On July 6, 2026, Strategy (formerly MicroStrategy) announced a blockbuster news that rocked the crypto industry's capital markets: the company sold a total of 3,588 Bitcoin between June 29 and July 5, with a total value of approximately $216 million. This is the company's largest reduction since December 2022 and the second publicly disclosed Bitcoin sale in 2026.

Source: @saylor

For a company that has enshrined "buy and never sell Bitcoin" in its corporate DNA, every sale draws attention. This time, the scale of 3,588 — 112 times the 32-coin "test" sale in late May — completely shattered any market illusion that the "only buy, never sell" narrative might only be loosened symbolically.

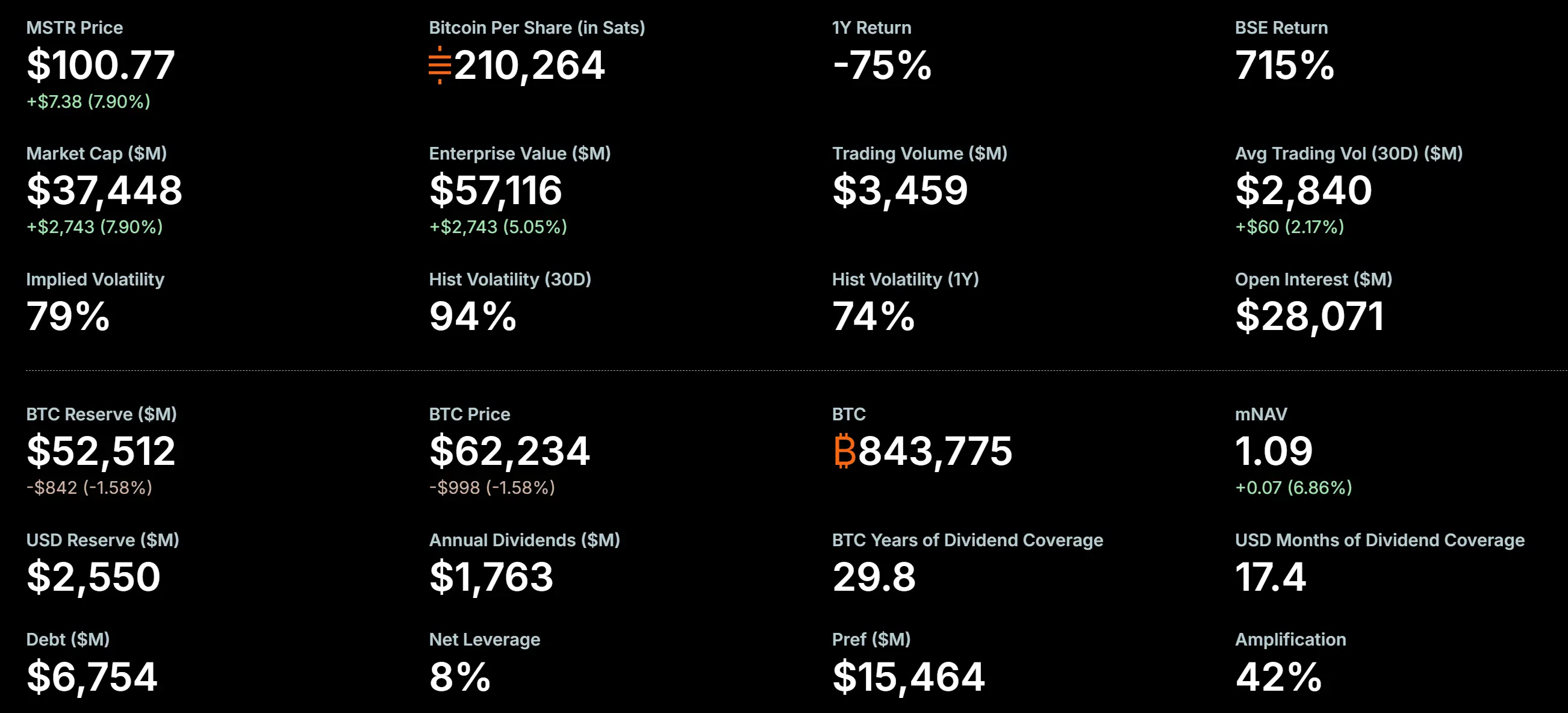

As of July 5, 2026, Strategy still holds 843,775 Bitcoin, with a total cost basis of approximately $63.69 billion, an average cost of about $75,476 per coin. At the current Bitcoin price of $62,076.5, its remaining holdings still face significant unrealized losses. The 3,588 Bitcoin sold had an average price of about $60,197, relative to an average cost of $75,651, implying a realized loss of approximately $55.45 million.

Why would a company with "HODL" as its core business model sell Bitcoin twice in 2026? This article systematically analyzes the logic behind Strategy's BTC sale from four dimensions: historical selling records, financial pressure, capital structure, and strategic transformation.

Not the First Time: Strategy's Three Bitcoin Sale Records

Before delving into this sale, it is necessary to clarify Strategy's Bitcoin sale history. It is often mischaracterized as the "first reduction," but in fact, Strategy has two prior publicly recorded Bitcoin sales.

First: December 2022 — Tax-Loss Harvesting (704 BTC)

In December 2022, Strategy sold 704 Bitcoin, cashing out $11.8 million at an average price of about $16,776. However, this sale was not a true "reduction" — the company bought back 810 Bitcoin at a lower price two days later. It was a typical tax-loss harvesting operation designed to create losses on the books to offset taxes, not a fundamental shift in the company's long-term Bitcoin holding strategy. As such, the market generally does not regard this as a "real sell."

Second: May 26-31, 2026 — Paying Preferred Stock Dividends (32 BTC)

On June 1, 2026, Strategy filed an 8-K with the U.S. Securities and Exchange Commission, disclosing that the company sold 32 Bitcoin between May 26 and 31 at an average price of about $77,135, totaling approximately $2.5 million. The filing explicitly stated that the proceeds would be used entirely to pay dividends on the company's preferred stock. This was Strategy's first genuine reduction since the December 2022 tax maneuver, and the first time the "never sell" narrative was officially broken by a regulatory filing. However, 32 coins represented only about 0.004% of total holdings, having virtually no material financial impact. The market widely interpreted it as a "signal engineering" exercise — to validate processes and manage expectations for a larger reduction framework.

Third: June 29 to July 5, 2026 — The Current Large-Scale Sale (3,588 BTC)

This is the core event of this article. On the same day the "Digital Credit Capital Framework" was formally approved (June 29), Strategy initiated the first batch of sales. The two transactions totaled 3,588 BTC, 112 times the size of the May sale.

Understanding the difference in nature among these three sales is crucial: the 2022 sale was a tax tool, the May 2026 sale was a symbolic "flare," and the July 2026 sale — this one — is a genuine, cash-flow-driven, financially material large-scale reduction.

Transaction Details: How 3,588 BTC Were Sold

According to regulatory filings, Strategy's reduction of 3,588 Bitcoin was completed in two batches.

The first batch occurred from June 29 to June 30, selling 1,363 Bitcoin for a total of $80.8 million, at an average price of $59,256 per coin. The second batch occurred from July 1 to July 5, selling 2,225 Bitcoin for a total of $135.2 million, at an average price of $60,773 per coin. The two transactions together total approximately $216 million.

MicroStrategy Bitcoin holdings, Source: 策略

Before this sale, Strategy's total BTC holdings stood at 847,363. After the sale, holdings decreased to 843,775. Notably, on July 1, on-chain data detected a transfer of 491 Bitcoin from a wallet associated with Strategy, sparking market speculation about further reductions. Based on the final disclosed data, this transfer was part of the second batch of 2,225.

Prior to this large-scale sale, Strategy had already sold 32 BTC at the end of May. That small transaction now appears to have served as a validation of the sale process and infrastructure, paving the way for the larger July reduction.

Financial Pressure: The Structural Shift When mNAV Fell Below 1.0

To understand why Strategy sold Bitcoin twice in 2026, one must first grasp a key metric: mNAV (Market Value to Net Asset Value) ratio. This measures the ratio of the company's market capitalization to the net asset value of its Bitcoin holdings.

Historically, Strategy's mNAV operated well above 1.0, peaking at 3.89 in November 2024. An mNAV above 1.0 means the market is willing to pay a premium for the company's Bitcoin holdings, recognizing the added value of "corporate packaging" relative to directly holding BTC — including tax efficiency, capital market liquidity premiums, and the ability to expand holdings through debt and equity financing.

However, this premium reversed fundamentally in 2026. On June 26, Strategy's mNAV ratio fell below 1.0 for the first time, to 0.99. Some analysts note that because Strategy uses the face value of debt and preferred stock rather than market value when calculating enterprise value, the officially reported mNAV may be overstated — using market value, the actual mNAV could be even lower.

An mNAV below 1.0 carries profound symbolic and practical implications. It means the market perceives Strategy's corporate structure itself as a net liability relative to directly holding Bitcoin. CoinShares Research Director James Butterfill commented: "mNAV falling below 1.0 is a structural break — the premium that once supported the debt-financed acquisition model has vanished."

When a company's market cap is lower than its net asset value, traditional corporate finance logic points in one direction: sell assets to repay debt, buy back stock, or pay dividends to close the discount. That is exactly where Strategy now finds itself.

Dividend Obligations: Cash Flow Pressure from Digital Credit Securities

The direct purpose of Strategy's Bitcoin sale is to pay dividends on its Digital Credit Securities.

Digital Credit Securities are a series of preferred stock products that Strategy aggressively launched in 2025, including STRF (10% annual interest), STRE, STRK (8% annual), STRD (10% annual), and the flagship STRC (11.5% annual). These products, backed by Bitcoin holdings, offer investors fixed or variable dividend yields. Strategy calls them "digital credit." Essentially, it raises funds by issuing preferred stock, uses those funds to buy Bitcoin, and covers the dividend payments with the potential appreciation of the Bitcoin holdings.

This model worked well during a Bitcoin price uptrend — appreciation covered dividend costs, preferred investors earned steady returns, and the company continuously expanded its BTC holdings. However, as Bitcoin prices fell from their 2025 all-time highs, this "flywheel" began spinning in reverse.

As of 2026, Strategy's total preferred stock size is approximately $15.482 billion, 2.3 times the size of its convertible bonds (approximately $6.754 billion). Just the annualized dividend expense for STRC alone is nearly $1.2 billion, while the company's software business annual revenue is only about $500 million. The company's total annualized interest and dividend obligations are approximately $1.712 billion.

Strategy's dollar cash reserve set up in December 2025 was $2.25 billion, but by May 31, 2026, it had fallen to about $900 million, consuming $1.35 billion in six months. JPMorgan estimates that the existing dollar reserve can only support about 6.3 months of dividend payments. The Q1 2026 earnings report recorded a net loss of $12.54 billion, including approximately $14.46 billion in unrealized Bitcoin losses.

When Bitcoin prices are below the cost basis and the company cannot cycle finance through issuing new shares at a premium, selling some Bitcoin for dollars to meet dividend payments becomes a necessary but painful choice.

On June 29, 2026, Strategy's board formally approved the "Digital Credit Capital Framework," authorizing the company to sell up to $1.25 billion worth of Bitcoin to strengthen cash reserves, pay preferred dividends and interest, and conduct share buybacks. The introduction of this framework marks Strategy's shift from a pure "capital issuance" model to a more active "capital management" phase.

Notably, as of July 5, the $1.25 billion authorization limit had not been touched — meaning this $216 million sale came from other channels, leaving room for further sales in the future.

Strategic Transformation: From "One-Way Accumulation" to "Two-Way Capital Management"

Strategy's sale of 3,588 BTC should not be simply interpreted as "bearish on Bitcoin" or "strategic retreat." A more accurate characterization is: the company is transitioning from a "one-way accumulation" model to a "two-way capital management" model.

Under the "one-way accumulation" model, Strategy's core narrative was "constantly buy more Bitcoin" — raising funds through issuing stock, preferred shares, and convertible bonds, then deploying all funds into the Bitcoin market. This model was highly effective from 2020 to 2024, with the company at one point holding over 847,000 BTC, becoming the largest corporate Bitcoin holder globally.

However, the sustainability of this model depended on several key premises: continuous Bitcoin price appreciation, the company's stock price maintaining a premium relative to BTC (i.e., mNAV > 1.0), and the market's willingness to provide financing at reasonable costs. When these premises no longer hold, the inertia of the model itself becomes a risk.

The introduction of the "Digital Credit Capital Framework" is an institutional response to this risk. Under this framework, Bitcoin is no longer just an "asset to be hoarded," but is incorporated into the company's proactive balance sheet management tool. The company can sell Bitcoin under specific conditions — including to pay dividends, repurchase shares, or build dollar cash reserves — thereby meeting short-term dollar liquidity needs while maintaining long-term Bitcoin exposure.

Huobi Research Institute defines this shift as a leap from the "DAT 1.0 era" to the "DAT 2.0 era" — moving from purely financing to hoard Bitcoin to a new stage of digital asset treasury management focused on liquidity. Bitwise Chief Investment Officer Matt Hougan commented that Strategy can no longer be simply described as a "one-way Bitcoin buyer"; institutional market participants' perception of its role in the Bitcoin ecosystem is changing.

The implications of this shift are far-reaching: Strategy is evolving from a "Bitcoin accumulation vehicle" into a "Bitcoin capital management platform."

Market Impact and Potential Risks

Limited Direct Impact on the Bitcoin Market

In terms of scale, 3,588 BTC represents only about 0.4% of Strategy's total holdings. Given that the current daily average Bitcoin market trading volume is already in the tens of billions of dollars, this magnitude is insufficient to cause a structural shock. After the news, Bitcoin prices did not show significant volatility. The market's pricing logic seems to be: this is a sale driven by specific financial needs, not a denial of the company's long-term Bitcoin conviction. Moreover, as a leading enterprise with a vast institutional network, Strategy likely executed the sale through over-the-counter or block trades to institutional buyers to avoid direct impact on spot market prices.

But the "Demonstration Effect" Cannot Be Ignored

The greater impact is on the expectation level. Strategy's previous "only buy, never sell" pledge served as a kind of "rigid demand" in the market — the market knew that regardless of price fluctuations, there was always a large buyer steadily absorbing BTC. The 32-coin sale in May 2026 already broke the "sanctity" of that pledge, and the 3,588-coin sale in July completely eliminated a key "buy-side anchor" from the market.

JPMorgan noted in a recent report that Strategy's new policy creates "two-way trading risk" — the company can both buy and sell Bitcoin, increasing the difficulty of forecasting price movements. The report further stated that if Strategy can maintain a higher cash reserve to cover two to three years of dividend payments, it could reduce the probability of forced Bitcoin sales in the future.

Risk of a Negative Feedback Loop

The primary risk Strategy currently faces is a potentially self-reinforcing negative feedback loop: Bitcoin price falls → mNAV declines further → the company faces greater dividend payment pressure and tighter liquidity → needs to sell more Bitcoin for dollars → selling pressure may further depress Bitcoin prices → cycle continues.

As of July 5, Strategy's dollar cash reserve stood at $2.55 billion. This reserve level is an increase from the $900 million at the end of May, mainly due to capital allocation around the framework approval on June 29. However, given its preferred stock annualized payment obligations of approximately $1.712 billion, and convertible bonds maturing in 2027 and 2028, whether the $2.55 billion buffer is sufficient remains to be seen.

Strategy's sale of 3,588 Bitcoin is a rational financial decision in the 2026 market environment — neither a simple "capitulation" nor a fundamental reversal of strategic direction. It reveals the real fragility of the "Bitcoin treasury model" in extreme market cycles: when the mNAV premium vanishes and dividend payment obligations are rigid, even the most steadfast "HODLers" must make trade-offs in asset allocation.

Looking back at Strategy's three sales — the 2022 tax maneuver, the 32-coin "flare" in May 2026, and the 3,588-coin large reduction in July 2026 — a clear evolutionary path emerges: from accounting tool to symbolic action to genuine liquidity management. The nature of each sale changes, but the direction is consistent — the company is transforming from a pure "Bitcoin accumulator" into a more complex "digital asset capital manager."

This event provides an important reflection window for the entire crypto industry — enterprise-level Bitcoin holding strategies cannot rely solely on the assumption of one-way appreciation; they must be built on a complete framework of hedging mechanisms, cash flow management, and dynamic capital structure adjustment. Strategy's "Digital Credit Capital Framework" may well be a product of such reflection. Going forward, the market will closely watch whether its mNAV can recover, whether cash reserves can cover the dividend gap, and whether this "two-way management" model can prove its sustainability amid Bitcoin volatility. For other listed companies considering adding Bitcoin to their balance sheets, Strategy's choice is undoubtedly a costly but highly instructive case study.

FAQ

Q1: Has Strategy sold Bitcoin before?

Yes, three times. First: December 2022, selling 704 BTC (tax-loss harvesting, bought back 810 BTC two days later). Second: May 2026, selling 32 BTC (to pay preferred stock dividends). Third: June 29 to July 5, 2026, selling 3,588 BTC (this large-scale reduction).

Q2: How much loss did this sale incur?

Strategy sold the 3,588 BTC at an average price of about $60,197, while its overall BTC average cost basis is about $75,651, resulting in a realized loss of approximately $55.45 million from this sale. The remaining 843,775 BTC still face significant unrealized losses.

Q3: Will Strategy continue to sell Bitcoin?

Possibly. Strategy's "Digital Credit Capital Framework" authorizes the company to sell up to $1.25 billion worth of Bitcoin. This sale was $216 million, and as of July 5, that limit had not been touched — meaning this sale came from other channels, leaving room for further sales. Whether to continue selling will depend on Bitcoin price trends, the company's dividend payment needs, and whether mNAV can recover above 1.0.

Q4: What does this mean for the Bitcoin market?

In the short term, direct impact is limited — 3,588 BTC is only 0.4% of Strategy's total holdings, and likely executed via OTC. However, the complete break of the "only buy, never sell" pledge removes a key buy-side anchor from the market, increasing the complexity of price prediction. JPMorgan notes this creates "two-way trading risk."

Q5: Has Strategy's "Bitcoin Treasury Model" failed?

It cannot be simply labeled a "failure." A more accurate description: the model worked well during an uptrend but exposed structural vulnerabilities during a downtrend — reliance on a continuous market premium to sustain the financing cycle. Strategy is upgrading the model from "one-way accumulation" to "two-way management" via the Digital Credit Capital Framework, marking an evolution rather than an end.