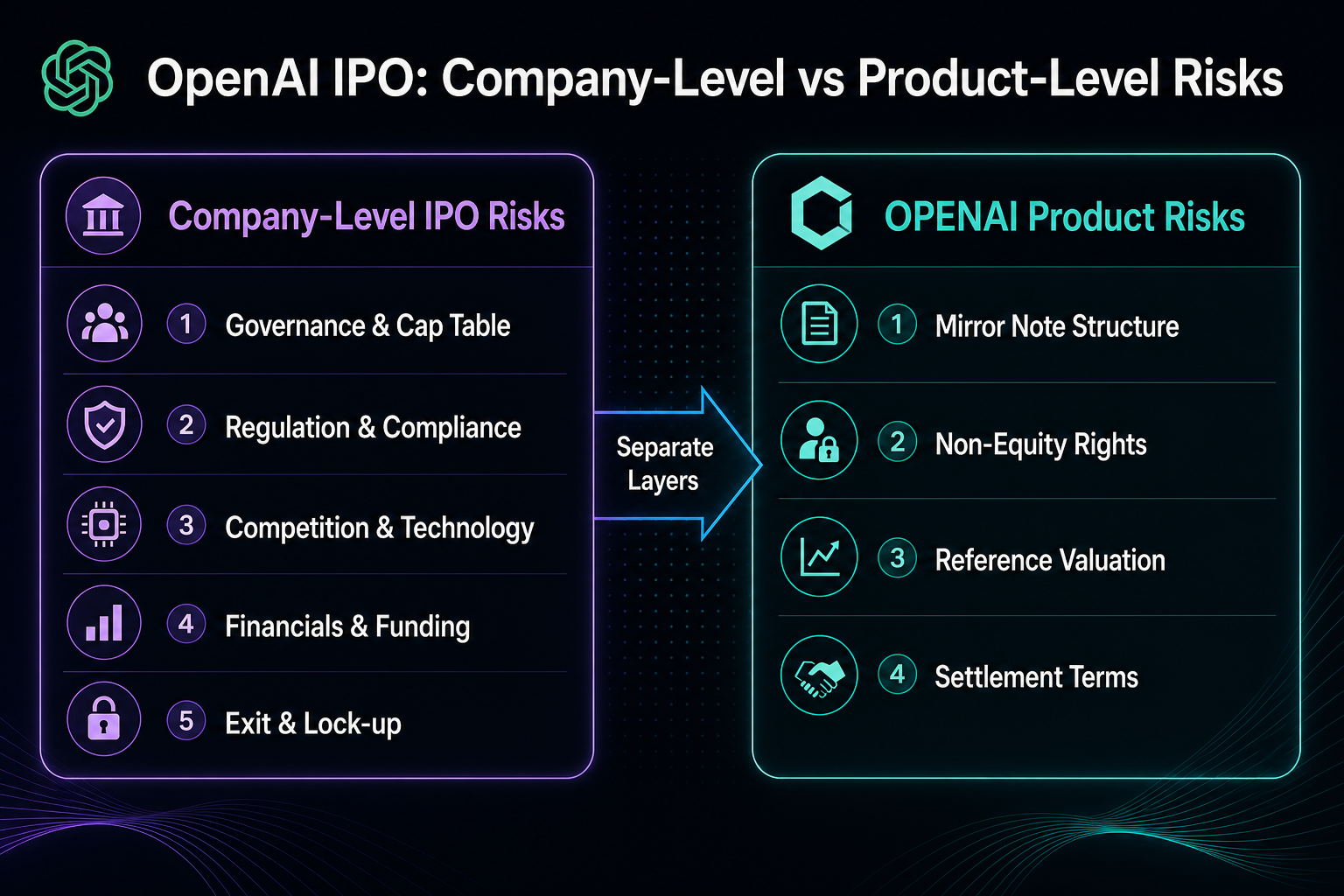

What are the risks associated with an OpenAI IPO? For companies not yet publicly listed, the typical due diligence framework covers five categories of company-level variables: governance and equity structure, regulatory and compliance, competition and technology, financials and ongoing financing, and exit and lock-up periods. OpenAI is still in the pre-IPO stage, and when the market discusses its potential IPO, it often conflates “whether the company can go public” with “how platform notes will be settled.” It’s important to read OpenAI’s company entity, its equity structure, and the rules for Gate Pre-IPOs’ OPENAI separately. The following sections break down each category and clarify their boundaries with OPENAI product risk.

Company-level risks address whether the entity can complete an IPO and how its capital structure may change; product-level risks address the terms under which holders receive allocation, transfer, and settlement. These two layers are related, but the subjects and sources of due diligence differ.

What are the risks of an OpenAI IPO? Five main company-level risk categories

| Risk Category |

Core Concern |

Typical Manifestation |

| 1. Governance and Equity Structure |

Cap table, dilution, share classes |

Complex nonprofit parent and capped-profit arrangements |

| 2. Regulatory and Compliance |

AI governance, data, cross-border |

SEC disclosures and multi-jurisdictional review |

| 3. Competition and Technology |

Model iteration, open source, compute power |

Technology window and gross margin pressure |

| 4. Financials and Financing |

Burn rate, profitability path |

Delayed IPO or additional financing |

| 5. Exit and Lock-up |

IPO delay, M&A, bankruptcy |

Secondary liquidity and lock-up |

These five risk categories apply to the OpenAI company itself and are distinct from the terms and conditions risk of Gate’s OPENAI mirror notes. The recommended order is to review company-level risks first, then product-level risks, to avoid confusing stock terminology with note-specific constraints.

Figure 1. Company-level IPO risks and OPENAI product risks are different layers of due diligence and should be reviewed separately.

Figure 1. Company-level IPO risks and OPENAI product risks are different layers of due diligence and should be reviewed separately.

Risk 1: Governance and Equity Structure—What should you focus on before the IPO?

OpenAI’s governance includes the nonprofit OpenAI, Inc. and OpenAI Global, LLC, among other entities. The capped-profit structure makes share classes and profit limits more complex than at traditional tech companies. New financing rounds, option pool expansion, or share reclassification can all dilute per-share economic rights.

Regulators and underwriters typically review the cap table and key shareholder rights; the more complex the structure, the longer IPO filings may take. New share issuances will change the reference share count used for OPENAI’s implied valuation, but note holders do not become registered shareholders as a result.

Risk 2: Regulatory and Compliance—What scrutiny do AI companies face in an IPO?

Generative AI companies are subject to multi-jurisdictional regulation: model safety, training data compliance, privacy, content liability, and export controls, all of which can impact business operations and costs. The U.S. Securities and Exchange Commission (SEC) has specific disclosure requirements for AI-focused companies, which may increase IPO filing complexity.

Cross-border APIs and contracts with governments or enterprises introduce data localization risks. Regulatory investigations or business restrictions may not directly change product settlement terms, but they can impact market assessments of pre-IPO valuation and listing feasibility. This risk category is part of company compliance and should be reviewed against public information and policy trends, not just subscription parameters.

Risk 3: Competition and Technology—How do model and compute dependencies create IPO pressure?

OpenAI faces competition from closed-source leaders, open-source alternatives, and proprietary models developed by cloud providers. The window for technological leadership is limited, and inference costs and user switching costs evolve with each iteration. Compute power and chip procurement are hard constraints that affect gross margins and capital expenditures.

Technology risk impacts whether the IPO narrative can be sustained and whether the public market will accept R&D spending. This is a company fundamental, related to but not equivalent to OPENAI’s pre-market price fluctuations—pre-market prices reflect note supply and demand and platform rules, not the company’s financials.

Risk 4: Financials and Ongoing Financing—Why is it difficult for unprofitable AI companies to go public?

Unlisted AI companies have high R&D and compute expenses; the timeline to profitability and self-sustaining cash flow remains a market focus. Ongoing financing, debt arrangements, and customer concentration all affect pre-IPO pricing expectations.

If the burn rate exceeds revenue growth, the company may delay its IPO or increase fundraising frequency. Financial risk means the IPO window depends on whether financial statements can support ongoing disclosure, not on specific stock price forecasts. The OPENAI promised price and implied valuation are product mapping inputs, not substitutes for independent analysis of income statements and cash flow.

Risk 5: Exit and Lock-up—What happens if the IPO is delayed or doesn’t occur?

Exit paths include IPO, M&A, secondary sales, and long-term private holding. IPO delays mean public liquidity is postponed; M&A can change the equity structure; bankruptcy or restructuring can result in common equity being impaired or wiped out. Private secondary liquidity is limited, and transfers are often subject to ROFR and lock-up restrictions.

| Company Exit Scenario |

Common Impact on Unlisted Equity |

Relationship to OPENAI Terms |

| Successful IPO |

Public liquidity opens, shares tradeable after lock-up |

Platform discloses redemption or holding options post-IPO |

| IPO Delayed |

Private valuations and secondary liquidity under pressure |

Pre-market and expiry terms still follow product rules |

| M&A / Merger |

Consideration and equity conversion per transaction documents |

Product handled per common stock FMV and disclosure standards |

| Bankruptcy / Liquidation |

Common stock may be wiped out or heavily impaired |

Product reference value may also go to zero |

After the company goes public, underwriter and existing shareholder lock-ups further limit early liquidity. Gate discloses a six-month lock-up for OPENAI following IPO; redemption options after this period are handled at the product level and are not the same as company shareholder lock-ups.

Figure 2. The five company-level IPO risk categories are organized by governance, regulatory, competition, financial, and exit order to facilitate due diligence.

Figure 2. The five company-level IPO risk categories are organized by governance, regulatory, competition, financial, and exit order to facilitate due diligence.

What additional risks are associated with Gate’s OPENAI mirror notes?

The five company IPO risk categories address whether OpenAI can go public; OPENAI has additional product-level risks: non-equity nature, no voting or dividend rights, reference value adjustments, pre-market liquidity, account and regional eligibility, and FMV settlement if the company does not list, is acquired, merges, or goes bankrupt. Each item is detailed in the OPENAI product risk checklist.

Even if IPO expectations rise, holders must confirm that the note is defined as a mirror note and/or contingent payment note, with settlement dependent on Gate’s disclosed hedging and exit arrangements and the handling of unlisted status at maturity in 2035. Company narratives and product terms should be reviewed in parallel.

Summary: In what order should OpenAI IPO risks be reviewed?

The recommended order is: five company-level risks → product terms → individual eligibility and liquidity. This sequence helps avoid treating financing news as direct settlement grounds for notes or inferring inevitable listing from subscription parameters.

FAQ

When will OpenAI IPO?

OpenAI has not announced a definitive IPO date; timing remains one of the structural uncertainties of a private company. Official and public information only confirm that it remains private; the actual window depends on governance structure, regulatory review, financial performance, and market environment, with no definitive timetable available.

What are the risks of an OpenAI IPO?

The five main company-level risks are: cap table and dilution issues due to complex governance and equity structure; AI and data-related regulatory compliance; competition from model alternatives, open source, and compute dependencies; ongoing financing and profitability challenges with high burn rates; and exit uncertainties from IPO delays, M&A, failed listings, and lock-up periods. These risks apply to OpenAI as a company and are different from the terms risks of OPENAI mirror notes.

What if OpenAI doesn’t go public?

If OpenAI remains private long-term or does not IPO within the expected window, private shareholders and secondary market exit timing will be affected, and pre-IPO valuations and liquidity expectations may be adjusted. For Gate OPENAI, the official maturity date is December 31, 2035; if still unlisted, or in the event of acquisition, merger, or bankruptcy, settlement will be based on the fair market value (FMV) of common stock in USDT, and the reference value may also go to zero if the equity is wiped out.

How should OpenAI equity dilution be understood?

New financing, option pool expansion, share reclassification, or M&A consideration may all increase outstanding or potential equity, diluting existing shareholders’ per-share economic interests. OpenAI’s capped-profit and multi-entity structure require more granular analysis of dilution paths than a standard public company; the reference share count for OPENAI’s implied valuation will also adjust with company actions.

What is the relationship between OPENAI notes and OpenAI’s IPO?

OPENAI is a mirror note disclosed by Gate, mapping to OpenAI’s pre- and post-IPO market value, but does not represent actual shares. The company’s IPO progress affects market expectations for the unlisted entity and may trigger product settlement or redemption arrangements as disclosed; however, note holders do not become OpenAI shareholders by default, and rights are governed by the product terms.

Which should be reviewed first: company IPO risks or OPENAI product risks?

Company-level IPO risks—governance, regulatory, competition, financial, and exit—should be reviewed first to understand the unlisted entity, followed by OPENAI’s non-equity nature, reference value, pre-market liquidity, and settlement at maturity. The two layers involve different due diligence objects and are not interchangeable.

What other product risks should be confirmed before trading OPENAI?

Beyond the company’s IPO progress, confirm the mirror note definition, absence of voting or dividend rights, implied valuation and pre-market price differences, account and regional eligibility, post-IPO lock-up, and FMV settlement terms at maturity. These are OPENAI product-level risks and should be reviewed separately from the five company IPO risk categories.