Public listing requires HOOD to continuously disclose its business activities, risk factors, and financial information. Treating these disclosures as a compliance roadmap helps clarify the regulatory environment behind each revenue item and allows for cross-verification with the transactional revenue and net interest logic outlined in the HOOD Stock Business Model.

Crypto and on-chain products bring additional considerations around custody and transparency. For further details, refer to HOOD Crypto and Robinhood Chain and Security Compliance and Transparency. For a comparison of regulatory priorities with Coinbase, see HOOD vs COIN.

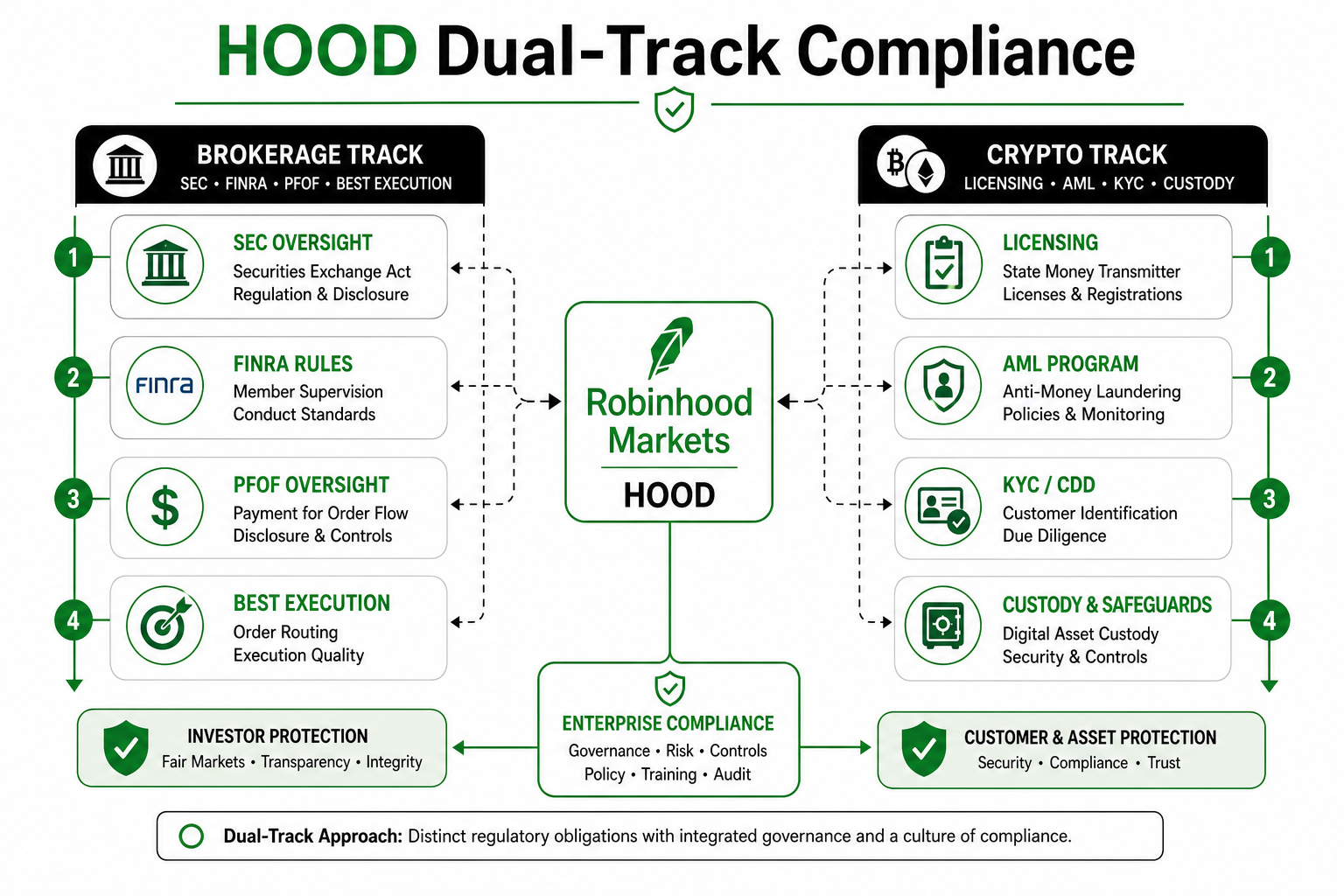

What Are the Main Regulatory Frameworks Governing HOOD?

On the brokerage side, Robinhood Markets (HOOD) and its subsidiaries must comply with securities brokerage registration, client protection, reporting, and supervisory requirements, which involve a multi-layered structure including SEC, FINRA, and clearinghouse rules. On the crypto side, operations must meet applicable money transmission licensing, anti-money laundering (AML)/know your customer (KYC) obligations, and adapt to evolving digital asset classifications and market structure regulations.

| Track |

Typical Constraints |

Significance |

| Brokerage |

Registration, client assets, best execution, reporting |

Shapes the regulatory environment for transactional revenue |

| Crypto Services |

Licensing, AML/KYC, asset custody |

Impacts the availability and cost of crypto products |

| Public Company |

Disclosure, internal controls, governance |

Affects the quality of information available to investors |

| International Growth |

Local licensing and product customization |

Influences the geographic distribution of revenue |

This table establishes a “multi-track parallel” perspective. Different subsidiaries and product lines in various countries may fall under different licenses; it is inaccurate to generalize all operations under a single “SEC regulation.”

How Should the PFOF Controversy Be Understood?

Payment for order flow (PFOF) is an arrangement where brokers may receive compensation for routing retail orders to market makers or other execution venues. Proponents argue that competition improves pricing; critics highlight potential conflicts of interest and concerns about whether execution quality is adequately disclosed. For HOOD, PFOF-related revenue is a significant component of transactional income, making regulatory stances on PFOF a structural focus.

To properly assess the controversy, consider three aspects: the market mechanism (how orders are routed), disclosure obligations (whether clients can evaluate execution quality), and revenue dependence (the materiality of this item in financial reports). The existence of controversy does not imply illegality; rather, it signals that this revenue source is sensitive to regulatory changes.

What Are the Key Compliance Considerations for Crypto Business?

Crypto compliance typically centers on which assets can be listed, whether they qualify as securities, how custody responsibilities are allocated, how cross-border transfers satisfy AML requirements, and whether advertising and investor protection statements are compliant. Robinhood delivers crypto services through different entities in various jurisdictions, resulting in differences in product offerings and features.

On-chain and self-custody scenarios introduce additional dimensions: self-custody of private keys reduces platform responsibility but shifts operational risk to users; permissionless networks increase composability as well as smart contract and bridging risks. These product-level issues shape compliance design but do not alter HOOD’s core disclosure narrative as an equity issuer.

Figure 1. HOOD dual-track regulatory structure: brokerage rules (including PFOF) and crypto compliance requirements jointly constrain operations.

Figure 1. HOOD dual-track regulatory structure: brokerage rules (including PFOF) and crypto compliance requirements jointly constrain operations.

What Are the Access Points for Disclosures and Investor Relations?

The investor relations website is the central source for annual reports, quarterly reports, investor presentations, and governance documents, serving as the primary reference for business descriptions and risk factors. The SEC EDGAR system provides full statutory filings, which can be cross-checked with company disclosures. When reviewing, focus on the business overview, revenue recognition notes, and Risk Factors sections related to brokerage, PFOF, crypto, and cybersecurity.

Disclosures address “what the company has stated”; enforcement actions and rulemaking documents address “how the regulatory environment is changing.” Both should be treated as factual sources, not trading signals.

What Structural Risks Should Be Stated Separately?

Regulatory and Litigation Risks: Changes in rules, investigations, or lawsuits may result in fines, operational adjustments, or product delistings.

Market and Revenue Structure Risks: Lower trading volume impacts transactional revenue, while interest rate changes affect net interest income.

Operational and Security Risks: System outages, fraud, and mismanagement of client assets.

Competition and Reputational Risks: User migration to traditional brokers and other fintech platforms.

These risks describe potential mechanisms for a risk checklist and do not constitute investment ratings or recommendations for HOOD stock.

How Should Client Asset Protection and Operational Disruptions Be Reflected in the Risk Map?

Client asset protection rules require brokers and related entities to meet industry standards for recordkeeping, segregation, and reporting, aiming to reduce the risk of misappropriation or commingling of client securities and cash. Public risk factors also typically mention system outages, cyberattacks, fraudulent transactions, and reliance on third-party services: while these may not immediately impact revenue, they can increase operating costs and affect reputation.

When mapping asset protection and secure operations, distinguish three areas: fulfillment of statutory obligations, effectiveness of technical controls, and the mechanisms for client communication and compensation after incidents. For HOOD stock observers, major incidents are company-level events that require review of their impact in disclosure documents, not reliance on isolated social media rumors.

What Are the Limitations of Compliance Discussions?

Limitation 1: Public articles cannot exhaustively cover all licenses and subsidiary structures. Limitation 2: Rules are evolving, so evergreen statements only describe the framework type and cannot substitute for reviewing current statutory filings. Limitation 3: On-chain transparency tools do not automatically fulfill statutory brokerage obligations. Limitation 4: Peer comparisons only highlight differences in regulatory focus and do not indicate relative “safety.”

Therefore, the purpose of the compliance section is to help readers ask the right questions: which business line, which license, which revenue item, which risk factor. A checklist of questions is more valuable for knowledge sharing than definitive conclusions.

Summary

HOOD’s regulatory landscape features a dual-track structure of brokerage rules and crypto compliance, with PFOF, client asset protection, AML/KYC, and public company disclosure collectively shaping operational boundaries. Understanding this structure allows for better correlation between revenue fluctuations and regulatory changes, and prevents misinterpreting on-chain product risks as direct equity compliance conclusions.

FAQ

What Regulations Apply to HOOD Stock?

As a public company and brokerage group, HOOD entities are subject to SEC and other securities regulations, FINRA self-regulation, and applicable crypto business licensing and AML rules. International products are also subject to local licensing requirements.

What Is PFOF and Why Is It Frequently Mentioned?

PFOF is an order routing compensation arrangement tied to the microstructure of retail order execution. Robinhood’s transactional revenue is closely related, which is why regulatory discussions often highlight it as a key focus.

Are Crypto Business Compliance and Brokerage Compliance the Same?

No. Brokerage compliance emphasizes securities trading, client protection, and execution quality; crypto compliance focuses on asset classification, custody, transfers, and anti-money laundering. Both may exist in different product lines within the same group.

What Risks Are Involved in Trading Robinhood Stock?

Beyond price volatility, risks include regulatory and litigation exposure, changes in revenue structure driven by trading volume and interest rates, operational security, competition, and reputation. There are also execution risks, such as code selection errors and fee rule risks.

Where Can Official Disclosures Be Verified?

You can review annual reports, quarterly reports, and risk factor sections on the Robinhood investor relations website and SEC EDGAR, using statutory filings as the standard for verification.