OpenAI Operational and financing details of a company can influence market expectations for its pre-IPO valuation. However, when the route involves Gate Pre-IPOs OPENAI, the primary risk arises from the product’s structure.

Gate’s risk disclosure states: the target company is not yet listed and the listing date is undetermined, presenting significant uncertainty; a decline in value, failure to list with no alternative exit, or bankruptcy resulting in zero value may cause losses; crypto asset volatility and insufficient pre-market liquidity are also highlighted. These statements address uncertainty and potential loss, not a guarantee or exclusion of any outcome.

Why is the product's nature the primary item to verify?

OPENAI is officially defined as a mirror note and contingent payment note, designed to reflect market value before and after listing. The presence of OpenAI or Pre-IPO in the name does not mean each certificate corresponds to a deliverable company share. OPENAI and Actual Equity clarifies that rights are governed by platform terms, not by the shareholder register. If product classification is overlooked, subsequent discussions about valuation, pre-market activity, and settlement will be based on incorrect premises.

The disclaimer emphasizes that the issuance is not connected to OpenAI; OpenAI is not involved, authorized, or endorsing; does not receive proceeds; and has not provided information to Gate. Treating platform materials as company commitments directly deviates from proper disclosure.

What boundaries result from non-shareholder rights?

Holders do not have voting rights, dividend rights, or any other shareholder privileges, nor can they assert claims against OpenAI based on product gains or losses. Contractual claims are limited to product arrangements: allocation, unlocking, circulation, and settlement. In other words, the discussion centers on “whether product terms allow a certain action,” not “what shareholder rights are granted by company bylaws.”

| Verification Dimension |

OPENAI |

OpenAI Actual Equity |

| Source of Rights |

Gate product terms |

Shares and company documents |

| Voting / Dividend |

None |

Based on share class |

| Legal Relationship |

Not established |

Shareholder and company |

| Value Handling |

Reference value + terms |

Company equity and exit arrangements |

What uncertainties affect valuation and pre-market pricing?

The implied valuation of approximately $895 billion is derived from committed price and reference share count, as detailed in Implied Valuation and Dilution. Historical post-investment valuations in the company’s financing table offer a separate data set. Issuance, cancellation, stock splits, or reclassification may alter references; pre-market prices are also influenced by order depth and temporary trading arrangements and should not be considered the official market price for listed shares. Equating “implied valuation” and “pre-market transactions” leads to misinterpretation of both formula inputs and market mechanisms.

Pre-market trading is subject to volatility, limited liquidity, and potential rule adjustments. Announcements and risk disclosures specify: borrowed funds cannot be used for subscription; institutional accounts and subaccounts are not eligible; users in restricted regions may not be able to access all or part of services; in case of translation discrepancies, the English version prevails. Subscription and unlocking details are outlined in Subscription Allocation and Unlock. Eligibility and borrowing restrictions define participation boundaries, not legal opinions for individual users.

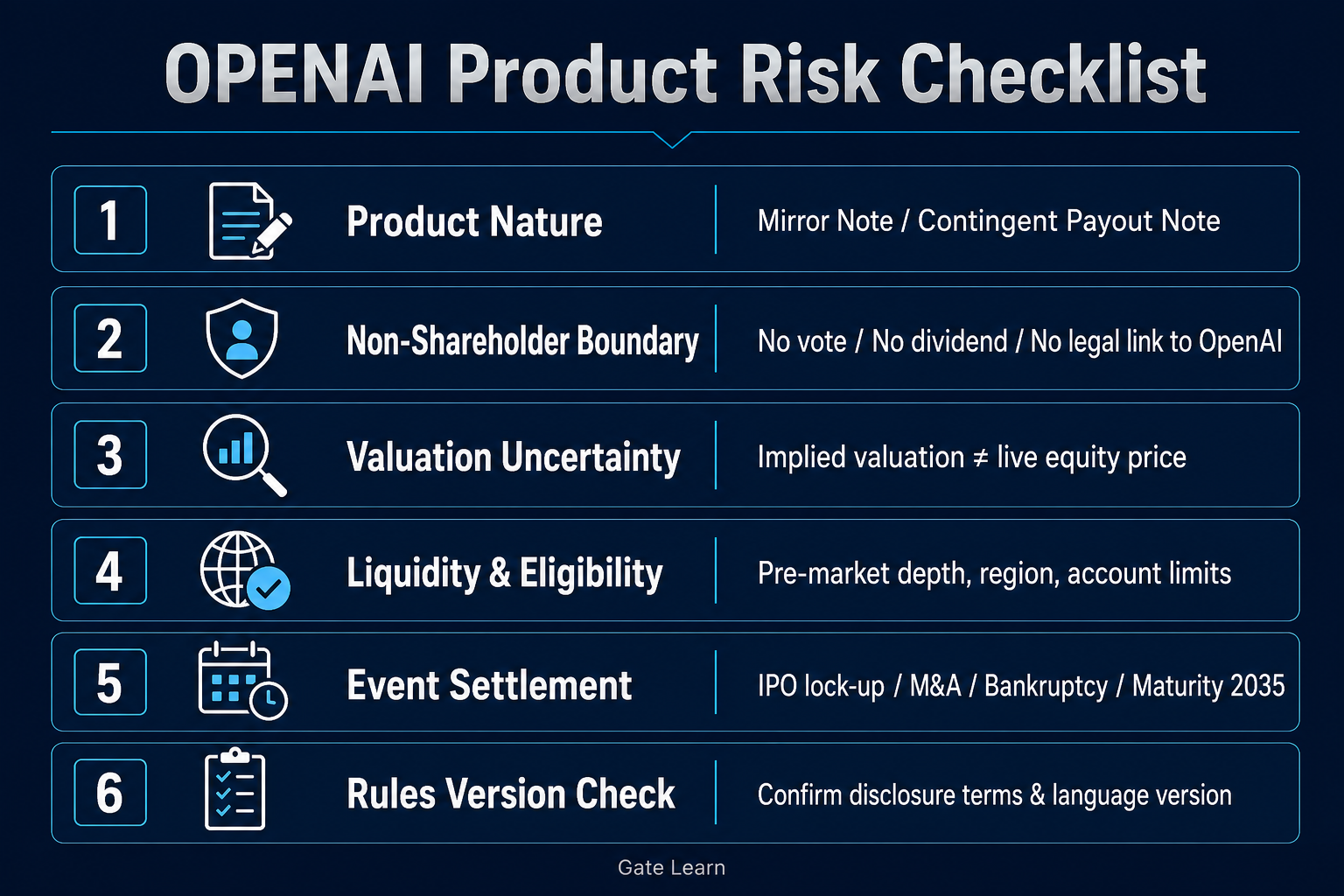

Figure 1. Checklist for product nature, non-shareholder rights, reference value, liquidity, eligibility, and settlement.

Figure 1. Checklist for product nature, non-shareholder rights, reference value, liquidity, eligibility, and settlement.

How do IPO delays, mergers, or bankruptcy impact the process?

Uncertainty around the listing date means the exit path remains governed by pre-market and maturity terms. After the target company’s IPO, assets are subject to a six-month lock-up period; upon expiration, disclosed options include conversion to stock assets, tokenized shares, or USDT redemption. If the company is not listed by December 31, 2035, or undergoes acquisition, merger, or bankruptcy, settlement is based on the fair market value of common stock in USDT; if liquidation results in zero, the product’s reference value may also become zero. Process details are available in Pre-Market Trading and Settlement.

How to establish a product rule checklist?

| Order |

Fact to Confirm |

Corresponding Risk Boundary |

| 1 Product Definition |

Mirror note / contingent payment note |

Not actual equity |

| 2 Scope of Rights |

No voting, dividend, or company legal relationship |

Do not treat notes as shareholder qualification |

| 3 Reference and Adjustment |

Implied valuation formula, company actions |

Figures may become invalid |

| 4 Market and Eligibility |

Pre-market, account, region, borrowing restrictions |

Availability uncertain |

| 5 Event Settlement |

IPO lock-up, maturity, merger, bankruptcy |

Exit method and FMV criteria |

The checklist should be cross-referenced with the specific version and timestamp of the Gate project page and announcements; PANews reports are only suitable for cross-checking public statements. When verifying, it is advisable to review both the project page FAQ and the full announcement text: the FAQ often condenses boundaries into Q&A format, while the announcement provides complete parameters for subscription window, unlock schedule, and settlement section. If statements differ, such as “certificates can be traded pre-market” versus “allocations are unlocked in installments,” they should be interpreted in a mechanism-compatible manner, not by drawing conclusions from a single statement.

Investors tracking OpenAI should also confirm whether their materials reference company financing rounds or OPENAI product committed prices. Mixing the two is likely to distort risk assessment. Platform risk disclosures highlight high uncertainty and potential principal loss and do not guarantee returns; the purpose of reviewing the checklist is to identify terms, not to seek “definite commitments.” If terms are updated, verification should be based on the updated English original and project page—not outdated paraphrasing.

Summary

When assessing platform mapping routes under the OpenAI keyword, risks extend beyond pre-IPO value volatility to include the rights and settlement boundaries of mirror notes. Non-shareholder status, reference valuation assumptions, pre-market liquidity, eligibility restrictions, and IPO, merger, bankruptcy, or maturity terms collectively determine the scope of claimable outcomes. Systematic verification against official disclosures separates company narratives from product rules and prevents the use of stock terminology to describe note constraints. High risk and non-principal protection should be considered fundamental premises when reviewing this content.

FAQ

Is OPENAI OpenAI stock?

No. It is a mirror note and contingent payment note disclosed by Gate, not representing actual shares and does not establish a legal relationship with OpenAI.

Why might implied valuation and pre-market price differ?

Implied valuation is based on committed price and reference share count; pre-market price is determined by trading supply and demand and platform rules. Company actions and the unlisted status further widen the gap.

What liquidity risks exist in pre-market trading?

Risks include price volatility, limited order depth, and potential changes to transfer conditions; temporary codes and circulating supply may also be adjusted based on listing status.

How is settlement handled if IPO is delayed or not listed?

The maturity date is December 31, 2035; if not listed by then or in the event of acquisition, merger, or bankruptcy, settlement is based on the fair market value of common stock in USDT; if liquidation results in zero, the reference value may also become zero.

Which accounts or regions may be unable to participate?

Official notice: users in restricted regions may not be able to access all or part of services; institutional accounts and subaccounts are not eligible for Pre-IPO subscription; borrowed funds may not be used for subscription.