On June 17, 2026, the newly appointed chair of the Federal Reserve, Kevin Warsh, completed his first Federal Open Market Committee (FOMC) meeting since taking office. The rate decision itself was unsurprising—FOMC voted 12 to 0 and kept the target range for the federal funds rate unchanged at 3.50% to 3.75% for the fourth consecutive time. However, what truly rattled the market was not the “unchanged” rate, but the “changed” dot plot.

From March’s “12 officials supported rate cuts” to June’s “9 officials supported rate hikes,” the dramatic reversal in the dot plot thoroughly upended market expectations for the monetary-policy path. As of June 22, 2026, Bitcoin (BTC) was trading at $64,513. This Warsh-led “hawkish debut” is forcing crypto assets to re-examine their valuation logic.

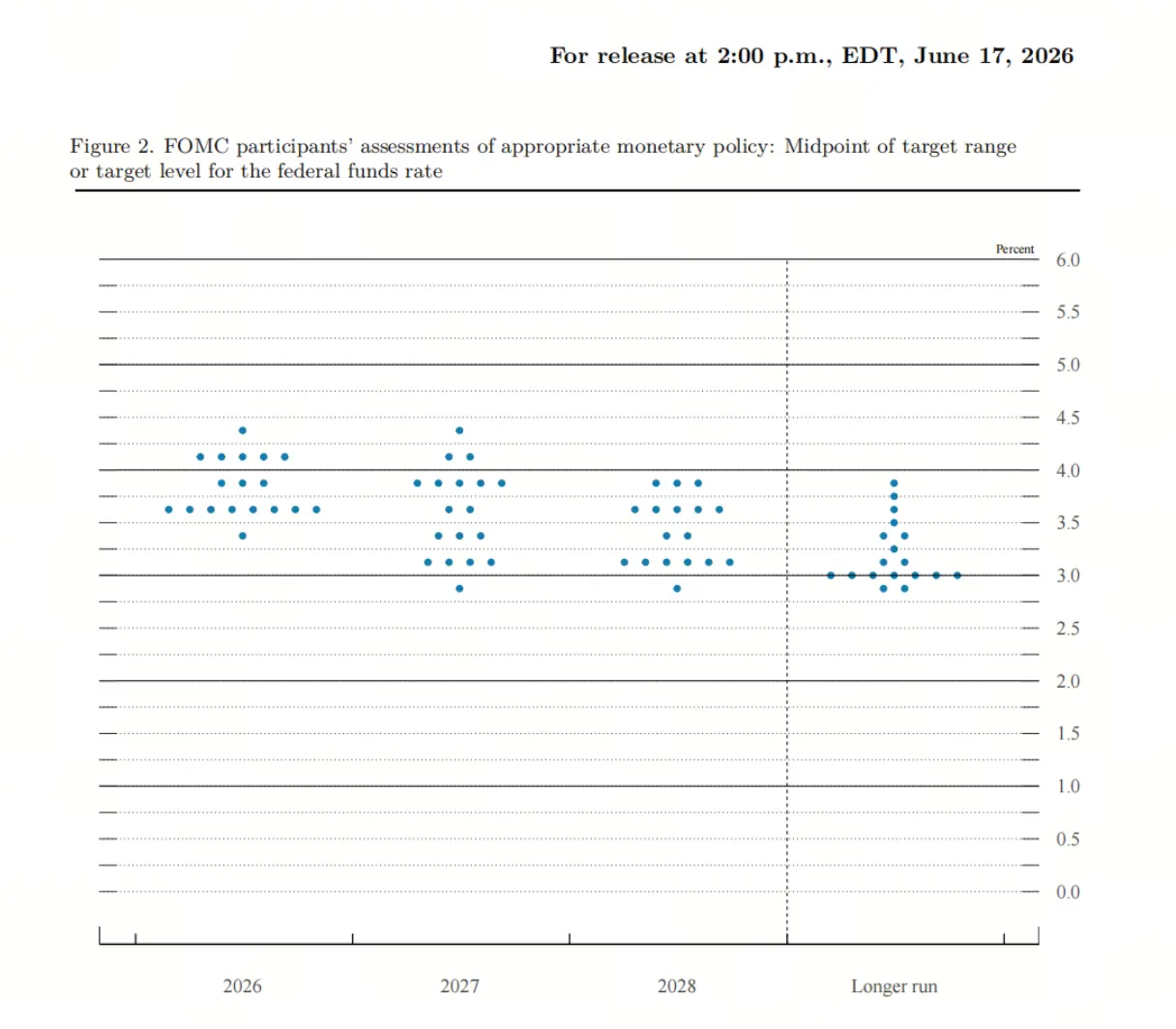

How the dot plot flipped from “rate-cut consensus” to “rate-hike divergence”

In the March dot plot, none of the 19 Federal Reserve officials expected that a rate hike would be needed in 2026, with the median rate expectation at 3.4%. The mainstream market interpretation was that there was still room for rate cuts within the year. At that time, as many as 12 people expected rate cuts within the year, while 7 expected rates to be held steady.

By June, the situation had completely reversed. Warsh himself did not submit a rate forecast—continuing his long-standing reservations about both the dot plot and the Summary of Economic Projections (SEP). Among the 18 officials who did submit forecasts, 9 expected rate hikes in 2026. Of those, 3 predicted 1 hike, 5 predicted 2 hikes, and 1 predicted 3 hikes. Meanwhile, only 1 person still expected a rate cut within the year.

The median year-end rate for 2026 was revised up from 3.4% in March to 3.8%. The median rate expectations for 2027 and 2028 were also raised to 3.6% and 3.4%, respectively, while the long-run neutral rate expectation remained unchanged at 3.1%. The median in the dot plot points to no rate cuts in 2026; the balance between 9 votes supporting hikes and 9 votes supporting holding steady (including the subtle balance created by Warsh not voting) formed an equilibrium.

Why Warsh’s debut is interpreted as “hawkish” by the market

Warsh’s “hawkish” label stems more from how he reshaped his communication style and policy framework than from any explicit statement on raising rates. In fact, multiple analysts have noted: “Warsh isn’t hawkish, but the Fed is hawkish”—the hawkish signal in the dot plot reflects the collective judgment within the board, and Warsh himself did not make a clear statement about rate hikes.

But Warsh changed the market’s policy-expectation framework on three levels. First, the policy statement was drastically reduced from 341 words in April to about 130 words, removing the “looser stance” and forward guidance that hinted at possible rate cuts in the future. Second, in the press conference, Warsh strongly emphasized inflation risks and made it clear that the inflation target would not be revisited until inflation returns to 2%. Third, he announced the establishment of five independent working groups covering five areas: the Fed’s communication mechanisms, balance-sheet management, data sources and reliance, productivity and employment, and the inflation framework.

Warsh wants the market to price based on real economic conditions rather than follow the Fed’s forward guidance. This “Greenspan-style” ambiguous communication approach causes the market to price on its own when clear policy signals are lacking—ironically amplifying volatility in rate-hike expectations.

How rate-hike expectations hit crypto valuation models

Crypto assets, as an interest-free, highly volatile category that is highly sensitive to liquidity, are deeply coupled in their pricing logic to the Fed’s monetary-policy path. Switching from a “rate-cut trade” to a “rate-hike narrative” means the core assumptions in valuation models are being rewritten.

Under the “rate-cut trade” framework, markets expect easier liquidity to push down the risk-free rate and raise the relative appeal of risk assets. Capital flows out of low-yield safe assets (such as U.S. Treasuries) and into high-risk assets, including crypto. But when the narrative switches to “rate hikes,” the logic reverses completely. Higher policy rates mean higher yields on safe assets, increasing the opportunity cost of holding interest-free assets like Bitcoin.

During the Fed’s aggressive rate-hike cycles in 2022 and 2023, crypto and the stock market both fell sharply. A hawkish Fed makes capital more expensive and scarcer, reducing the flow of capital toward speculative assets that are sensitive to risk. Crypto sits at the far end of the risk spectrum, making it the most sensitive to liquidity tightening.

How the market re-priced the probability of December rate hikes

After the FOMC meeting ended, the market quickly reacted to the hawkish dot plot. The CME FedWatch tool showed that the probability priced in the futures market of at least a 25-basis-point hike before December jumped from about 40% before the meeting to 58%. Some data showed that after the meeting, this probability rose further to above 80%. The implied number of rate hikes for all of 2026 from interest-rate futures increased from 0.8 before the meeting to 1.5, and the first hike timing moved to October 2026.

The reaction in asset prices was equally intense. The U.S. Treasury yield curve flattened significantly— the spread between the 2-year and 10-year Treasury yields narrowed to about 28 basis points, the tightest level since April 2025. The U.S. dollar index strengthened, while U.S. stocks and gold fell in tandem.

Within 24 hours after the decision was released, the crypto market was dealt a heavy blow. Bitcoin fell below $63,000. The liquidation volume for crypto futures across the market was close to $500 million, and more than 116,000 traders were liquidated. Crypto’s total market capitalization dropped 4.48%. Long positions betting on a rebound were trapped “in the opposite direction”—the market’s reaction was not to the rate staying “unchanged,” but to expectations that rate hikes could happen in the future.

The long-term implications of Warsh’s reform framework for crypto assets

Warsh’s reforms are not only about the path of interest rates—they are also about the Fed’s underlying operating logic, which could shape the long-term pricing environment for crypto assets more profoundly than a single rate hike.

On the balance-sheet front, Warsh advocates returning to a smaller, more neutral Fed balance sheet. This means not only that interest rates could rise, but also that the “quantity” of liquidity could be reduced—two-way tightening would constitute a more severe stress test for crypto assets. On the data-dependency side, Warsh emphasizes bringing in more data sources, including financial market prices and real-time data from the public. This means Fed decisions would be closer to actual economic activity rather than relying on lagging official statistics, and the risk of sudden policy pivots could increase.

On productivity and employment, Warsh specifically set up a working group to assess AI’s impact on productivity, employment structure, and wages. He views AI-driven productivity gains as a potential supply-side disinflationary force. If AI truly boosts productivity significantly, it could suppress inflation from the supply side, thereby changing the necessity of Fed rate hikes. Finally, on communication mechanisms, Warsh plans a comprehensive review of press conferences, dot plots, and meeting arrangements before year-end. Reforms to the SEP and the restructuring of the communication framework will gradually be rolled out, and by then, the way the market understands and prices Fed policy itself will change.

Uncertainty in rate-hike expectations still remains

Even though the dot plot released strong hawkish signals, whether rate hikes truly happen within the year remains uncertain. Warsh himself did not submit an interest-rate forecast, and in his press conference he played down the dot plot’s guidance for the policy path. He described the act of submitting forecasts by committee members as “using pencils with large erasers.”

The drivers of inflation also merit attention. In May, the U.S. CPI year-over-year increase was 4.2%, but the main driver of this round of inflation upside has been higher energy costs triggered by the conflict in the Middle East. Iran and the U.S. have signed an agreement; oil prices have not yet returned to pre-conflict levels, but they have already clearly fallen back from their highs. If oil prices continue to decline trend-wise, confirmation that inflation pressure is easing would strengthen, and rate-hike expectations within the year could still be rolled back.

In addition, Warsh is heavily influenced by Friedman’s quantity theory of money. He believes that inflation ultimately is a monetary phenomenon, and that the cure lies in shrinking the balance sheet rather than boosting interest rates. This means his intense focus on inflation does not necessarily translate into a linear impulse to hike rates.

FAQ

Q: Did the June FOMC meeting really hike rates?

No. The FOMC voted 12-0 to keep the federal funds rate unchanged at 3.50%-3.75%—the fourth consecutive time it held steady. What drew the market’s attention instead was the dot plot showing 9 officials supporting rate hikes within 2026.

Q: What are the core differences between the March dot plot and the June dot plot?

In the March dot plot, 12 officials expected rate cuts within the year, and none expected rate hikes; in the June dot plot, 9 officials expected rate hikes within the year, and only 1 expected rate cuts. The median year-end rate for 2026 was revised up from 3.4% to 3.8%.

Q: What is Warsh’s personal stance on rate hikes?

Warsh did not submit his own interest-rate forecast. In the press conference, he emphasized inflation risks, but downplayed the dot plot’s significance as guidance. The market generally believes the hawkish signal comes from the board as a whole, not from Warsh’s personal position.

Q: What is the main transmission mechanism of how rate-hike expectations affect crypto assets?

Higher policy rates increase the yields of safe assets (such as U.S. Treasuries), raising the opportunity cost of holding interest-free assets like Bitcoin. At the same time, a hawkish Fed tightens liquidity, reducing capital flows into speculative assets.

Q: Are rate hikes within the year a certainty?

No. Inflation is mainly driven by energy prices, and oil prices have already eased after the U.S.-Iran agreement. If inflation pressure weakens, rate-hike expectations could be rolled back. Warsh himself also made no explicit commitment to a rate-hike path.