As one of China's largest DRAM manufacturers, CXMT’s stock narrative is deeply intertwined with the global memory cycle, AI Hashrate demand for memory, and the push for semiconductor supply chain independence.

Prior to its official listing, various CXMT-related trading formats had already appeared: the A-share STAR Market offers a traditional equity route; Hyperliquid has introduced Pre-IPO perpetual contracts under the HIP-3 framework; and Gate has launched the CXMT_USDT pre-market perpetual, which is a stock derivative rather than a gStocks tokenized security. To fully understand the CXMT DRAM business structure, it’s important to distinguish the company’s fundamentals, the product attributes of the three participation routes, and the specific rights and risk boundaries for each.

ChangXin Memory Technologies (CXMT) is a leading DRAM manufacturer in China, specializing in the R&D and mass production of memory chips. CXMT refers to its planned or listed holding/operating entity. In the context of A-shares, CXMT typically means this listed platform and its corresponding stock code.

In summary: ChangXin Memory Technologies holds the DRAM business and production capacity, while CXMT, as the listed entity, connects with capital markets. For stock analysts, evaluating CXMT should focus on DRAM revenue structure, capacity ramp-up, market share shifts, and advances in technology and HBM (High Bandwidth Memory), rather than simply classifying it as a generic semiconductor manufacturer.

| Entity |

Positioning |

Key Analysis Focus |

| ChangXin Memory Technologies |

DRAM manufacturing & R&D |

Products, capacity, market share |

| CXMT |

Listed entity / equity vehicle |

Financials, fundraising use, governance structure |

| CXMT (on-chain) |

Derivative ticker |

Contract rules, non-registered equity |

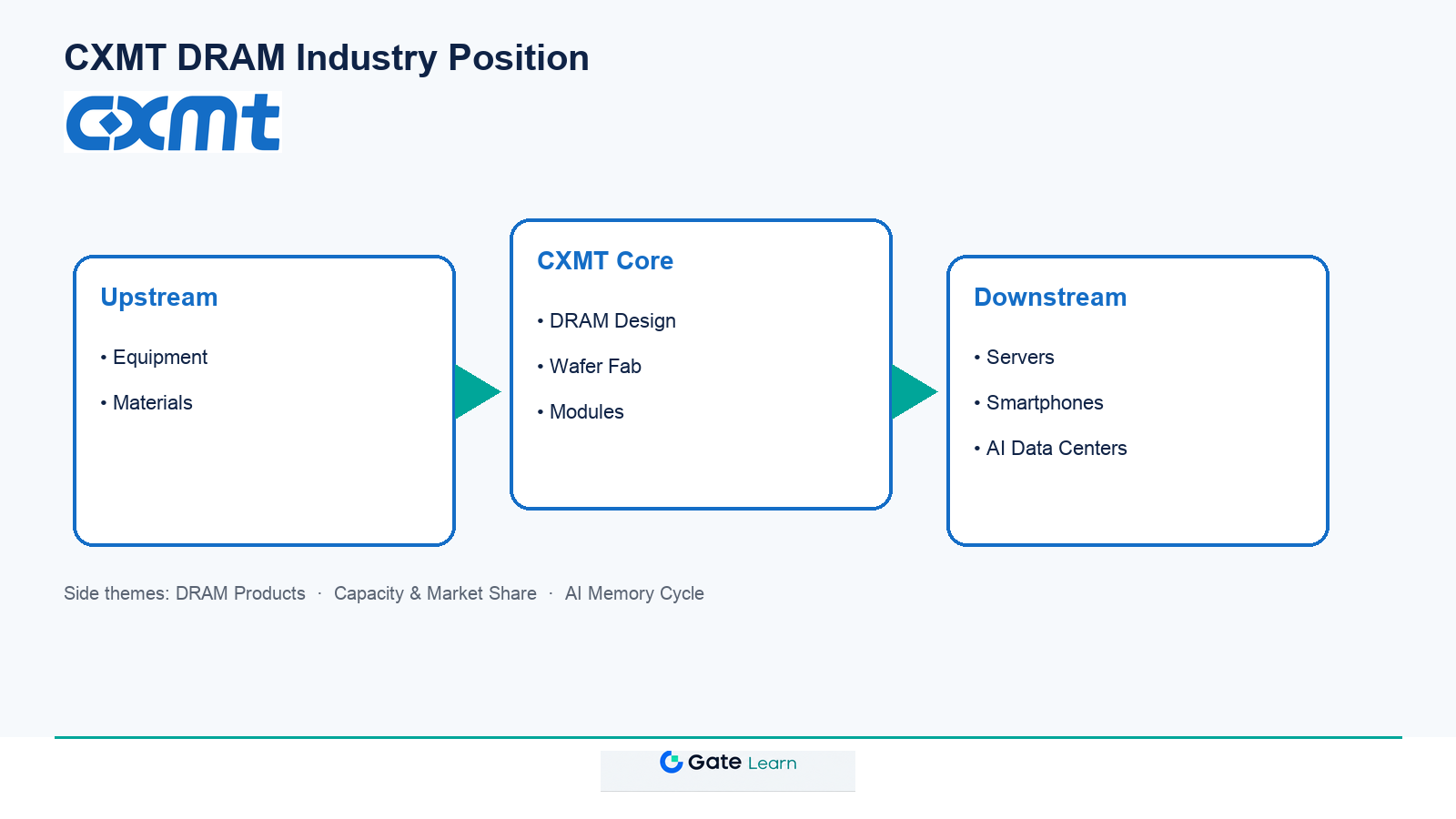

How Does CXMT’s DRAM Business Operate? Where Does It Stand in the Industry Chain?

DRAM is at the core of the memory industry chain: upstream are equipment and material suppliers, downstream are servers, smartphones, PCs, and AI accelerator cards. CXMT’s DRAM competitive landscape shows that global leaders include Samsung Electronics, SK Hynix, and Micron Technology. CXMT continues to expand in standard DRAM, gradually increasing its market share, but still trails the leaders in high-end segments like HBM.

CXMT’s revenue model is driven by DRAM shipment volumes and product mix: mature products such as DDR4 and LPDDR4 support scale, while advanced nodes and high-end products drive long-term competitiveness. The AI-driven memory supercycle has boosted industry sentiment, but cyclical volatility, equipment access restrictions, and R&D pace remain key structural factors impacting fundamentals.

Figure 1. CXMT’s role in the DRAM industry chain: upstream equipment/materials, core DRAM manufacturing, and downstream AI/consumer electronics demand.

Figure 1. CXMT’s role in the DRAM industry chain: upstream equipment/materials, core DRAM manufacturing, and downstream AI/consumer electronics demand.

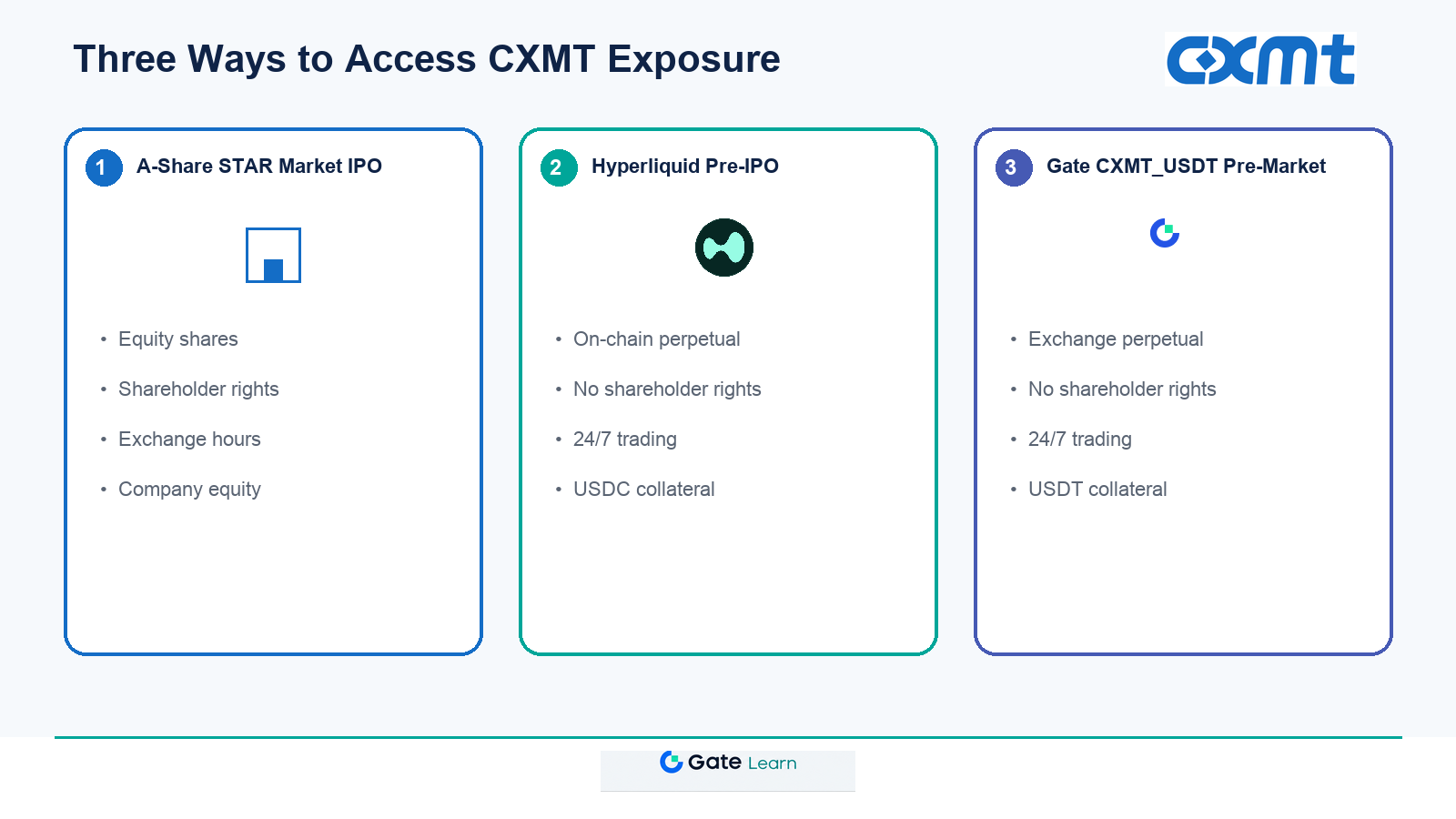

How Can Investors Access CXMT? Three Participation Routes Overview

Currently, there are three main ways to participate in CXMT, each with distinct product features and rights boundaries. How investors can participate in CXMT compares these across conditions, process structure, and rights differences; here is a high-level summary.

| Route |

Product Type |

Registered Equity |

Typical Participants |

| A-share STAR Market IPO/Secondary |

Listed equity |

Yes |

Qualified domestic investors |

| Hyperliquid Pre-IPO |

HIP-3 perpetual contract |

No |

Global users with on-chain trading access |

| Gate CXMT_USDT |

Pre-market perpetual contract |

No |

Gate contract users |

The A-share route offers legal equity ownership and shareholder rights; Hyperliquid and Gate provide derivative exposure to CXMT’s expected share price, without IPO allocation, dividends, or voting rights, and cannot be directly converted into A-share holdings after listing.

Figure 2. Comparison of three CXMT participation routes: A-share equity, Hyperliquid Pre-IPO contract, and Gate pre-market perpetual.

Figure 2. Comparison of three CXMT participation routes: A-share equity, Hyperliquid Pre-IPO contract, and Gate pre-market perpetual.

How Does the CXMT Pre-IPO Contract Function on Hyperliquid?

Hyperliquid’s HIP-3 framework enables third parties to deploy Pre-IPO perpetual contract tickers. The CXMT contract tracks the expected RMB price of one A-share and converts it to USD using the exchange rate, settled in USDC. Hyperliquid CXMT mechanism explains mark pricing, funding rates, and IPOP rules in detail.

Before listing, the contract price is primarily determined by on-chain order book supply and demand, without an enforceable external spot oracle. After listing, the contract is expected to follow standard perpetual pricing logic, with external A-share prices included in the index calculation. Holding a CXMT contract reflects a directional view on CXMT’s public market price, not actual equity ownership.

What Is Gate’s CXMT_USDT Pre-Market Perpetual?

Gate’s CXMT_USDT is a stock-type pre-market perpetual contract (is_pre_market), settled in USDT, supporting leveraged long and short positions. This product differs from gStocks tokenized securities (such as SKHYNIXG, MUG, etc., which are mapped 1:1 to real stock reserves): Gate has not yet launched a gStocks spot product for CXMT.

Before sufficient external spot data is available, the pre-market perpetual’s index price may use internal platform pricing; after listing, it is expected to transition smoothly according to Gate’s rules for converting pre-market to official perpetuals. Users on Gate must confirm the product is a contract, not a tokenized equity, and review leverage, margin, and liquidation rules.

What Are the Advantages and Risks of Holding or Trading CXMT Exposure?

Each route offers distinct advantages in accessibility, trading hours, and rights structure, but also comes with unique risks.

| Advantage |

Description |

| Multiple routes |

A-share, on-chain, and Gate contracts cover different jurisdictions and account types |

| On-chain/contract 24/7 |

Hyperliquid and Gate are not limited by traditional market hours |

| Two-way trading |

Contracts support shorting for hedging or contrarian strategies |

| Risk Type |

Main Source |

| Pricing deviation |

Contract prices may diverge significantly from A-share IPO or post-listing spot prices |

| Liquidity |

Low order book depth may increase slippage |

| Rule changes |

Changes to platform contract parameters, HIP-3 rules, or regional restrictions |

| Fundamentals |

DRAM cycle, HBM technology gap, equipment controls |

| Operational |

Ticker selection errors, excessive leverage, insufficient margin |

The Hyperliquid trading process provides a step-by-step overview of the on-chain route’s execution and operational checkpoints. Any route should be chosen based on a clear understanding of product features and risk mechanisms, not just price trends.

Summary

CXMT is the listed entity of ChangXin Memory Technologies, with its DRAM business and global memory competition forming the core of its stock narrative. Investors can currently gain exposure through the A-share STAR Market, Hyperliquid Pre-IPO contracts, and Gate CXMT_USDT pre-market perpetuals, with the latter two as derivatives rather than registered equity. Understanding CXMT requires analyzing the company’s business, the differences among the three routes, and each mechanism’s risks and compliance boundaries.

FAQ

What Kind of Company Is CXMT?

CXMT is the listed entity of ChangXin Memory Technologies, focusing on the design, manufacturing, and sales of DRAM memory chips. In the A-share context, CXMT refers to the listed platform and its stock code; on-chain, it often refers to Pre-IPO contract tickers on platforms like Hyperliquid.

What Is the Relationship Between ChangXin Memory Technologies and CXMT?

ChangXin Memory Technologies is responsible for DRAM R&D and mass production, while CXMT, as the listed entity, connects with capital markets. When analyzing CXMT stock, focus on the DRAM business’s financials and competitive position, rather than conflating the two entities.

Is On-Chain CXMT an Equity Stock?

On-chain CXMT (such as Hyperliquid Pre-IPO contracts) is not an A-share registered stock, but a perpetual contract tracking CXMT’s expected price. Holding the contract does not grant IPO allocation, dividends, or voting rights, nor can it be directly converted into A-share holdings.

What Are the Differences Between A-Share IPO, Hyperliquid, and Gate Pre-Market Contracts?

The A-share route offers legal equity ownership; Hyperliquid and Gate offer derivative exposure, settled in USDC or USDT, supporting leverage and two-way trading. The three differ structurally in position type, shareholder rights, trading hours, and pricing anchors.

Does Gate Offer CXMT gStocks?

Gate has not yet launched a gStocks spot product for CXMT, but does provide the CXMT_USDT pre-market perpetual contract. gStocks are mapped 1:1 to real stock reserves and are a separate product line from pre-market perpetuals.

What Are the Risks of Trading CXMT Exposure?

Key risks include contract price deviation from A-share spot prices, limited order book liquidity, changes in platform rules or regional restrictions, DRAM industry cycle fluctuations, as well as leverage operations and ticker selection errors. Derivative routes do not eliminate fundamental or operational uncertainties.