Protocol-level identity is the essential gateway for understanding how Concordium (CCD) differs from other public blockchains. Most chains equate "address with identity," placing KYC processes on centralized platforms. Concordium, however, embeds the link between verified entities and accounts directly into the protocol, ensuring that all subsequent transactions, Agent registrations, and attribute checks operate on a unified foundation of accountability.

One common user question is: If compliance is required, why not upload KYC results directly on-chain? Concordium's response is that the chain needs verifiable authorization and attribute conclusions, not permanent exposure of sensitive records. Zero-Knowledge Proofs (ZKP) are the bridge between these requirements.

What Problems Does Protocol-Level Identity Solve? How Is It Different from "Address Anonymity"?

The standard public blockchain model is pseudonymity: addresses are traceable but not necessarily tied to accountable, real-world entities. For basic transfers, this may suffice; for Agent signing, qualification-based service access, or enterprise PayFi, counterparties need to know "who is responsible" and "whether compliance conditions are met"—without seeing all personal data.

| Model |

Identity Location |

Typical Limitation |

| Address anonymity |

No protocol-level binding |

Difficult accountability, compliance relies on off-chain platforms |

| Platform KYC marking |

Centralized database |

Data is siloed, cross-application recognition is limited |

| Protocol-level identity |

Bound at account creation |

Requires support from identity issuance ecosystem |

Concordium's protocol-level identity means every account is associated with a human or business entity verified by an Identity Issuer, and this association is enforced as part of network rules—not as an optional DApp add-on. This enables the Agent Registry registration and verification process to trace Agents back to verified, authorized parties.

How Are Concordium Accounts Linked to Real Individuals or Entities?

The binding process conceptually splits into off-chain verification and on-chain referencing. Users submit required materials to an Identity Issuer recognized by the Concordium ecosystem; after completing KYC or KYB, the issuer grants an identity object to the user's account. What is visible on-chain is the identity reference and cryptographic structure associated with the account—not plaintext scans of documents.

The identity object gives the account a "verified origin": any action signed by the account—including Agent creation, transaction initiation, or attribute proof presentation—can be linked to an entity endorsed by the issuer. Revocation, updates, and expiration rules are governed jointly by the protocol and issuer policies, with parameters defined by current network documentation.

This approach differs from "opening a CEX account and then making an on-chain withdrawal": CEX KYC remains internal, leaving the on-chain address anonymous. Concordium aims for on-chain accounts to carry a verifiable chain of accountability from inception.

How Do Zero-Knowledge Proofs Work? What Attributes Can They Prove?

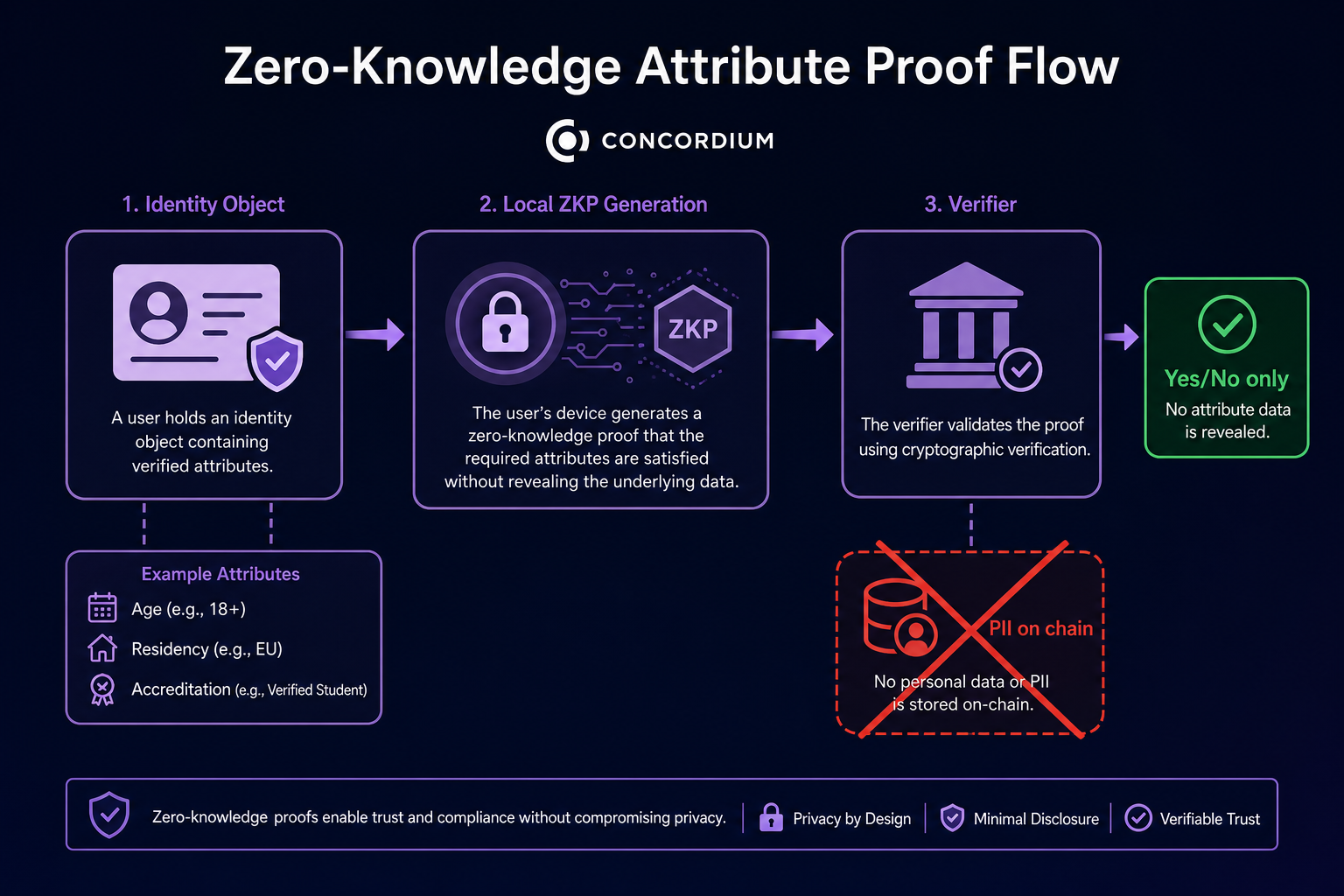

Zero-Knowledge Proofs enable a prover to demonstrate to a verifier that "a statement is true" without revealing additional information required to prove it. In Concordium, such statements are typically attribute-based: whether the user is over 18, resides in a specific country, qualifies as an accredited investor, or is within an authorized spending limit.

The process involves four steps: the Identity Issuer verifies original materials off-chain and writes credentials into the identity object; the user locally generates a ZKP as needed; the verifier (on-chain contract, app, or Agent) checks only the validity of the proof; the result is returned as yes/no or threshold, and original certificate content never enters the ledger.

| Proof Type |

What the Verifier Receives |

What Is Visible On-Chain/Public Layer |

| Age threshold |

"≥18" is true |

No birth date disclosed |

| Residence |

"Located in jurisdiction" is true |

No address disclosed |

| Qualification |

"Has investment level" is true |

No income or asset details disclosed |

The Verify and Access product wraps these attribute checks into interfaces callable by applications, enabling Agents or frontends to obtain clear authorization signals before accessing restricted services. In the Concordium vs Worldcoin discussion: World ID focuses on "unique human," while Concordium's ZKP is used to verify "whether an account meets specific compliance or business requirements."

For enterprise clients, this means onboarding can require "verified account plus specific attribute proof" without building a complete KYC data lake. For Agent frameworks, authorization checks can be inserted before tool calls, preventing unverified Agents from accessing restricted APIs. The identity object's lifecycle includes updates and revocation: when a user's identity status changes or issuer policy updates, credentials may need to be reissued or invalidated, allowing account-level accountability to evolve with compliance needs.

Figure 1. Concordium zero-knowledge attribute proof flow: from identity object to verification result, original personal information never enters the chain.

Figure 1. Concordium zero-knowledge attribute proof flow: from identity object to verification result, original personal information never enters the chain.

How Is Protocol-Level Identity Different from Traditional On-Chain KYC?

"On-chain KYC" is often misunderstood as storing names and ID numbers in blocks. Concordium avoids this: what is persisted on-chain is the identity binding and proof verification capability—not a PII repository. Comparison dimensions are outlined below.

| Dimension |

Traditional On-Chain KYC (misunderstood) |

Concordium Protocol-Level Identity |

| On-chain data |

May include plaintext or hashed PII |

Identity object + proof result |

| Privacy |

Difficult to retract once public |

ZKP enables selective disclosure |

| Interoperability |

Repeated KYC across platforms |

Proofs reused across scenarios for the same account |

| Accountability |

Platform-dependent |

Account-level authorization chain |

For RegTech and Agent ecosystems, the difference is that counterparties verify cryptographic conclusions and issuer endorsements, not trust in a centralized form field copy. PayFi, stablecoin issuance, and tokenized fund scenarios often require confirming investor eligibility or jurisdiction without exposing full profiles—the protocol-level identity + ZKP combination is designed for "verifiable but minimal disclosure."

From a developer's perspective, applications typically don't handle raw KYC packages directly; instead, they call Verify and Access or wallet-side proof generation interfaces to obtain Boolean or enumerated authorization results, then decide whether to allow transactions, Agent calls, or content access. This reduces compliance burdens for frontends and smart contracts, but requires clear product logic: which actions require which attribute proofs.

What Are the Advantages and Limitations of Protocol-Level Identity?

Advantages include: shifting compliance checks to the protocol, reducing repeated identity module integrations at the application layer; ZKP decouples "compliance proof" from "data exposure"; verified accounts provide unified authorization roots for the Agent Registry. For enterprise scenarios, audit trails can focus on accounts and proof events, avoiding distribution of raw KYC packages.

Limitations are clear. Identity quality depends on the coverage and standards of Identity Issuers, and jurisdictional differences lead to varying attribute sets. Users must understand that ZKP generation relies on local wallets and credential status, making operations more complex than purely anonymous addresses. If issuers or credentials expire, proofs must be updated. Protocol-level identity does not automatically solve all off-chain fraud—it addresses "verifiable attributes and accountability for on-chain interactions."

Further, protocol-level identity does not eliminate the need for off-chain audits: regulators or partners may lawfully request records from issuers, but these records do not need to be permanently public on the global ledger due to a single on-chain interaction. For projects, transparent product explanations are necessary to balance privacy commitments with compliance, avoiding misconceptions that ZKP means "completely untraceable."

Summary

Concordium protocol-level identity embeds "verified entities" into the account model, while zero-knowledge proofs enable attribute verification without exposing original data. Understanding this combination is essential for further exploration of Agent Registry, Verify and Access, and PayFi scenarios.

FAQ

What is Concordium protocol-level identity?

Protocol-level identity means Concordium accounts are bound to a human or business entity verified by an Identity Issuer at creation. The chain retains identity objects and cryptographic references—not plaintext personal information. This provides accounts with accountable authorization sources and supports subsequent zero-knowledge attribute proofs.

How does Concordium verify identity?

Verification has two layers: off-chain, the Identity Issuer completes KYC/KYB and issues the identity object; on-chain, or via interfaces like Verify and Access, zero-knowledge proofs generated by the user are validated. Verifiers typically receive only conclusions about attribute satisfaction—not original certificate content.

How do zero-knowledge proofs protect privacy?

Zero-knowledge proofs allow the prover to present valid evidence to the verifier that "a condition is met" without revealing sensitive details required to prove it. For example, proof of "over 18" without disclosing birth date. Concordium uses this to minimize on-chain PII exposure in compliance contexts.

What is the relationship between protocol-level identity and Agents?

Agent Registry links Agents to verified Concordium accounts. Protocol-level identity forms the root of the Agent accountability chain: counterparties verifying an Agent can trace back to an authorized party endorsed by the Identity Issuer. Without this layer, on-chain Agent identity cannot be reliably connected to real responsible parties.

What are the limitations of protocol-level identity?

Limitations include the coverage of Identity Issuers, regional compliance differences, credential updates and expiration management, and the learning curve for ZKP wallet operations. Protocol-level identity addresses on-chain accountability and attribute proof, but does not replace off-chain risk controls or all anti-fraud processes.