In Korean equity research, "LG vs Samsung" is often reduced to a battle of TV brands, overlooking the structural impact of semiconductors on Samsung Electronics' financial statements and the automotive cycle exposure brought by LG Electronics' vehicle solutions segment. Clarifying the business divisions of both listed entities is fundamental for meaningful peer analysis after reviewing the LG Electronics overview. The comparison is intended to establish analytical boundaries and does not imply any judgment regarding the merits of either company.

What Is LG Electronics?

LG Electronics Inc. is a South Korean consumer electronics and vehicle solutions company listed on the KOSPI. Its operations are organized into three main segments: Home Appliance & Air Solution (H&A), Home Entertainment (HE), and Vehicle Component Solutions (VS). LG Electronics does not engage in wafer manufacturing; its revenue streams are derived from home appliances, OLED and QNED TVs, and in-vehicle infotainment and display systems for automakers.

Within the LG Group, LG Electronics is independently listed alongside LG Chem and LG Display. The LG Electronics Business Model illustrates the operational logic of each division in terms of revenue recognition, business segmentation, and intra-group procurement. When searching for financial reports or trading pages, always verify the full company name to avoid confusion with other group entities such as LG Display.

What Is Samsung Electronics?

Samsung Electronics Co., Ltd. is a flagship technology company under Samsung Group, focusing on semiconductors, mobile devices, and consumer electronics, and is listed on the KOSPI. Samsung Electronics organizes its business into Device eXperience (DX) and Device Solutions (DS): DX includes smartphones, TVs, home appliances, and network equipment; DS encompasses memory chips, logic chips, and foundry services, with the semiconductor business typically contributing a significant share of revenue and operating profit.

Unlike LG Electronics, Samsung Electronics manages both chip design and manufacturing as well as end-brand sales. The Galaxy smartphone series, Neo QLED TVs, and DRAM/NAND memory chips represent three distinct profit chains: mobile, display, and semiconductors. When comparing to LG Electronics, it's essential to factor in the impact of the semiconductor business, rather than limiting analysis to TVs or home appliances.

How Do Business Structures and Semiconductor Exposure Differ?

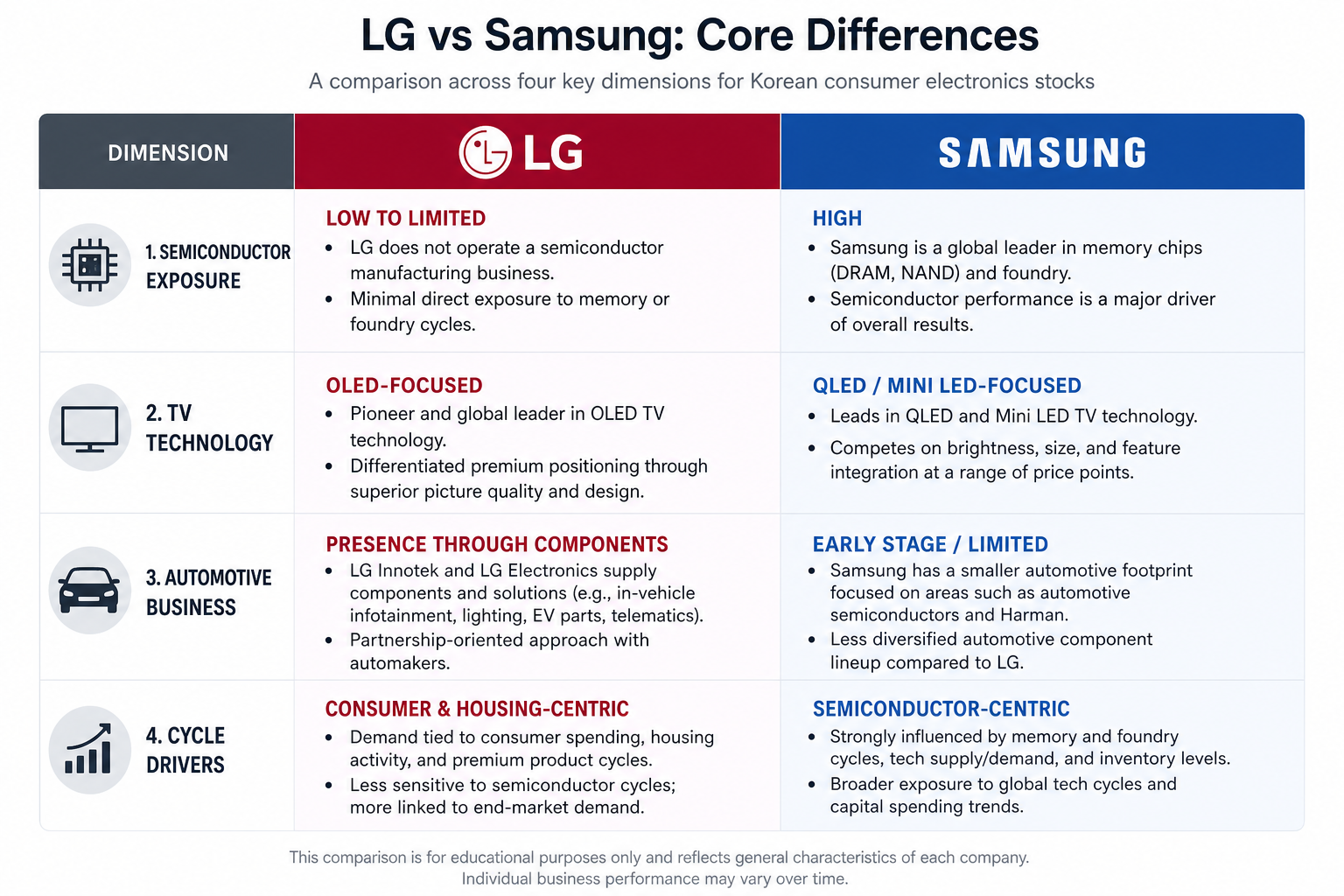

The core structural differences between LG Electronics and Samsung Electronics lie in "whether wafer manufacturing is present" and "segment profit weighting." LG Electronics' three segments focus on finished products, branding, and vehicle system integration. Components such as panels may be sourced from LG Display, but LG Electronics does not produce memory or logic chips. Samsung Electronics' DS division is directly involved in the global memory and foundry market, and chip price cycles have a much greater impact on its financials than on LG Electronics.

| Comparison Dimension |

LG Electronics |

Samsung Electronics |

| Semiconductor Manufacturing |

None |

Memory, logic chips, foundry |

| Core Revenue Segments |

H&A, HE, VS |

DX, DS |

| Smartphones |

Not a main business |

Galaxy series as core product line |

| Panel Role |

TV integrator |

Manufactures panels for end products |

| Automotive Strategy |

VS segment operates independently |

Components and system solutions |

| Main Cyclical Drivers |

Home appliance demand, TV competition, automotive contracts |

Chip pricing, mobile shipments, display demand |

This table summarizes structural differences from an industry value chain perspective. When semiconductor market conditions fluctuate, Samsung Electronics may experience profit elasticity through its DS segment that LG Electronics does not; during consumer slowdowns, both companies may be affected by weaker demand for home appliances and TVs, but the impact pathways differ due to segment weighting.

Figure 1. Business segment division and semiconductor exposure: LG Electronics focuses on home appliances, TVs, and vehicle solutions, while Samsung Electronics is anchored by semiconductors and mobile devices.

How Do TV and Home Appliance Competitiveness Compare?

TVs and home appliances are the most directly comparable sectors for the two companies, but their technological approaches differ. LG Electronics’ HE segment focuses on OLED self-emissive displays, while H&A covers refrigerators, washing machines, air conditioners, and air purifiers. Samsung Electronics pursues multiple TV technologies including QLED and Neo QLED, and its home appliance business competes directly with LG Electronics in many global markets.

| Category |

LG Electronics |

Samsung Electronics |

| Main TV Technology |

OLED, QNED |

QLED, Neo QLED |

| TV Operating System |

webOS |

Tizen |

| Core Home Appliance Categories |

Refrigerators, washing machines, air conditioners, purifiers |

Refrigerators, washing machines, air conditioners, etc. |

| Competitive Focus |

High-end OLED AV, energy-efficient appliances |

Quantum dot TVs, smart home ecosystems |

The TV and home appliance markets are highly competitive, with market share and raw material costs impacting segment performance. The comparison above describes differences in product and technology strategy, not brand superiority. For LG Electronics’ TV operations, see the LG Electronics Risk Metrics Checklist for further analysis of competition and segment indicators.

Market Capitalization Structure and Valuation Methodology Differences (Mechanism Explanation, Not Investment Advice)

Differences in market capitalization and valuation multiples between LG Electronics and Samsung Electronics reflect divergent business structures, profit sources, and capital market pricing logic. Market capitalization is calculated as share price times total shares outstanding; volatility in segment profits, capital expenditure intensity, and reinvestment needs influence the valuation frameworks used by the market.

Because semiconductors comprise a large share of Samsung Electronics’ business, the market often interprets its profit volatility through chip cycles and capital expenditure trends. LG Electronics, lacking wafer manufacturing, is priced more on home appliance and TV competition, the VS segment’s contract cadence, and intra-group transaction metrics. The comparability of valuation indicators such as price-to-earnings (P/E) and price-to-book (P/B) depends on profit stability and accounting policy consistency.

| Valuation-Related Mechanism |

LG Electronics |

Samsung Electronics |

| Profit Volatility Drivers |

Home appliances, TV competition, auto contracts |

Chip prices, mobile shipments, display demand |

| Capital Expenditure Profile |

Finished product lines, vehicle solution R&D |

Advanced processes, memory capacity expansion |

| Common Valuation Benchmarks |

Consumer electronics, automotive electronics solution providers |

Integrated semiconductor + consumer electronics |

Valuation metrics reflect market expectations for future performance. When directly comparing valuation multiples, first confirm whether business structure differences allow for meaningful profit comparability. The above explanation describes mechanism differences only and does not constitute investment advice or price targets.

Figure 2. Four core dimensions of differentiation for Korean consumer electronics stocks: business focus, semiconductor exposure, TV technology path, and cyclical drivers.

What Are the Limitations in Comparison?

There are structural limitations in directly comparing LG Electronics and Samsung Electronics: LG Electronics must be analyzed separately from LG Display and LG Chem, while Samsung Electronics integrates chips and end products within one entity, resulting in different segment disclosure granularity. LG Electronics procures panels from LG Display, so related-party transactions should be considered when comparing gross margins. Semiconductor industry logic cannot be directly applied to LG Electronics, as the VS and H&A segments follow their own cycles. Differences in capital expenditure and R&D policy also affect the comparability of P/E and P/B ratios.

Summary

LG Electronics and Samsung Electronics are frequently compared in the Korean consumer electronics equity space, with key differences centered on semiconductor exposure and business boundaries: Samsung Electronics is anchored by memory and logic chips and covers smartphones and displays, while LG Electronics focuses on home appliances, OLED TVs, and vehicle solutions, and does not engage in wafer manufacturing. Although there is direct competition in TVs and home appliances, the technology paths and profit structures differ. Effective comparison requires attention to financial disclosure granularity, related-party transactions, and segment weights, and an awareness of the limits of simple multiple-based comparisons.

FAQ

What is the biggest business difference between LG Electronics and Samsung Electronics?

The most significant difference is semiconductor exposure: Samsung Electronics operates memory and logic chip manufacturing, with semiconductors typically accounting for a major share of revenue and profit. LG Electronics does not engage in wafer manufacturing, and its revenue is concentrated in home appliances, OLED TVs, and vehicle component solutions.

Why can’t LG Electronics be compared solely by its TV business?

LG Electronics’ revenue comes from H&A, HE, and VS segments, with TVs only part of the HE segment. Vehicle solutions are tied to the automotive cycle, and home appliances provide stable cash flow. Focusing only on TVs ignores the structural impact of the VS and H&A segments.

How do the TV technology paths of LG Electronics and Samsung Electronics differ?

LG Electronics focuses on OLED self-emissive displays in the HE segment and is also developing QNED; Samsung Electronics pursues multiple paths including QLED and Neo QLED, with webOS and Tizen as their respective operating systems. The two companies follow different technology strategies, which does not imply a value judgment.

How does Samsung Electronics’ semiconductor business affect its comparison with LG Electronics?

The semiconductor business causes Samsung Electronics’ profits to be highly sensitive to chip price cycles, while LG Electronics’ cyclical exposure is more closely tied to home appliances, TVs, and automotive electronics contracts. Structural differences must be factored into any analysis.

What should be considered when comparing the valuation multiples of the two companies?

First, confirm whether business structure allows for meaningful profit comparability. Samsung Electronics’ profits are more affected by DS segment volatility, while LG Electronics is more aligned with consumer electronics and vehicle solutions, so there are limits to horizontal P/E and P/B comparisons.

Do LG Electronics and Samsung Electronics share the same stock code?

No. Both companies are independently listed on the Korean Exchange. Always verify the full company name, financial statements, and stock codes separately to avoid confusing the abbreviations "LG" and "Samsung" with incorrect codes.