For modern banks, profitability depends not only on loan volume, but also on customer scale, assets under management, the interest rate environment and risk control capabilities. PNC has maintained an important position in the U.S. regional banking market over the long term largely because it has built an integrated financial ecosystem spanning personal finance, corporate finance and wealth management.

PNC’s businesses cover commercial banking, retail banking, wealth management and corporate financial services, serving individual consumers, small and medium sized businesses, large corporations and institutional investors. Compared with community banks, PNC has broader service capabilities. Compared with global financial institutions such as JPMorgan Chase, PNC is more focused on the U.S. domestic market.

PNC is the ticker symbol for PNC Financial Services Group, which is listed and traded on the New York Stock Exchange in the United States. The company is headquartered in Pittsburgh, Pennsylvania, and is one of the largest regional banking groups in the United States by asset size.

Within the U.S. banking industry, PNC is often seen as an important representative of the regional banking sector. Its operating performance is closely tied to U.S. economic growth, loan demand, consumer spending and interest rate changes, making it one of the important companies for observing the U.S. financial industry.

PNC’s Revenue Sources

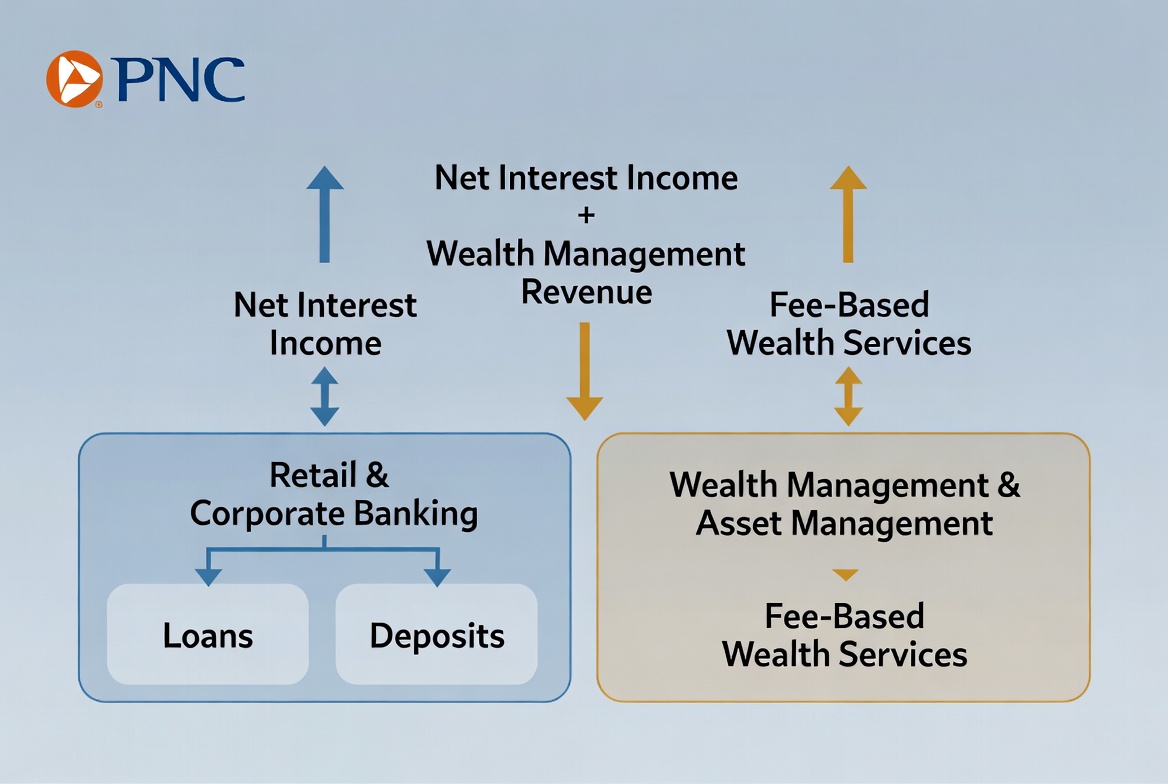

PNC’s revenue can mainly be divided into two categories: interest income and non interest income. Interest income has long played the central role, while wealth management and corporate financial services continue to increase the importance of non interest income.

The most traditional banking profit model comes from deposits and lending. PNC accepts customer deposits as a source of funding, then provides loans to individuals and businesses, earning income from the difference between loan interest and deposit costs. This revenue model is known as net interest income, and it is the most important source of revenue for most banks.

At the same time, modern banks are placing greater emphasis on non interest income. Wealth management, investment advisory, cash management, payment services and capital markets businesses can all generate fee income. Because this type of income does not directly depend on loan volume, it helps strengthen the stability and diversification of a bank’s revenue structure.

| Revenue Source |

Main Content |

| Interest income |

Personal loans, commercial loans, credit products |

| Wealth management income |

Investment advisory fees, asset management fees |

| Corporate finance income |

Cash management, financing services |

| Service fee income |

Payment, account and transaction services |

This revenue structure allows PNC to maintain relatively balanced development across different economic environments.

How Deposits and Lending Generate Revenue

Deposits and lending are the foundation of PNC’s business model and the classic source of profit in the banking industry. Banks obtain funds by accepting public deposits, then allocate those funds into lending activities, creating a cycle of capital.

For individual customers, loan products include mortgages, auto loans, credit lines and credit card services. For corporate customers, they include operating loans, equipment financing, commercial real estate loans and merger and acquisition financing. These loan products generate interest income and become an important source of bank profits.

The key to bank profitability lies in managing the interest spread. Put simply, the interest rate PNC pays to depositors is usually lower than the rate it charges on loans, and the difference between the two forms net interest income. For example, when a bank attracts deposits at a relatively low cost and lends those funds at a higher rate, it can generate stable returns.

Still, lending is not without risk. Banks need to assess borrowers’ credit profiles and repayment capacity to reduce default risk. For that reason, risk management capability is also an important factor in determining the profitability of deposits and lending.

How Wealth Management Contributes to Growth

As customer assets continue to grow, wealth management has become one of the most important growth areas for modern banks. For PNC, wealth management not only brings in additional revenue, but also helps build long term customer relationships.

Wealth management mainly serves high net worth clients, families and institutional investors. Services include asset allocation, retirement planning, investment advisory, trust services and wealth transfer planning. Unlike lending, wealth management places greater emphasis on long term asset growth and risk management.

An important feature of wealth management is its relatively stable revenue model. Many asset management products charge management fees based on the size of client assets, so bank revenue can grow as client assets increase. This model can reduce the bank’s dependence on loan demand and interest rate cycles.

For PNC, wealth management has become an important part of business upgrading. As the U.S. population ages and accumulated wealth continues to grow, demand for investment planning and wealth transfer is also increasing, creating long term room for growth in wealth management.

How Corporate Financial Services Expand the Revenue Structure

Corporate financial services are one of the areas that distinguish PNC from ordinary retail banks. Compared with personal banking, corporate finance often involves more complex funding needs and higher value financial services.

Corporate clients usually need financing support for business expansion, equipment purchases or working capital management. In addition to traditional lending, PNC also provides cash management, payment settlement, trade finance and capital markets services, helping companies improve the efficiency of fund operations.

Large companies often require more specialized financial solutions. Services such as cross border payments, foreign exchange risk management, bond issuance advisory and merger and acquisition financing are all important parts of corporate finance. These businesses can generate fee income while also strengthening customer loyalty.

By covering different stages of corporate development, PNC can build long term partnerships. For banks, corporate clients represent not only lending income, but also more cross selling opportunities, further expanding revenue sources.

Why the Interest Rate Environment Affects Bank Profitability

The interest rate environment is one of the most important external factors affecting bank profitability. Because banks essentially profit from the difference between funding costs and loan returns, changes in interest rates directly affect net interest income.

When interest rates rise, rates on new loans usually rise as well. If deposit costs increase more slowly, banks may be able to widen their net interest margin and improve profitability. In some periods, a rising rate environment can therefore support bank revenue growth.

However, higher interest rates do not always have a positive effect. Elevated rates can reduce loan demand and increase repayment pressure for some borrowers. If economic growth slows or default rates rise, banks may still face operating pressure.

For a regional bank such as PNC, the interest rate environment affects not only loan yields, but also customer deposit behavior and broader financial market activity. As a result, the interest rate cycle is often an important reference point for investors analyzing banking sector performance.

Conclusion

PNC’s business model is built on deposits and lending, wealth management and corporate financial services. Interest income remains its most important revenue source, while wealth management and corporate finance help PNC build a more diversified profit structure. At the same time, the interest rate environment, loan demand and risk management capabilities continue to shape the bank’s operating performance. Through an integrated financial services system covering both individual and corporate clients, PNC has become an important participant in the U.S. regional banking market.

FAQs

How does PNC mainly make money?

PNC mainly generates revenue through loan interest income, wealth management service fees, corporate financial service fees, and payment and account management fees.

What is net interest income?

Net interest income is the difference between the interest a bank earns on loans and the interest it pays on deposits. It is one of the most important sources of bank profit.

Why is wealth management important?

Wealth management can generate stable management fee income and help banks reduce dependence on lending and interest rate cycles.

What do corporate financial services include?

Corporate financial services usually include commercial loans, cash management, payment settlement, trade finance and capital markets related services.

How do interest rate changes affect PNC’s profitability?

Interest rate changes affect loan yields, deposit costs and loan demand, so they directly influence a bank’s net interest income and overall profitability.

Is PNC a regional bank or a national bank?

PNC is generally classified as a large regional bank. Its business covers multiple U.S. states, but it remains primarily focused on the U.S. domestic market.