Constellation Energy (CEG) operates on a business model that goes far beyond revenue from a single nuclear power plant. Its core lies in a layered portfolio of power assets and customer contracts. The company generates electricity and monetizes it through wholesale markets, capacity markets, long-term power purchase agreements (PPAs), and retail supply relationships.

Many users mistakenly view CEG as merely a "nuclear power company" or an "AI power play." This is only partially accurate. While nuclear assets are central to CEG, natural gas, geothermal, retail customers, commercial contracts, and market prices all significantly impact business performance.

A more robust analytical framework starts with examining CEG’s power assets, then explores how this electricity reaches the market or is contracted, and finally considers how customer demand shapes the value of power. CEG vs Vistra vs NextEra vs Duke provides a comparative view of asset types and regulatory exposure, highlighting CEG’s long-term nuclear value, AI data center demand, and power market risks.

Where does CEG’s electricity come from?

CEG sources its electricity from nuclear, natural gas, geothermal, hydro, wind, and solar assets. Nuclear is the cornerstone, offering stable, long-term baseload generation. Natural gas plants add flexibility, supplying regulation when demand shifts or renewables fluctuate.

Each asset plays a distinct role: nuclear delivers stability, natural gas provides regulation, and geothermal, hydro, wind, and solar diversify the energy mix. For CEG, asset value is defined not only by scale, but by stability, dispatch capability, and how well it matches customer needs.

How does CEG generate revenue through wholesale and capacity markets?

Wholesale power markets reflect real-time supply and demand, while capacity markets value the future availability of power resources. In markets like PJM, generation assets earn not just from producing electricity, but also from capacity payments for reliability and availability.

| Revenue Source |

Definition |

Key Factors |

| Generation Revenue |

Selling electricity to markets or customers |

Power price, generation volume, fuel and O&M costs |

| Capacity Revenue |

Compensation for future available power resources |

Capacity auctions, regional supply-demand, resource certification |

| Contract Revenue |

Long-term supply agreements with customers |

Contract price, duration, delivery terms |

| Retail Supply |

Supplying electricity to commercial or residential customers |

Customer volume, load structure, regional regulations |

This table illustrates that CEG’s revenue is diversified—energy sales are just one part. Capacity markets, long-term contracts, and retail customers all contribute to revenue stability and volatility.

Why is nuclear power ideal for AI data centers?

AI data centers demand continuous, stable, and highly reliable electricity. Training, inference, cooling, storage, and networking require sustained operation—intermittent power is insufficient for large-scale loads. Nuclear power’s 24/7 generation and low direct carbon emissions make it an optimal candidate for data center power strategies.

However, the link between nuclear power and data center demand does not guarantee uniform results for all nuclear companies. Customer contracts, grid connection, delivery timelines, regional pricing, and regulatory frameworks all shape actual returns. CEG’s advantage is asset scarcity; its risks are rooted in execution and regulatory hurdles.

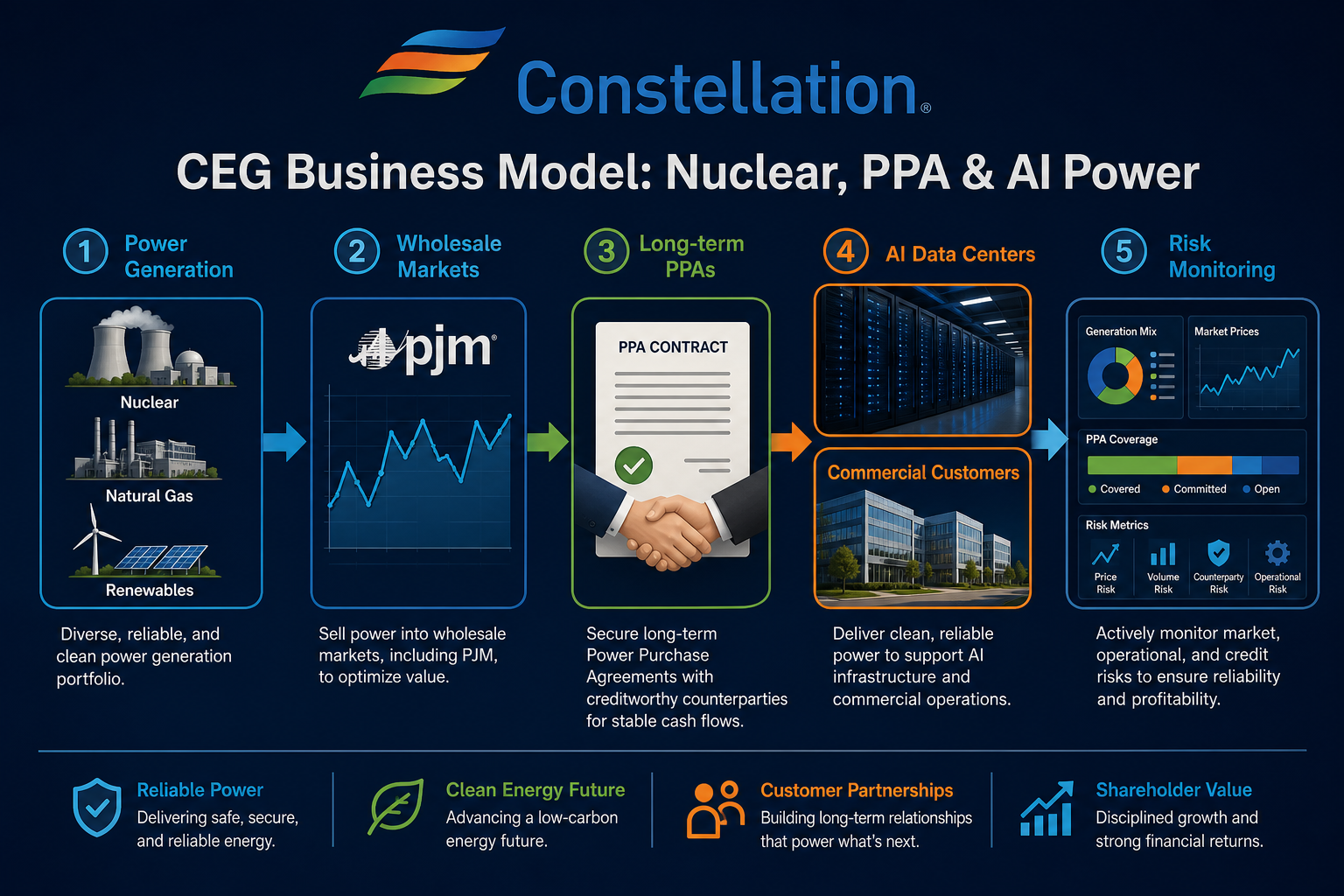

Figure 1. CEG business model flow: Power assets connect AI data centers and commercial demand via wholesale markets, long-term PPAs, and customer contracts.

Figure 1. CEG business model flow: Power assets connect AI data centers and commercial demand via wholesale markets, long-term PPAs, and customer contracts.

What role do long-term PPAs play in CEG’s business model?

Long-term power purchase agreements (PPAs) link generators with large electricity consumers. For data centers, industrial clients, and major enterprises, PPAs secure future supply; for CEG, PPAs enhance revenue visibility and reduce dependence on volatile spot prices.

The value of a PPA extends beyond contract size—it includes term, pricing mechanism, delivery location, grid connection, credit quality, and alignment with actual generation assets. If execution relies on new projects, restarted units, or transmission access, timelines and regulatory approval become critical.

How did CEG’s business structure change after Calpine merged?

With Calpine’s integration, CEG’s portfolio now emphasizes “nuclear foundation + natural gas flexibility + supplemental geothermal resources.” Natural gas assets provide regulation during peak demand or renewable fluctuations, boosting overall supply flexibility.

Mergers bring integration challenges: debt, capital expenditure, system and cultural integration, asset dispatch, and regulatory approval require ongoing oversight. Larger scale does not automatically mean lower risk—the key is whether new assets synergize with CEG’s nuclear base and customer contracts.

For users, Calpine adds a “flexible power” dimension. Nuclear is ideal for stable baseload, natural gas for demand swings and peak regulation; together, they approach an all-weather supply portfolio.

What are the limitations and risks of CEG’s business model?

CEG’s model is constrained by capital intensity, regulatory complexity, and market price sensitivity. Nuclear assets require rigorous safety standards and long-term maintenance; capacity and wholesale prices are shaped by regional supply-demand and policy; data center PPAs face grid, delivery, and customer concentration risks. Trading via Gate Stocks (Buying CEG on Gate Stocks) involves code search and order validation, separate from fundamental company analysis.

Another risk is oversimplification. While AI-driven demand highlights stable power, company outcomes still depend on contract execution, market rules, and asset performance. CEG analysis should layer macro demand, asset capability, and CEG risk metrics checklist for financial and trading review.

Summary

CEG’s business model is defined by: delivering reliable power through nuclear and diversified assets, connecting customer demand via wholesale markets, capacity markets, long-term PPAs, and retail supply. AI data centers are a key demand driver, but not the sole variable. Comprehensive analysis should cover nuclear operations, power markets, customer contracts, merger integration, and regulatory risk.

FAQ

What is CEG’s main source of income?

CEG earns primarily by selling electricity from its generation assets to wholesale markets, capacity markets, long-term PPAs, and retail customers. Nuclear provides stable baseload; natural gas and other resources supply regulation. Capacity markets and long-term contracts influence revenue visibility and volatility.

Why are PPAs important for CEG?

Long-term PPAs connect generators with data centers, industrial clients, and major consumers, securing future supply and improving revenue predictability. PPA pricing, terms, grid arrangements, and credit quality all influence execution outcomes.

Do AI data centers fundamentally change CEG’s business model?

AI data centers raise the importance of reliable, continuous power, but CEG’s model remains anchored in generation assets, power markets, and customer contracts. Data center demand is a significant customer source, but does not replace nuclear operations, regulatory approvals, or market pricing mechanisms.

What does CEG resemble after Calpine’s integration?

Post-Calpine, CEG’s portfolio is closer to “nuclear baseload + natural gas flexibility + supplemental geothermal resources.” The merger expands asset scale and introduces integration, debt, and regulatory variables, which must be evaluated alongside existing nuclear assets and customer contracts.

What should be prioritized when analyzing CEG’s business model?

Review the operational status of nuclear and other generation assets, exposure in wholesale and capacity markets, structure of long-term PPAs and retail customers, and changes from mergers and regulatory policy. Macro demand is background—it cannot substitute for contract and asset capability verification.