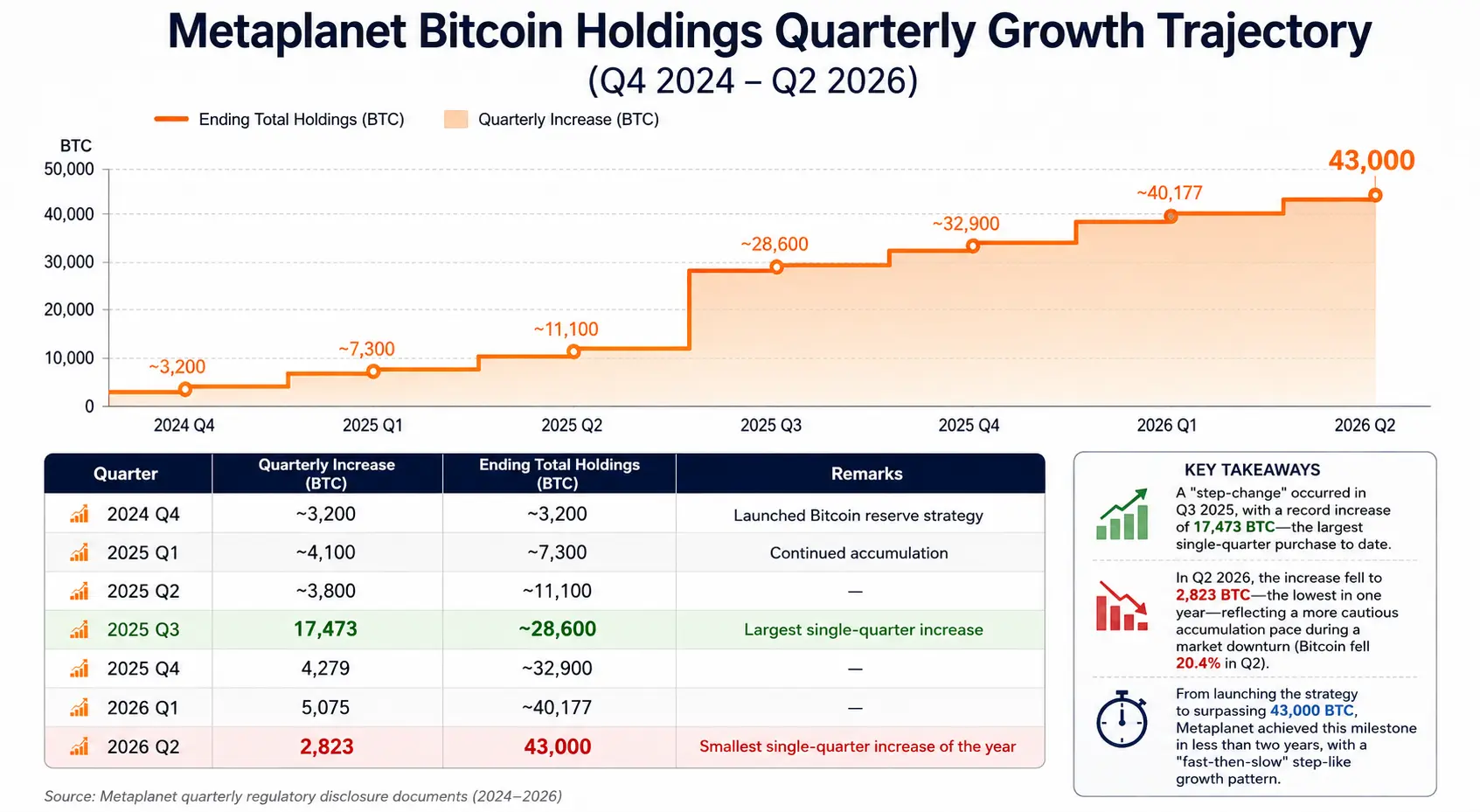

Since initiating its Bitcoin reserve strategy in 2024, Metaplanet has accumulated from zero to 43,000 BTC in less than two years, with a clear quarterly acquisition trajectory: 17,473 BTC purchased in Q3 2025, 4,279 BTC in Q4 2025, 5,075 BTC in Q1 2026, and 2,823 BTC in Q2 2026. The company's management has an even more aggressive target: to accumulate 100,000 BTC by the end of 2026 and reach 210,000 BTC by the end of 2027.

Metaplanet's rapid rise is not an isolated event. It reflects a broader trend: an increasing number of publicly traded companies are incorporating Bitcoin into their balance sheets as a strategic reserve asset. This phenomenon is reshaping the paradigm of global corporate financial management and exerting a profound impact on the supply-demand structure of the Bitcoin market.

Metaplanet's Latest Accumulation: Data Breakdown and Financial Structure

Metaplanet's second-quarter accumulation warrants detailed examination across multiple dimensions.

From a purchase price perspective, the company's average cost per coin in Q2 was approximately $88,300, lower than its overall average cost basis of $106,500. This means the latest round of accumulation helped lower the overall cost basis—the previous average cost was around $107,700, which has now dropped to roughly $106,500 after this purchase. In a market environment where Bitcoin fell from $73,580 to $58,558 in Q2, a decline of 20.4%, Metaplanet's decision to continue buying during the downturn represents a contrarian positioning strategy.

From a financing structure standpoint, the funds for this accumulation mainly came from credit facility borrowings and bond issuances, without any new share issuance, thus avoiding direct dilution of shareholder equity. According to the company's disclosure, its total debt and preferred stock account for approximately 23% of its overall capital structure. As of June 30, Metaplanet's Bitcoin holdings had a book value of approximately ¥409 billion (about $2.5 billion), while the cumulative purchase cost was about ¥659 billion (roughly $4.07 billion), resulting in an unrealized book loss of approximately ¥250 billion.

Notably, Metaplanet also operates a "Bitcoin yield generation business," which generates premium income through strategies such as selling Bitcoin cash-covered call options. In the second quarter of fiscal 2026, this business generated revenue of approximately $10.95 million (¥1.747 billion), with cumulative revenue of about $29.3 million (¥4.717 billion) in the first half of the fiscal year. The company reported a Q2 Bitcoin Yield (BTC Yield) of 6.6%. This metric reflects whether the growth rate of total Bitcoin holdings outpaces shareholder dilution during equity or convertible bond financing—a core quantitative indicator for evaluating shareholder value dilution for companies operating on a Bitcoin reserve model.

Metaplanet Bitcoin Holdings Quarterly Growth Trajectory (Q4 2024 – Q2 2026)

Global Corporate Bitcoin Holdings Ranking: Landscape and Changes

With Metaplanet's rapid ascent, the top-tier landscape of global public company Bitcoin holdings is undergoing restructuring.

According to BitcoinTreasuries.net and multiple data platforms, as of July 2, 2026, the top three public companies by Bitcoin holdings are as follows:

Number 1: Strategy (formerly MicroStrategy) , holding approximately 847,363 Bitcoin, about 4% of the total Bitcoin supply of 21 million. Since 2020, the company has continuously financed purchases through stock and convertible bond issuances, making it the pioneer and largest practitioner of the corporate Bitcoin reserve model globally.

Number 2: Twenty One Capital , holding approximately 43,514 Bitcoin, with a slim lead of about 514 Bitcoin over Metaplanet. The gap between them is equivalent to roughly $30 million at current market prices, and the ranking change next quarter depends almost entirely on the accumulation pace of both parties.

Number 3: Metaplanet , holding 43,000 Bitcoin, accounting for approximately 0.205% of the total Bitcoin supply.

Number 4: MARA Holdings , holding approximately 36,303 Bitcoin. This US Bitcoin mining company had long been in the global top three but has been overtaken by Metaplanet's continued accumulation.

Source: BitcoinTreasuries.net

The dynamic changes in rankings reflect a divergence in corporate strategic choices. While Metaplanet continues to increase its holdings, some previously holding companies are exiting. Nasdaq-listed K Wave Media filed with the SEC in the first week of July to sell all 88 Bitcoin holdings and repay approximately $6 million in debt. French company Sequans Communications announced in May that it would gradually liquidate its remaining 658 Bitcoin. Strategy also paused its regular weekly purchasing plan in late June and introduced a new capital management framework.

The continued buying by top companies and the orderly exit by tail-end companies together form the complete picture of the current corporate Bitcoin reserve ecosystem—it is not a one-way "buying race," but a differentiated decision-making matrix based on each company's capital structure, financing costs, and risk appetite.

Why Are More Listed Companies Allocating to Bitcoin?

The drivers for listed companies to include Bitcoin on their balance sheets can be understood from three layers: financial logic, strategic logic, and institutional logic.

Financial Logic: Hedging against fiat depreciation and optimizing capital allocation. Since 2020, monetary easing policies and inflationary pressures in major global economies have exposed companies holding large cash reserves to the risk of diminished purchasing power. Bitcoin's fixed supply cap of 21 million gives it anti-dilution properties, leading some firms to view it as "digital gold" to replace part of their cash reserves. As Bernstein noted in its mid-2026 report, despite net outflows from Bitcoin spot ETFs, corporate treasuries continue to buy, meaning the long-term "store of value" narrative for Bitcoin has not been weakened.

Strategic Logic: Differentiated competition and brand narrative. For a listed company like Metaplanet, becoming "Asia's first public Bitcoin treasury company" itself constitutes a unique market positioning. This strategic narrative helps attract a specific investor group—those who want indirect exposure to Bitcoin price volatility but prefer not to hold directly or allocate via ETFs. Michael Saylor congratulated Metaplanet after it broke the 43,000 BTC mark, saying: "You are proving that the Bitcoin reserve strategy is global." This statement highlights the demonstration effect and brand value of such a strategy.

Institutional Logic: Evolution of accounting standards and regulatory environment. The cryptocurrency accounting standards update (ASU 2023-08) issued by the US Financial Accounting Standards Board (FASB) at the end of 2023 requires companies holding crypto assets to use fair value measurement, changing the previous accounting treatment where impairment could not be reversed. The new rules allow companies to recognize unrealized gains in financial reports when Bitcoin prices rise, reducing the financial reporting cost of including Bitcoin on the balance sheet. This institutional change lowers the accounting threshold for corporate Bitcoin allocation and is one of the underlying institutional factors driving more listed companies to follow suit.

Advantages and Risks of the Corporate Bitcoin Reserve Model

The Bitcoin reserve model offers unique strategic advantages to companies, but it also comes with structural risks that cannot be ignored.

Advantages

Balance sheet diversification and inflation hedging. Including Bitcoin on the balance sheet means a company's reserve assets no longer rely solely on fiat cash or short-term Treasuries. Bitcoin's decentralized nature and fixed supply cap provide potential hedging functions during fiat depreciation cycles.

Financing convenience and market premium. Pioneers like Strategy have demonstrated that "holding Bitcoin" itself can become a financing narrative—companies can raise funds through stock or convertible bond issuance to buy Bitcoin, and the market is sometimes willing to pay a premium (the so-called mNAV premium) for this strategy. Although this premium has significantly narrowed in 2026, for companies still in the accumulation phase, opening such financing channels is inherently strategically valuable.

Synergy with yield generation businesses. Metaplanet's case shows that companies holding large Bitcoin spot positions can generate additional operating income through options strategies. The company's Q2 options income of $10.95 million effectively lowered the actual cost of that quarter's accumulation. This "hold + yield" dual-track model is becoming a standardized operational framework for Bitcoin reserve companies.

Risks

Balance sheet risk from price volatility. This is the most direct and quantifiable risk. The high volatility of Bitcoin prices means the value of Bitcoin holdings on a company's balance sheet can fluctuate significantly in the short term. In the June 2026 market downturn, the total market value of corporate Bitcoin treasury holders evaporated by approximately $62 billion. Metaplanet itself faces this issue—as of June 30, its holdings' market value (about $2.5 billion) was significantly below its cumulative purchase cost (about $4.07 billion).

Leverage accumulation and financing cost pressure. Most Bitcoin reserve companies rely on debt or equity financing for expansion. Strategy carries about $6.7 billion in convertible bonds and $15.5 billion in perpetual preferred stock, with annual interest payment obligations of approximately $1.712 billion. When Bitcoin prices fall, these fixed interest expenses do not decrease, while the company's net asset value shrinks, creating a two-way squeeze. JPMorgan analysts recently warned that Strategy's Bitcoin selling policy introduces "two-way risk" to the market.

Tension between shareholder value and dilution. For companies that finance Bitcoin purchases through stock issuance, BTC per share is a key metric. If the pace of equity dilution from issuance outpaces the growth of Bitcoin holdings, the per-share Bitcoin value declines even if total holdings increase. Metaplanet reported a Q2 Bitcoin Yield of 6.6%, indicating positive growth in Bitcoin per share that quarter—but this needs to be validated each quarter.

Risk of strategic narrative fading. When Bitcoin prices remain depressed for an extended period, market confidence in the Bitcoin reserve model may waver. Signs in 2026 suggest some investors are shifting from "focusing solely on holdings size" to "focusing on per-share dilution and financing structure." Metaplanet's stock price has fallen approximately 48% year-to-date, exceeding Bitcoin's roughly 31% decline over the same period—this gap indicates the market is pricing in execution risk for this model.

Market Supply-Demand Implications of Continued Corporate Bitcoin Reserve Growth

The ongoing accumulation of Bitcoin by corporate treasuries has multiple impacts on the BTC market supply-demand structure, understood from the following aspects.

Long-term buy-side support on the demand side. Unlike the trading positions of retail investors or hedge funds, corporate Bitcoin holdings exhibit a clear "long-term hold" characteristic—these companies explicitly position Bitcoin as a reserve asset, not a trading tool. This means this portion of buying is relatively insensitive to short-term price fluctuations, forming "sticky demand" in the market. In 2026, when Bitcoin spot ETFs saw net outflows, continued buying by corporate treasuries acted as a counterbalance to some extent.

Continuous compression of circulating supply. 43,000 Bitcoin represents about 0.205% of the total 21 million supply. When the top three companies together hold over 930,000 Bitcoin (approximately 4.4% of the total), the circulating supply available for free trading on the market is being continuously compressed. With demand unchanged or growing, a reduction in circulating supply theoretically supports prices—but this depends on whether these holdings are locked long-term or may be forced to sell under pressure.

Structural contradiction of "the largest buyer also being a potential seller." This is the most subtle potential impact of the Bitcoin reserve model on the market. When these companies need to sell Bitcoin due to financing pressure, dividend payment needs, or strategic shifts, the "largest buyer" that previously supported demand could instantly become the "largest seller." JPMorgan's warning about Strategy is based on this logic—the company's newly authorized plan to sell up to $1.25 billion in Bitcoin means that a previously buy-only largest holder now has the legal authority to sell. The introduction of this "two-way liquidity" changes the market's expectation framework for the behavior of Bitcoin reserve companies.

Amplifying effect on price volatility. The concentrated holdings structure of corporate treasuries means that once a large-scale purchase or sale decision occurs, it may have a disproportionate price impact on the market. This "large order shock" effect becomes more pronounced, especially during periods of low market liquidity. This is both a spillover effect of corporate strategic choices on the market and a new systemic variable that market participants need to consider.

FAQ

Q: How many Bitcoin does Metaplanet currently hold? What is its global ranking among public companies?

As of July 2, 2026, Metaplanet holds 43,000 Bitcoin, making it the world's third-largest publicly traded company by Bitcoin holdings, behind Strategy (approximately 847,363) and Twenty One Capital (approximately 43,514).

Q: What was Metaplanet's average purchase price for Bitcoin in Q2?

Metaplanet purchased 2,823 Bitcoin in Q2 2026 at an average price of approximately $88,300 per coin. This price is below the company's overall average cost of $106,500, helping to lower the cost basis.

Q: What are Metaplanet's Bitcoin holding targets?

The company plans to accumulate 100,000 Bitcoin by the end of 2026 and reach 210,000 Bitcoin by the end of 2027, equivalent to 1% of the total Bitcoin supply.

Q: What are the main risks of the corporate Bitcoin reserve model?

Main risks include balance sheet impairment from Bitcoin price volatility, interest expense pressure from debt financing, shareholder dilution from stock issuance, and the structural risk of the "largest buyer becoming the largest seller" when market sentiment reverses.

Q: How does Metaplanet finance its Bitcoin purchases?

Metaplanet primarily finances through credit facility borrowings and bond issuances, avoiding equity dilution from new share issuance. The company's total debt and preferred stock account for approximately 23% of its capital structure.