As one of the world’s three major credit rating agencies, Moody’s is not only involved in credit assessment in the bond market, but has also built a large financial infrastructure ecosystem through risk analytics platforms, financial data products, and enterprise software services. For anyone studying global financial markets, understanding Moody’s business model helps explain how capital markets measure and manage risk.

What Is MCO (Moody’s)

MCO is the stock ticker for Moody’s Corporation. Headquartered in New York, Moody’s is one of the world’s most influential credit rating agencies.

Moody’s core business is mainly divided into two segments:

The credit ratings business is mainly responsible for assessing the credit risk of bond issuers and borrowers, while the analytics business provides data, models, software, and research services to banks, insurance companies, asset managers, and corporate clients.

Moody’s ratings are widely used across global bond markets, making its rating system one of the important reference standards in international capital markets.

Moody’s History and Market Position

Moody’s history dates back to 1909.

At the time, financial analyst John Moody began publishing analytical reports on railroad bonds and gradually built a systematic credit rating framework. As the US capital market developed, Moody’s ratings business continued to expand, eventually covering corporate bonds, municipal bonds, financial institution debt, sovereign debt, and other areas.

After more than a century of development, Moody’s has evolved from a traditional rating agency into an important part of the global financial infrastructure.

Today, the global credit rating market is mainly dominated by three agencies:

| Institution |

Headquarters |

| Moody’s |

United States |

| S&P Global Ratings |

United States |

| Fitch Ratings |

United States |

Because rating systems require long term market recognition and accumulated historical data, the barriers to entry in this industry are high, which has led to a highly concentrated market structure.

How Moody’s Credit Ratings Business Works

Credit ratings are Moody’s most representative business segment.

The core purpose of a credit rating is to assess a debt issuer’s ability and willingness to meet its future debt obligations.

When a company, financial institution, or government prepares to issue bonds, it will usually invite a rating agency to conduct a credit assessment. Moody’s analyzes financial data, operating conditions, industry dynamics, cash flow structure, and macroeconomic factors before assigning an appropriate rating.

Moody’s rating system typically includes:

| Rating |

Category |

| Aaa |

Highest credit quality |

| Aa |

High credit quality |

| A |

Upper medium credit quality |

| Baa |

Lowest investment grade range |

| Ba and below |

Speculative grade bonds |

Investment grade ratings are generally viewed as lower risk debt instruments, while speculative grade ratings imply a higher risk of default.

Credit ratings directly affect financing costs. The higher the rating, the more likely the issuer is to obtain financing at a lower interest rate.

Moody’s Analytics and Risk Data Services

As financial markets have become increasingly digital, Moody’s has steadily expanded its analytics and software businesses.

Moody’s Analytics has become one of the company’s important sources of growth.

This segment mainly provides:

-

Risk management software

-

Credit analysis tools

-

Macroeconomic research

-

ESG risk analysis

-

Financial data services

-

Stress testing models

Banks commonly use Moody’s analytics platforms to assess loan portfolio risk.

Insurance companies use related models to estimate potential losses.

Asset managers use data platforms for credit research and investment decision making.

Compared with one time ratings services, analytics services are typically subscription based, allowing them to generate more stable recurring revenue.

Moody’s Role in the Global Bond Market

Moody’s is an important provider of credit information in the global bond market.

The core issue in the bond market is information asymmetry. Investors often cannot directly understand an issuer’s true level of risk, so they need third party institutions to provide professional assessments.

Moody’s ratings play a role across multiple parts of the market.

Bond issuers use ratings to improve financing transparency.

Institutional investors use ratings to screen investment targets.

Banks use ratings to assess loan risk.

Regulators may also use ratings as reference indicators in certain capital regulatory frameworks.

For many large bond issuance projects, obtaining a rating from an international rating agency has become standard market practice.

How Moody’s Differs from S&P Global and Fitch

Although all three agencies provide credit rating services, their business structures differ in some ways.

Moody’s has long been known for its strength in credit ratings and risk analytics.

S&P Global has a broader data and index business, including the well known S&P 500 index system.

Fitch is smaller in market scale, but it has strong influence in certain regional markets and specific debt segments.

The main differences are as follows:

| Dimension |

Moody’s |

S&P Global |

Fitch |

| Core strengths |

Credit ratings and analytics |

Indexes and ratings |

Ratings business |

| Data business |

Strong |

Very strong |

More limited |

| Market share |

Global leader |

Global leader |

Third place |

| Software services |

Relatively comprehensive |

Continuing to expand |

Relatively limited |

From a business model perspective, Moody’s has continued to strengthen its analytics platforms and software services in recent years, aiming to reduce its dependence on bond issuance cycles.

Moody’s Main Use Cases

Moody’s serves many types of financial market participants.

Companies use Moody’s ratings to lower financing costs.

Banks use Moody’s data to assess credit risk.

Insurance institutions use risk models for capital management.

Fund companies use rating results to screen portfolios.

Government departments use ratings to improve transparency in the bond market.

Sovereign countries also often seek credit ratings from Moody’s when issuing international bonds.

As a result, Moody’s business has become embedded in key parts of the global fixed income market.

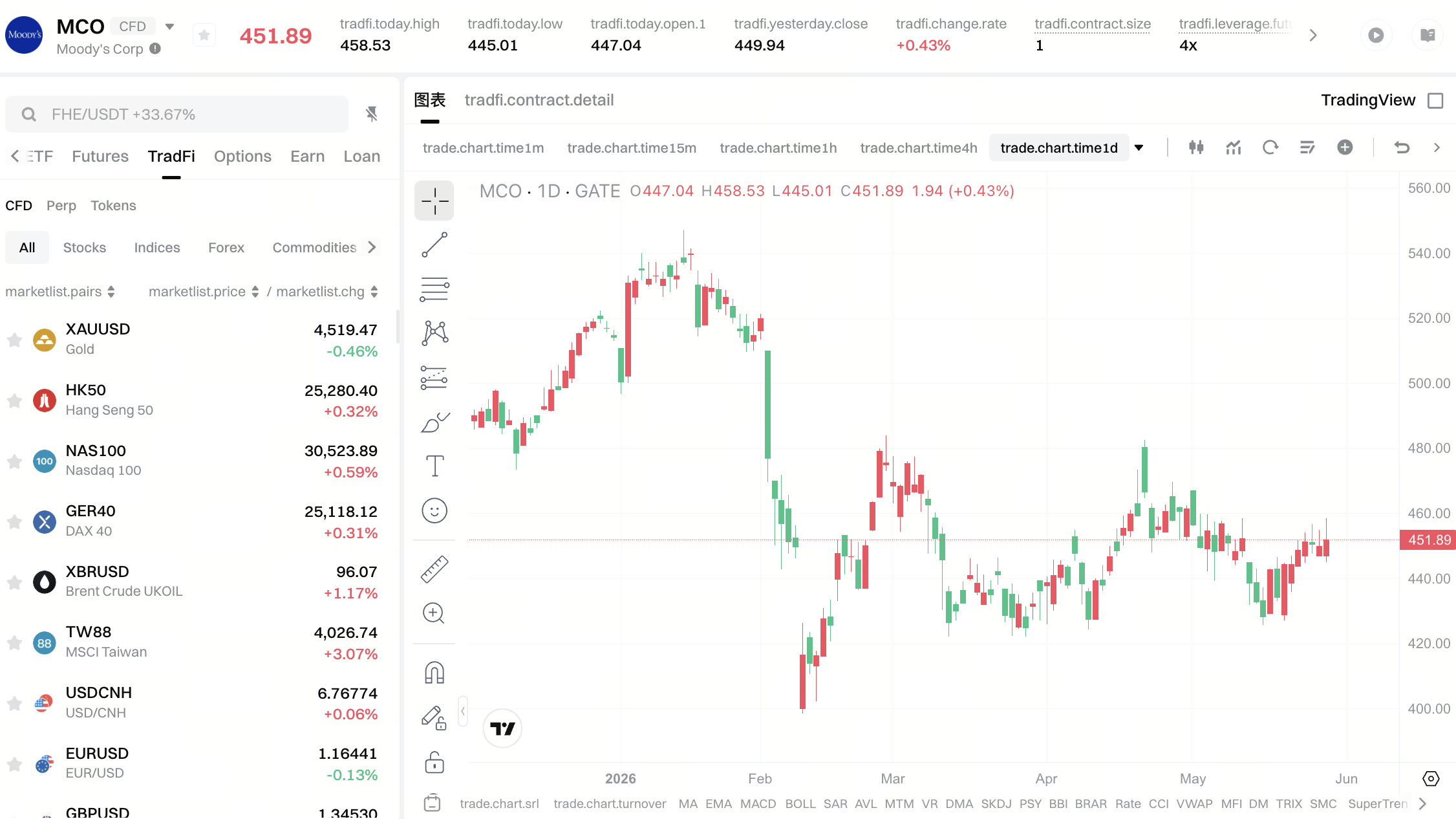

How to Buy MCO (Moody’s) Stock

MCO is listed on the New York Stock Exchange and is one of the important listed companies in the US financial information and credit rating industry.

Investors can buy MCO shares through traditional securities brokers and participate in the potential rewards and risks tied to the company’s operating performance and capital market development.

In addition to traditional stock markets, some digital asset trading platforms also offer CFD products linked to US stock prices. Through markets such as Gate CFD, users can use digital assets to trade related stock price movements.

CFDs are leveraged derivatives, and their trading mechanisms, risk characteristics, and actual ownership features differ from ordinary stocks. Before participating in trading, users should fully understand the product rules and potential risks.

Moody’s Strengths and Limitations

Moody’s greatest strength comes from its long established brand credibility and industry barriers.

The credit rating industry requires market trust to be built over a long period of time, making it difficult for new entrants to gain broad recognition quickly.

Moody’s also has extensive historical databases, professional analytical teams, and a global client network, all of which further strengthen its competitive advantages.

At the same time, Moody’s also faces certain limitations.

The credit ratings business is closely tied to bond issuance activity. When capital market financing demand declines, ratings revenue may be affected.

In addition, the ratings industry has long faced debate over potential conflicts of interest. Because rating fees are usually paid by issuers, the market continues to pay close attention to the independence of ratings.

Conclusion

MCO (Moody’s) is a major representative of the global credit rating industry, with businesses spanning credit ratings, risk analytics, financial data, software services, and more. As an important infrastructure provider for global capital markets, Moody’s helps investors, financial institutions, and companies assess credit risk and improve market transparency. As demand for risk management continues to grow, analytics services and data businesses have become important parts of Moody’s business model, gradually transforming the company from a traditional rating agency into a comprehensive financial information services provider.

FAQs

What Does Moody’s Mainly Do?

Moody’s mainly provides credit ratings, risk analytics, financial data services, and enterprise risk management software. Its clients include companies, banks, insurance institutions, governments, and investment institutions.

Why Is Moody’s Important in Financial Markets?

Moody’s provides independent credit risk assessments that help investors evaluate a debt issuer’s ability to repay its obligations, thereby improving information transparency and capital allocation efficiency in capital markets.

What Does Aaa Mean in Moody’s Ratings?

Aaa is the highest credit rating in Moody’s rating system. It usually indicates extremely low default risk and very strong debt repayment capacity.

How Is Moody’s Different from S&P Global?

Moody’s focuses more on credit ratings and risk analytics, while S&P Global, in addition to its ratings business, has a broad system of data, index, and market information services.

What Are Moody’s Revenue Sources?

Moody’s revenue mainly comes from credit rating services, as well as the data, software, research, and risk management solutions provided by Moody’s Analytics.

What Industry Does MCO Stock Belong To?

MCO is generally classified under the financial services and financial information industries. Its business spans credit ratings, financial data, risk management, and enterprise software services.